Secured credit and unsecured credit are types of credit that are very different in terms of risk to consumers and lenders.

In a Credit Countdown video on our YouTube channel, credit expert John Ulzheimer explains the benefits and drawbacks of each type of credit and how different types of credit can affect your credit score. Read what he has to say below and watch the video on our channel!

What Is Secured Credit?

Secured credit is a form of credit that is backed by some sort of physical asset as collateral. If the borrower defaults on a secured loan, the lender can take the asset in order to recoup the loss.

Examples of Secured Credit

When you take out an auto loan, the loan is secured by your vehicle. Technically, the lender is the owner of the car until you finish paying off the debt. If you fail to repay the loan as agreed, the lender can take back the car using the process of repossession.

Similarly, when you take out a mortgage, that loan is secured by your home, and the bank still “owns” the home until you pay it off. In this case, not paying your mortgage can lead to the bank foreclosing on your home, meaning that they evict you from the home and then can sell it to someone else.

Pawn shop loans and title loans are also examples of secured loans.

While most credit cards are typically unsecured, secured credit cards do exist for consumers who may not be able to qualify for unsecured credit cards due to bad credit or a lack of credit history. With a secured credit card, you make a security deposit that counts toward your credit limit that the lender can keep in the event that you are not able to make the required payments on your credit card.

Mortgage loans are secured by your home.

What Is Unsecured Credit?

Unsecured credit is credit that does not have a physical asset as collateral, so the lender cannot take back an asset if you default on the debt.

Examples of Unsecured Credit

A student loan is an example of an unsecured loan because there is no material asset that can be taken away if you do not pay your student loans. Student loans are used to pay for an education, and obviously, the lender cannot “take back” the education you have already received.

Credit cards are generally extensions of unsecured credit, except in the case of secured credit cards, as we described above.

Secured Credit

Unsecured Credit

Auto loans

Unsecured credit cards

Mortgage loans

Student loans

Home equity lines of credit

Unsecured personal loans

Secured credit cards

Unsecured lines of credit

Motorcycle loans

Boat loans

Pawn shop loans

Title loans

The Impact of Secured and Unsecured Debt on Your Credit Score

Secured and unsecured accounts are treated equally by credit scoring models, according to John. You are not penalized or rewarded by credit scores based on your accounts being unsecured or secured.

Different types of accounts are still treated differently by credit scores due to other factors (e.g. credit cards are treated differently than installment loans), but this particular factor does not play a role.

Secured Credit Cards: Use Them Carefully

Secured credit card accounts are commonly used by consumers to establish credit or rebuild their credit after having bad credit. This is a valuable credit-building strategy, but you should be cautious about how much you spend on your secured credit card.

Why? Because secured credit cards often have very low credit limits. That means you can quickly get to a high utilization ratio on the account even from modest spending. For example, if your secured credit card has a credit limit of $500 and you spend $250, you already have a utilization ratio on that account of 50%.

Having heavily utilized credit card accounts can have a significant negative impact on your credit score, so if you’re trying to keep your credit score as high as possible, you’ll want to keep an eye on the balance of your secured credit card and not let it creep too high relative to your credit limit.

Secured credit and unsecured credit are types of credit that are very different in terms of risk to consumers and lenders.

In a Credit Countdown video on our YouTube channel, credit expert John Ulzheimer explains the benefits and drawbacks of each type of credit and how different types of credit can affect your credit score. Read what he has to say below and watch the video on our channel!

What Is Secured Credit?

Secured credit is a form of credit that is backed by some sort of physical asset as collateral. If the borrower defaults on a secured loan, the lender can take the asset in order to recoup the loss.

Examples of Secured Credit

When you take out an auto loan, the loan is secured by your vehicle. Technically, the lender is the owner of the car until you finish paying off the debt. If you fail to repay the loan as agreed, the lender can take back the car using the process of repossession.

Similarly, when you take out a mortgage, that loan is secured by your home, and the bank still “owns” the home until you pay it off. In this case, not paying your mortgage can lead to the bank foreclosing on your home, meaning that they evict you from the home and then can sell it to someone else.

Pawn shop loans and title loans are also examples of secured loans.

While most credit cards are typically unsecured, secured credit cards do exist for consumers who may not be able to qualify for unsecured credit cards due to bad credit or a lack of credit history. With a secured credit card, you make a security deposit that counts toward your credit limit that the lender can keep in the event that you are not able to make the required payments on your credit card.

Mortgage loans are secured by your home.

What Is Unsecured Credit?

Unsecured credit is credit that does not have a physical asset as collateral, so the lender cannot take back an asset if you default on the debt.

Examples of Unsecured Credit

A student loan is an example of an unsecured loan because there is no material asset that can be taken away if you do not pay your student loans. Student loans are used to pay for an education, and obviously, the lender cannot “take back” the education you have already received.

Credit cards are generally extensions of unsecured credit, except in the case of secured credit cards, as we described above.

Secured Credit

Unsecured Credit

Auto loans

Unsecured credit cards

Mortgage loans

Student loans

Home equity lines of credit

Unsecured personal loans

Secured credit cards

Unsecured lines of credit

Motorcycle loans

Boat loans

Pawn shop loans

Title loans

The Impact of Secured and Unsecured Debt on Your Credit Score

Secured and unsecured accounts are treated equally by credit scoring models, according to John. You are not penalized or rewarded by credit scores based on your accounts being unsecured or secured.

Different types of accounts are still treated differently by credit scores due to other factors (e.g. credit cards are treated differently than installment loans), but this particular factor does not play a role.

Secured Credit Cards: Use Them Carefully

Secured credit card accounts are commonly used by consumers to establish credit or rebuild their credit after having bad credit. This is a valuable credit-building strategy, but you should be cautious about how much you spend on your secured credit card.

Why? Because secured credit cards often have very low credit limits. That means you can quickly get to a high utilization ratio on the account even from modest spending. For example, if your secured credit card has a credit limit of $500 and you spend $250, you already have a utilization ratio on that account of 50%.

Having heavily utilized credit card accounts can have a significant negative impact on your credit score, so if you’re trying to keep your credit score as high as possible, you’ll want to keep an eye on the balance of your secured credit card and not let it creep too high relative to your credit limit.

Revolving accounts and installment accounts are both important account types when building credit, but they are not equally powerful when it comes to your credit score. Which type of account has a greater impact on your credit score? Keep reading to find out.

Revolving Debt vs. Installment Debt: Definitions

Revolving Credit Account Definition

A revolving credit account is an account that allows you to “revolve” a balance, which means you do not have to pay the full outstanding balance on the account every month.

Revolving accounts typically have a credit limit up to which you can charge up to. You can choose how much to borrow from the account; you do not have to use the full credit limit. Once you make payments against the balance, that amount of credit is then available for you to use again.

Revolving accounts include lines of credit and credit cards.

Installment Credit Definition

Installment credit, in contrast, is credit where the full loan amount is disbursed at one time. You then make regular payments of a fixed amount toward the debt over a certain period of time.

Installment debt includes mortgages, auto loans, student loans, personal loans, credit-builder loans, and any other type of loan that has a regular payment schedule of fixed payments.

How Installment and Revolving Debts Affect Your Credit Score

Revolving Accounts and Your Credit Score

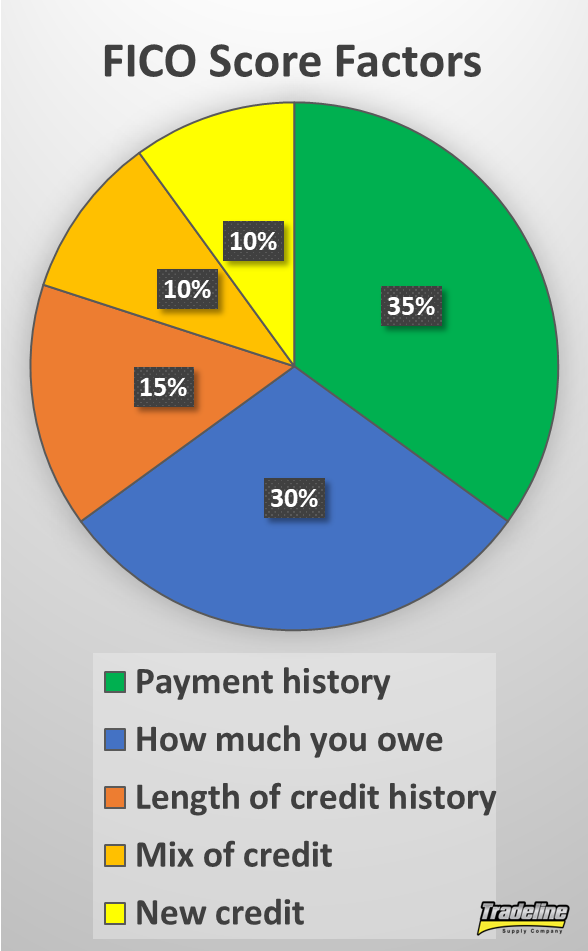

Five main factors are considered by FICO scores.

As you know from our article on credit scores, there are five main factors that influence your FICO score:

Revolving accounts can have a significant effect on each of these five factors.

As far as payment history, it’s important to pay your bills on time every single month just like any other account. However, with revolving accounts, you do not have to pay off the full balance every month. Instead, there is likely a minimum payment amount that you will be required to make. If you make a payment that is less than the minimum payment, your account will still be considered delinquent.

A lot of the power of revolving accounts comes from their influence on your utilization. This is because the credit utilization factor of your credit score places much more importance on the utilization of your revolving accounts.

Having high revolving utilization means that you are using a large portion of your available credit, which indicates to lenders that you might be at an increased risk of default. That’s why high credit utilization is bad news for your credit score.

If you run up a balance on a credit card and then only pay the minimum payment each month, you will be increasing your credit utilization. Since utilization makes up 30% of your FICO score, carrying a balance on your revolving accounts can seriously reduce your score.

Credit age is also important since it goes hand-in-hand with payment history. The longer you keep your revolving accounts open, the better. Even after they are closed, they can still continue to age and impact your average age of accounts.

Having a few different revolving accounts is also beneficial to your credit mix. Consumers with FICO scores of 785 and up have an average of seven credit cards in their credit files, including both open and closed accounts. In fact, if you don’t have enough revolving accounts, you can get dinged for a “lack of revolving accounts,” because without them there is not enough information to judge your creditworthiness, according to Discover.

Having too many inquiries for revolving accounts or too many new revolving accounts can hurt your credit score. Typically, each application for a revolving account is counted as a separate inquiry.

Installment Loans and Your Credit Score

When it comes to your credit score, installment loans primarily impact your payment history. Since installment loans are typically paid back over the course of a few years or more, this provides plenty of opportunities to establish a history of on-time payments.

Since installment loans typically don’t count toward your utilization ratio, you can have a high amount of mortgage debt and still have good credit.

Having at least one installment account is also beneficial to your credit mix, and installment debt can also impact your new credit and length of credit history categories.

What installment loans do not affect, however, is your credit utilization ratio, which primarily considers revolving accounts. That’s why you can owe $500,000 on a mortgage and still have a good credit score. This is also why paying down installment debt does not help your credit score nearly as much as paying down revolving debt.

This is the key to understanding why revolving accounts are so much more powerful than installment accounts when it comes to your credit score. Credit utilization makes up 30% of a credit score, and that 30% is primarily influenced by revolving accounts, not installment accounts.

In addition, with a FICO score, multiple inquiries for certain types of revolving accounts (mortgages, student loans, and auto loans) will count as just one inquiry as long as they occur within a certain time frame. As an example, applying for five credit cards will be shown as five inquiries on your credit report, whereas applying for five mortgage loans within a two-week period will only count as one inquiry.

Why Are Revolving and Installment Accounts Treated Differently By Credit Scores?

Now that you know why revolving accounts have a more powerful role in your credit score than installment accounts, you might be wondering why these two types of accounts are considered differently by credit scoring algorithms in the first place.

According to credit expert John Ulzheimer in The Simple Dollar, it’s because revolving debt is a better predictor of higher credit risk. Since credit scores are essentially an indicator of someone’s credit risk, more revolving debt means a lower credit score.

Since revolving accounts like credit cards are usually unsecured, they are a better indicator of how well you can manage credit.

Why is it that revolving debt better predicts credit risk than installment debt?

The first reason is that installment loans are often secured by an asset such as your house or car, whereas revolving accounts are often unsecured. As a result, you are going to be less likely to default on an installment loan, because you don’t want to lose the asset securing the loan (e.g. have your car repossessed or your home foreclosed on). Since revolving accounts such as credit cards are typically unsecured, you are more likely to default because there is nothing the lender can take from you if you stop paying.

In addition, while installment debts have a schedule of fixed payments that must be paid every month, revolving debts allow you to choose how much you pay back each month (beyond the required minimum payment). Since you can decide whether to pay off your balance in full or carry a balance, revolving accounts are a better reflection of whether you choose to manage credit responsibly.

How to Use Revolving Accounts to Help Your Credit

Since revolving accounts are the dominant force influencing one’s credit, it is wise to use them to your advantage rather than letting them cause you to have bad credit.

Here’s what you need to do to ensure your revolving accounts work for you instead of against you:

Make at least the minimum payment on time, every time.

Don’t apply for too many revolving accounts and spread out your applications over time.

Aim to eventually have a few different revolving accounts in your credit file.

Keep the utilization ratios down by paying off the balance in full and/or making payments more than once per month. Use our revolving credit calculator to track your utilization ratios.

Avoid closing revolving accounts so that they can continue to help your credit utilization.

Revolving Accounts vs. Installment Accounts: Summary

Revolving accounts are given more weight in credit scoring algorithms because they are a better indicator of your credit risk.

Revolving accounts play the primary role in determining your credit utilization, while installment loans have a much smaller impact. High utilization on your revolving accounts, therefore, can damage your score.

With a FICO score, inquiries for installment loans are grouped together within a certain time frame, while inquiries for revolving accounts are generally all counted as separate inquiries. Therefore, inquiries for revolving accounts can sometimes hurt the “new credit” portion of your credit score more than inquiries for installment accounts.

Use revolving accounts to help your credit by keeping the utilization low and keeping the accounts in good standing.

Bad credit is something we all fear, but what is actually considered poor credit and how could it affect you? In addition to explaining what bad credit is and why you need to avoid it, we’ll also provide some strategies in this article to help you fix bad credit.

What Is a Bad Credit Score?

The definition of “bad credit” varies depending on which credit scoring system you are talking about. Since FICO 8 is the scoring model most widely used by lenders, we will focus on FICO when discussing the question of what is considered bad credit.

The FICO 8 credit scoring system assigns consumers a number to represent their creditworthiness, with the lowest credit score possible being 300 and the high end of the scale being 850.

A high credit score shows lenders that they can be fairly confident that a consumer will repay debts because they have demonstrated responsible behavior when it comes to credit in the past.

A low credit score, on the other hand, means that someone represents a higher risk to lenders because they are thought to have a higher probability of defaulting on a loan.

According to Credit Karma, a FICO score between 300 to 579 is considered a poor credit score, while a fair credit score is between 580 and 669. In contrast, an excellent credit score is between 800 and 850.

Credit scores between 300 and 579 are considered poor credit.

What Gives You Bad Credit?

As we mentioned, a bad credit score means lenders perceive you as a high-risk borrower. Therefore, what causes bad credit is poor management of credit and risky behaviors that indicate you may have a higher probability of default.

For example, being late on payments or missing payments altogether can really hurt your credit because payment history is the most important factor of a credit score.

High credit card utilization can lead to bad credit. Photo by Natloans

What causes bad credit specifically? Here are some more examples:

Late or missed payments

Defaulting on a loan

Charge-offs Collection accounts

Judgments

Settlements

Bankruptcy

Foreclosures or repossessions

Maxed out or high-utilization credit cards

Too many inquiries at one time

Too much new credit

Sometimes people have bad credit because of things they can’t control, like having a medical emergency that leads to huge hospital bills that they can’t afford to pay. In fact, the majority of consumer debt in collections is medical debt, according to Magnify Money.

Bad Credit Loans

If you have bad credit, you’re likely going to have a hard time getting loans with favorable terms or possibly even getting approved for a loan in the first place. Since a bad credit score represents a high risk for the lender, loans for people with poor credit typically have higher interest rates and may require collateral or a down payment—if the lender is willing to approve the loan at all.

Personal Loans for Bad Credit

Payday loans can come with interest rates of up to 400%. Photo by Aliman Senai.

Personal loans for bad credit are few and far between. Usually, at least fair credit is needed to be considered for a loan. Bad credit loan lenders may charge very high interest rates since they are taking on a lot of risk by lending money to someone with poor credit. These higher interest rates may translate into thousands of dollars of additional interest payments over the term of a loan.

Very bad credit loans such as payday loans often have astronomical interest rates of up to 400%, which makes it nearly impossible for many consumers to get out of debt.

Bad Credit Car Loans

Bad credit auto loans, also known as subprime auto loans, are often considered “second-chance” loans because they are typically the next option for those who have been rejected for traditional auto loans. Although there is not necessarily an official dividing line between which credit scores are considered prime and subprime when it comes to auto loans, credit scores below 620 tend to be considered subprime.

Car loans for bad credit, similar to personal loans for bad credit, are associated with much higher costs than prime auto loans. Since lenders of second-chance auto loans are taking on additional risk, these loans often have significantly higher interest rates and more fees than auto loans for consumers with good credit. Additionally, car loans for bad credit may come with penalties for paying off the loan early.

Bad credit car loans can have triple or more the interest rate as prime auto loans. Photo by QuoteInspector.com.

According to Investopedia, “While there is no official subprime auto loan rate, it is generally at least triple the prime loan rate, and can even be five times higher.”

Credit Cards for Bad Credit

If you have bad credit, your options for getting a credit card will be limited, and you will most likely not be able to get the perks associated with premium credit cards, such as low interest rates, high credit limits, and rewards. Credit cards for poor credit may also come with annual or even monthly fees.

Subprime credit cards often require you to make a deposit with the lender as collateral. These cards are known as secured credit cards since they are secured by your deposit, which the lender can keep if you fail to make payments on the card. Sometimes, the lender may be willing to switch you to an unsecured card after you have shown a history of consistent on-time payments.

As we’ve seen with loans for bad credit, credit cards for bad credit, both secured and unsecured, will likely have high interest rates, sometimes as high as 30% or more.

How to Fix Bad Credit

Having a bad credit score is expensive. It makes getting any kind of credit more difficult and more costly because bad credit lenders tack on high interest rates and fees to compensate for the higher financial risk of poor credit loans.

Bad credit doesn’t just dramatically increase the cost of credit. It can also affect other aspects of your life, such as your insurance premiums, your ability to find housing, and even your job, since many employers now check prospective employees’ credit reports. Therefore, most people with bad credit want to fix it as soon as possible.

Here are some strategies that you can try if you need to fix bad credit.

Credit Repair

If you have bad credit as a result of identity theft or extensive errors on your credit report, you’ll likely need to undergo credit repair in order to clean up your credit file.

Some people opt to try their hand at DIY credit repair, while others may prefer to hire a trusted credit repair company to get help with the dispute process and potentially faster results. [Disclosure: This article contains affiliate links.]

Either way, it’s important to be aware of best practices when disputing credit report errors. It’s best to submit your dispute by sending a letter along with documentation to verify your identity and support your claim. Trying to dispute errors online or over the phone may not yield the best results.

In addition to disputing inaccurate information with the credit bureaus, it’s also important to contact the company that is furnishing the data so that the error doesn’t get reported again in the future.

Rebuilding Credit

Improving bad credit takes time and patience. While credit repair companies may claim to have tactics that can boost your credit fast, the reality is that these tactics are usually limited to removing inaccurate information from your credit report. If you remove everything from your credit report, what are you left with?

The best way to fix bad credit, beyond correcting inaccuracies, is to rebuild it with more positive credit history over time. In other words, you need to add more positive accounts to your credit profile and keep them in good standing while they age. At certain age levels, these accounts should begin to boost your credit profile with that positive payment history.

Rebuilding credit with positive credit history helps to fix bad credit.

One option that can help people re-establish credit is opening a credit-builder loan, which works in the reverse order of a traditional loan. Instead of receiving the loan amount up front and then making payments to the bank to pay off your debt, with a credit-builder loan, you make all the payments first and then receive the funds after you have finished paying off the loan. Since these loans are much less risky for lenders, they can be offered to those struggling with bad credit or lack of credit history.

Generally, though, building credit by opening new accounts can take at least two years to see much of a positive effect. The best way we have seen to bypass this two-year waiting period is by piggybacking on the good credit of others.

Have you been affected by bad credit? What did you do about it? Tell us your story in the comments.

If you have bad credit or no credit at all, you’ll likely have a hard time getting a loan. After all, the paradox of credit is that it’s hard to get credit without already having a credit history, much like trying to get a job without any work history.

A credit-builder loan can be a good option for those with no credit or bad credit because credit-builder loans do not require the borrower to have good credit to get approved. However, you will need to show that you have enough income to cover the monthly payments.

Just like a traditional loan, your payment history will be reported to the major credit bureaus. That means you need to make all of your payments on time if you want to build up your credit score.

How Do Credit-Builder Loans Work?

Credit-builder loans, also sometimes called “fresh start loans” or “starting over loans,” are set up differently than traditional loans in order to minimize risk for lenders.

These loans are typically small amounts, such as $500 or $1000. In addition, unlike other types of loans, you do not receive the money upfront and pay it back later. Instead, this process is reversed.

The definition of a credit-builder loan is a loan where you make the payments first and receive the funds after you have finished paying off the loan. The lender deposits the amount you are borrowing into a savings account or certificate of deposit that will be held for you until you finish making all the payments. Until that point, you can’t access the funds.

Do You Need a Credit Check to Get a Credit-Builder Loan?

Because credit-builder loans are low-risk, in many cases, you can apply for credit builder loans with no credit check. You’ll likely just need to provide your income to prove that you can afford to make the payments.

Banks That Offer Credit-Builder Loans

Most of the big national banks, such as Chase, Bank of America, and Capital One, do not typically offer credit-builder loans, although Wells Fargo offers secured personal loans.

The best credit-builder loans can often be found at local banks and credit unions or through online lenders.

Payment history makes up 35% of your FICO score.

Are There Downsides to Getting a Credit-Builder Loan?

With a “fresh start” loan, as with any loan, it can hurt your credit score if you miss any payments. Remember, payment history is the biggest contributing factor to your credit score, weighing in at 35%. So when it comes to building credit, you need to be prepared to make every single payment on time.

In addition, you will be paying interest on the loan and potentially an application fee or other fees, although some lenders may partially refund the interest if you pay the loan back on time.

Finally, it may be several months to over a year before you finish paying off the loan and receive your borrowed funds. Building up a credit score by making payments on a loan takes a minimum of six months of payment history, according to FICO.

Other Ways to Build Credit

For those looking to build or rebuild credit, credit-builder loans are just one option. If you need to build credit fast, also consider one of the credit piggybacking methods we cover in “The Fastest Ways to Build Credit.”

By purchasing authorized user tradelines, for example, you can add seasoned tradelines with years of credit history to your credit report within just days.

Conclusions on Credit-Builder Loans

For those who may be struggling to build credit due to bad credit or lack of credit history, a credit-builder loan represents one way to get a loan with no credit check and start building a positive credit history.

Just like other types of loans, credit-builder loans come with interest and fees, and the main downside of this type of loan is that you don’t have access to the funds until after you have made all the payments.

On the other hand, when you finish paying off the loan, you will have built up a record of on-time payments and you will have a chunk of savings to take home.

Businesses these days revolve around creating the perfect customer experience. Trends and preferences change with the blink of an eye, and businesses that can’t keep up are cut out of the race. A study shows that only 80% of the businesses cross their first-year mark and around 45% to 51% of the business survive for more than five years. One of the main reasons for this may be the lack of financing for immediate business requirements.

Recently, there has been an evolution in financing structure and procedure to facilitate easy and quick loans for businesses. Today, financing for small businesses can be classified into two types – traditional financing and alternative financing.

Traditional funding is given by established institutions. A few examples of the traditional financing options available are below.

1) Bank Loans:

Most banks offer term loans, a business line of credit or equipment loans. Term loans are preferred if you need money to fulfill your immediate business needs. A lump sum amount of money is given to be repaid in a fixed time period. The bank interest rate for the amount borrowed is added to the repayable amount. With a business line of credit, you can borrow money from the bank when you want per your business requirement. The interest rate will apply only for the money you have borrowed. Equipment loans are lesser-known bank loans that can cover between 80 to 100% of your business equipment costs This type of loan is useful in most business industries especially construction and auto repair.

Bank loans are one of the hardest loans to qualify for because the average APR for bank loans is 2.24% to 4.47% . The lower the interest rate, the tougher it is to get.

2) Government Grants

Bank loans and their strict lending requirements give rise to other kinds of traditional financing options. Banks and other lending institutions will provide the loan when it’s guaranteed by the government to small businesses. Government grants are not applicable for starting a business, paying off debt or for operational expenses. To learn whether a grant applies to your small busines, visit grants.gov.

3) Investment Capitals

The Small Business Administration has an Small Business Investment Capital(SBIC) program that is powered by private equity fund managers who pool capital for small businesses. This loan is guaranteed by the government and is a win:win for both the investor and the small business owner.

Alternative financing is not cash, stocks or bonds. It is immediate capital that is provided to the business to streamline their existing processes or launch new ones. The prerequisites for acquiring these types of funding is also comparatively lenient to their traditional counterparts and varies by type.

4) Crowdfunding

The accumulation of money from various investors for a single cause or business is called crowdfunding. There are many crowdfunding platforms where you can enroll and get huge financing from multiple investors. The best part of crowdfunding is that you do not have to depend on a single person or entity to provide you with a large sum of money.

5) Invoice Factoring

In this method, the lender takes responsibility for your invoices and directly collects the money from the concerned people/business. Invoice factoring or accounts receivable factoring allows you to bring cash inflow to your business and not sit around waiting for customers to settle their invoice amounts.

6) Short Term Loans

Short term loans are one of the most common types of alternative funding where you can borrow an amount of up to $200,000 depending on your business requirements. You can repay this amount within the next 3 to 18 months but, the APR (Annual Percentage Rate) is usually higher than the traditional financing sources.

Short term loans do not need a high credit score, a business plan or even three months bank statement and the amount requested will be approved almost immediately. It’s important that you have a plan for repayment of all types of loans, especially this one since the payment terms are for a shorter amount of time and have a higher interest rate.

7) Small Business Administration (SBA) Loans

SBA loans are government aided financing options where you can get loans for your small business with interest rates like bank loans. This loan does not fund businesses directly but allows lenders to pool in money and finance your business. As this is a government-led scheme, the SBA (small business administration) covers the losses of lenders in case of failed businesses.

Running a business can be an arduous task. With all the different types of financing options presented to you, it’s up to you to choose the best ones that fit your business model and requirements.

If you are struggling with getting the funding you need because your credit isn’t up to par, reach out to an NFCC small business coach today!

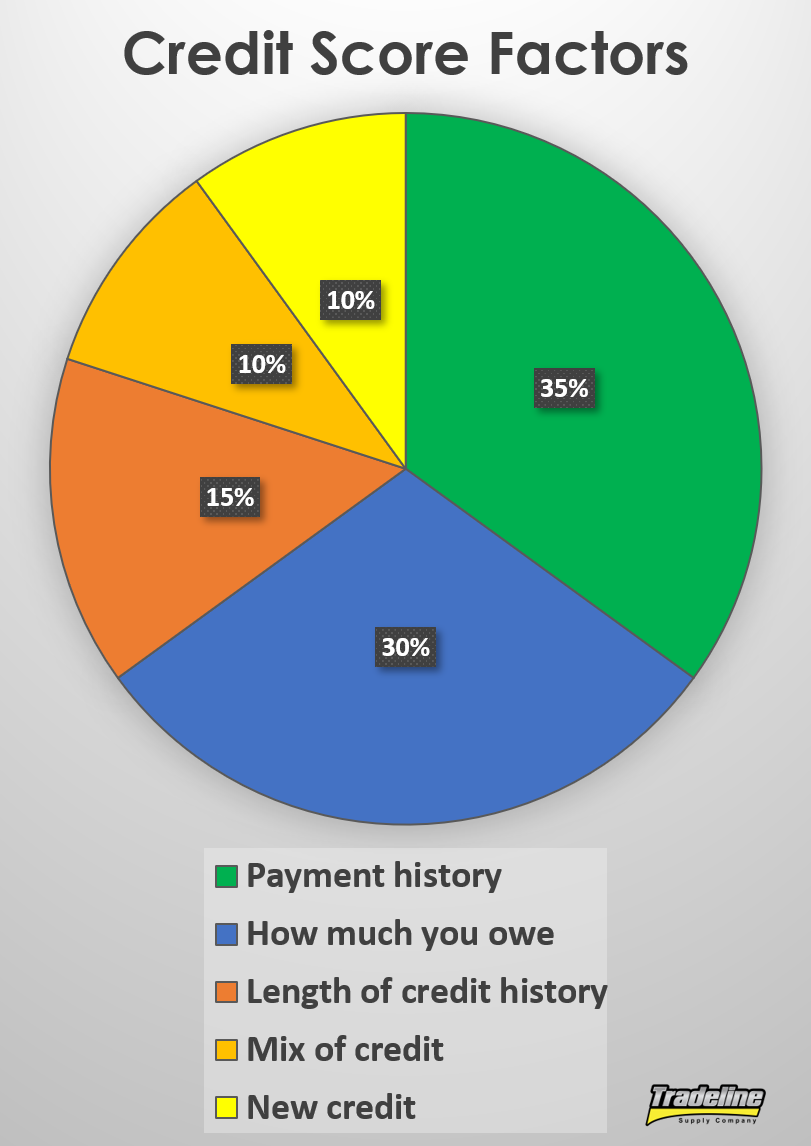

Credit mix, also called mix of credit, is one of the factors that your credit score takes into account. It is one of the least important factors, weighing in at 10% of a FICO score.

Credit mix is the diversity of types of credit accounts in your credit report. Having different types of credit accounts in good standing in your credit file demonstrates that you can use credit responsibly. Lenders ideally want to see that you have successfully managed a diverse mix of multiple types of accounts.

Types of Credit Accounts

Depending on how you define the types, there are 3-4 general categories when it comes to types of credit.

Revolving credit is a form of credit with which you can “revolve” or carry a balance each month. You are assigned a credit limit that you can charge up to and you make a payment each month. Interests will typically be charged if you carry a balance from month to month. Credit cards and lines of credit are the most common types of revolving credit accounts.

Charge cards are similar to credit cards, except the balance must be paid in full every month.

Service credit includes accounts with your service providers, such as utilities, cell phone service, etc. These are considered credit accounts because the service is provided before you pay the bill.

Installment credit is a loan of a specific amount of money that you pay back in regular payments of the same amount over a certain period of time. Types of installment loans include car loans, mortgages, student loans, etc.

Credit Karma simplifies the categories to 3 types of credit:

Revolving credit

Open credit (includes charge cards)

Installment credit

Examples of Revolving Credit

As we touched on above, the two most common types of revolving credit are credit cards and lines of credit.

Credit cards include those issued by banks such as Capital One, Bank of America, and Chase, as well as store cards, which can typically only be used at a particular retailer.

Lines of credit are similar to credit cards in that you have access to a set amount of money—your credit limit—that you can draw from. After you borrow money from your line of credit, the balance starts accruing interest, and when you pay it back, that credit is then available again for you to use. This is why it’s considered revolving credit: you can use it again and again as long as you keep paying it back.

Types of Lines of Credit

A home equity line of credit (HELOC) is secured by your home.

Lines of credit can be either secured, which means the borrower has provided collateral to back the line of credit in case of default, or unsecured, meaning no collateral is required.

Beyond those general categories, there are three main types of lines of credit.

A home equity line of credit (HELOC) is a line of credit secured by your equity in your home, which is the difference between the value of your home and the amount you still owe on your mortgage. Since your home equity serves as collateral, if you default on a HELOC, you could risk losing your home to foreclosure.

A personal line of credit is usually unsecured, although sometimes you may be able to provide collateral in the form of savings or investments.

A business line of credit may be secured or unsecured. They are offered by financial institutions as well as many commercial vendors.

Examples of Installment Loans

An auto loan is one type of installment account.

Types of installment credit include:

Auto loans

Mortgages

Student loans

Personal loans Credit-builder loans

Home equity loans (not to be confused with a HELOC, which falls under revolving credit)

The breakdown of account types outlined above is a simplified version of how credit scoring systems actually categorize different types of accounts. In reality, credit scoring models may consider as many as 75+ account types.

In addition, each type of account could have a different effect on your credit.

How Does Credit Mix Affect Your FICO Score?

As we mentioned at the top of this article, credit mix makes up about 10% of your FICO score. With VantageScore, type of credit and credit age are combined into the same category, which makes up approximately 21% of your VantageScore.

With both types of scores, credit mix is a relatively small portion of what determines a credit score, so having the perfect credit mix is not necessarily essential in order to have good credit. However, it’s still a good thing to aim for, especially if you want to get a perfect 850 credit score or somewhere close to it.

What Is a Good Credit Mix?

When it comes to your credit score, the most important thing is to demonstrate that you have managed both revolving and installment accounts. Therefore, it’s best to have at least one type of account of each type.

FICO high score achievers have an average of seven credit cards on their credit reports. Photo by Hloom on Flickr.

For example, you might have a credit card (revolving) and an auto loan (installment). Or, you could have a mortgage (installment) and a HELOC (revolving). Any combination of one revolving account and one installment account is a good start for your credit mix.

FICO supports this idea, saying, “Having credit cards and installment loans with a good credit history will raise your FICO Scores.”

FICO also says that people who have managed credit cards responsibly are better off than consumers that don’t have any credit cards, who can be seen as risky because they have not demonstrated experience in using revolving credit.

Statistics show that high FICO score achievers have an average of seven credit cards on their credit reports, which includes both open and closed accounts.

People with credit scores in the 800s also typically have installment loans such as mortgages and auto loans, according to Experian.

The total number of accounts in your file may also play a role. FICO has indicated that those with high credit scores can have 20+ credit accounts in their credit reports.

How Many Credit Cards Is Too Many?

Having too many credit card accounts could hurt your credit score.

Keep in mind that it is possible to have too many accounts on your credit file. According to the FTC, having too many credit cards could have a negative effect on your credit score, as could having loans from some types of companies.

There is no hard-and-fast rule when it comes to how many credit cards is too many because the impact of any given factor on your credit score depends on what is already in your credit profile, says FICO.

However, in figure 1 in the article “How Credit Actions Impact FICO Scores,” the hypothetical consumer “Rachel,” who has 33 credit accounts, has a lower credit score than “Maria,” who has 21 accounts. This would seem to imply that at some number between 21 and 33 accounts, one’s credit score might begin to suffer. However, these two consumers have other differences in their credit profiles, so the difference in their credit scores cannot be solely attributed to the number of accounts in their files.

Can Some Account Types Hurt Your Credit?

Certain types of loans on your credit report could make you seem like a more risky consumer and therefore could end up hurting your score instead of helping.

Why? It’s all based on statistics and who the credit score algorithms have deemed to be risky borrowers.

For example, taking out a furniture loan could actually drop your credit score. That’s because furniture loans are often reported as “consumer finance loans,” which are typically reserved for borrowers with bad credit who are statistically more likely to default on loans. Therefore, having this type of account on your credit report could be viewed as risky by lenders and credit scoring algorithms.

Alternatively, the financing arrangement may be reported as revolving debt, which will appear nearly maxed out until you make enough payments to get the balance to a lower level.

Payday and title loans, however, are typically not reported to the credit bureaus, so these types of loans won’t count toward your credit mix or credit score—unless, of course, you default on a loan and it gets sold to a collection agency, who will then report it as a collection account.

Conclusions on Credit Mix

Since credit mix makes up about 10% of your credit score, it is helpful to try to achieve a balanced mix of credit by keeping a few revolving and installment accounts in good standing. The best credit mix should ideally include a few credit cards and at least one or two installment loans, such as mortgages or auto loans.

However, it’s also important to note that credit mix is much less important than other credit score factors, such as payment history, credit utilization, and credit age. It’s probably not worth obsessing over because you won’t automatically get an excellent credit score just by having the perfect mix of accounts.

In addition, most people naturally accumulate different types of accounts over time, so it’s not necessarily the best idea to start opening new accounts left and right just to build up your credit mix. This strategy could result in lots of inquiries and new accounts bringing your score down in the short term, and having access to credit you don’t need could also encourage extra spending.

As with all credit-related decisions, it’s up to you to take your overall financial goals and priorities into account before taking action. You might decide that you don’t need to worry too much about improving your credit mix, and that’s fine. On the other hand, improving your credit mix can only help your credit score, and it is something that you should pay attention to if you want to get a perfect 850 credit score.

Secured credit and unsecured credit are types of credit that are very different in terms of risk to consumers and lenders.

Secured credit and unsecured credit are types of credit that are very different in terms of risk to consumers and lenders.