Ask an Expert: Is there anything I can do to fix accounts I settled in the past to help my credit so I can buy a house?

Question: I fell behind on credit card payments four years ago and settled a couple accounts for less than the full amount a little over 3 years ago, which I know now was not the wisest decision. My financial situation is much different today than it was but my credit score is still hurting. Is there any way to rectify these accounts and remove them? If I call the credit card companies, will they allow me to pay the amount that they wrote off in the settlement and change the status or am I stuck for four more years waiting in credit score limbo?

Dear Reader,

I understand your frustration. While you can’t change the past, you can focus on “actively” working to improve your score today and in the future.

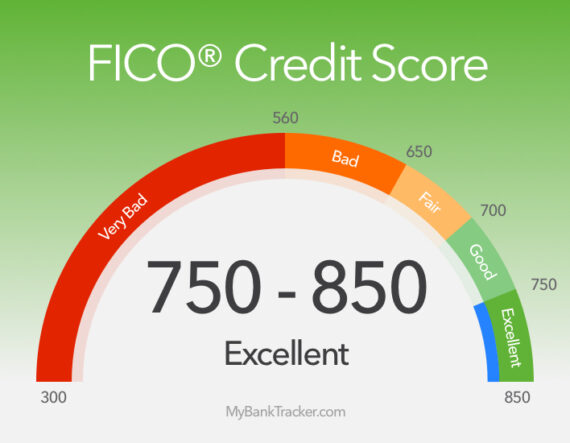

Your credit report is a record of your monthly financial activity. So, you have the power to influence your score each month. To see your score improve, you will need a strategy, discipline, and patience because it takes time to see the results. The first step is to see what’s on your credit report to determine what you need to work on. Instead of relying on data from a simulation software, get copies of your actual reports. You can get free copies from each of the leading credit bureaus–Equifax, Experian, and TransUnion–from annualcreditreport.com every 12 months. If you want to know your score, you can purchase it directly from the credit bureaus, FICO, or get them free of charge from a reliable third party.

When you get your reports, review them carefully, and correct any mistakes if you find any. From what you tell me, it looks like your settled debts may be keeping your score down. Unfortunately, removing those accounts before they are scheduled to drop off is very difficult. In some cases, collectors offer to delete the collections or report settled debts as paid in full when they are trying to collect payment. Yet, the rules of credit reporting don’t always make it possible for those arrangements to succeed. Legally, credit bureaus have to report this information for up to seven years after the first delinquency was reported. Otherwise, collection accounts would be deleted regularly, resulting in inaccurate credit histories for many people.

In your situation, try asking creditors for a goodwill deletion. You can send them a letter appealing to their good nature instead of offering to pay the amount they already forgave. When you settled your accounts, your creditors agreed to consider that debt satisfied. Additional payments won’t improve your score; if anything, bringing old collections current may reset the clock on those accounts.

Assuming that you have positive credit activity every month on your credit report, the negative effect of your collections should be diminishing with time. Your credit reports prioritize current information over the old, so it’s critical you manage your credit effectively. If you haven’t, it’s time to do so. In general, having a good credit report includes maintaining a mix of credit cards and loans, paying on time, using 30% or less of your available credit in each card, and asking for new credit sparingly.

Without details about what’s on your credit report, it’s difficult to give you specific recommendations. You can always talk to an NFCC certified financial counselor to get personalized guidance. Your counselor will review your credit report and overall financial situation to help you find the right strategy to improve your score and get you mortgage-ready. You are already on the right track. Good luck!

Sincerely,

Bruce McClary, Vice President of Communications

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

The post Ask an Expert: Is there anything I can do to fix accounts I settled in the past to help my credit so I can buy a house? appeared first on NFCC.

Read more: nfcc.org