The vast majority of lenders use your FICO credit score to evaluate your credit risk as a consumer when they are deciding whether or not to extend credit to you. And yet, historically, it has been costly for consumers to access their own FICO scores.

Popular websites such as Credit Karma and Credit Sesame offer free credit scores, but the scores provided are usually VantageScores, not FICO credit scores.

Knowing your VantageScore is still valuable information, but it is not directly tied to your FICO Score, so it is less useful when it comes to preparing to apply for credit. While it is often true that a consumer’s FICO score is similar to their VantageScore, in some cases, they may be vastly different, especially depending on which credit scoring models are used and which credit bureaus are providing the credit report information.

If you need to check your FICO score, where can you do so without paying a fee to access it?

Here are some of the best places to get your FICO score for free.

Your Credit Card Issuer

Several major credit card issuers now offer consumers the ability to check their FICO scores for free.

Discover Bank

Discover offers a free way to check your FICO score with their Credit Scorecard program. Even consumers who do not have a relationship with Discover Bank can freely use this feature.

Experian provides the credit report data that is used to calculate your FICO score. Your credit score updates once every 30 days and Discover notifies you when it is time to check your new FICO score.

In addition, Discover’s FICO Credit Scorecard keeps track of your credit score history so you can see how it changes from month to month.

The Credit Scorecard also provides a summary of what is going on with each of the five credit score factors that are influencing your FICO score: your payment history, credit utilization, length of credit history, mix of credit, and new credit (e.g. inquiries). You can find educational information about credit scores on the website as well.

To access your FICO score with Discover’s FICO Credit Scorecard, either visit their website or use the bank’s mobile app.

Bank of America

Bank of America is another widely used bank that offers free FICO scores to consumers. However, to enroll in this program, you must be a Bank of America credit card customer.

Much like Discover’s offering that we described above, Bank of America’s FICO Score Program provides customers not only with their FICO scores but also information on the major factors that influence your credit score, your month-to-month credit score history, and education about how to achieve and maintain good credit.

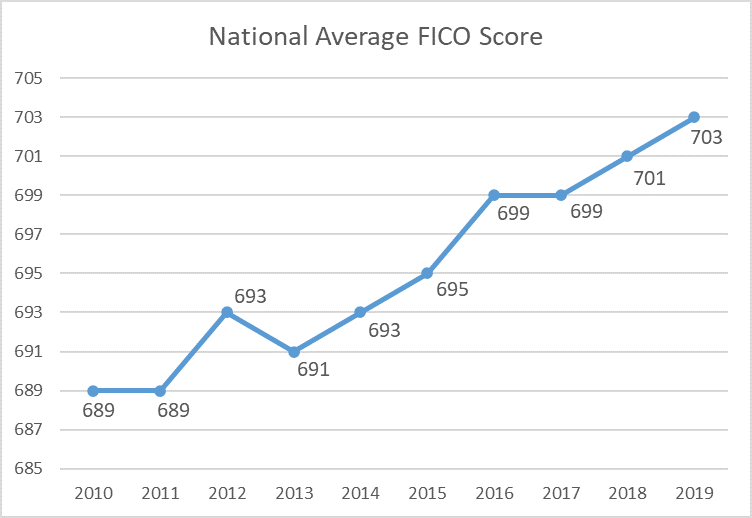

On top of this, Bank of America also compares your credit score to the national average.

Bank of America customers can view their FICO score for free on the company’s website or mobile app.

Citibank

Consumers who have Citibank branded credit cards can obtain their FICO score for free from Citi.

Citi states on their website, “We think it’s important to provide our cardmembers with free access to information that will help them understand and stay on top of their credit status. That’s why we’re providing you with your FICO® Score and information to help you understand it.”

Your FICO score from Citibank is determined using information from your Equifax credit report and the FICO Bankcard Score 8 credit scoring model. Unlike the standard version of FICO 8 that you may be used to seeing, which ranges from 300 to 850, the bank card model used by Citi ranges from 250 to 900. It is updated once a month.

You can find more information on Citi’s free FICO score program on their website.

American Express

Recently, American Express started providing access to free FICO scores to consumers who have American Express credit cards.

The bank uses the standard version of FICO 8, so the credit score range spans from 300 to 850. Experian provides the credit report data used to calculate your score.

As with the other free FICO score programs, you also get to see how your FICO score changes over time and you receive a summary of the factors affecting your credit score.

American Express credit cardholders can see their FICO scores in their online account or on their monthly statement.

Those who do not have credit cards with American Express can get their TransUnion VantageScore for free through the company’s MyCredit Guide program, but this does not include FICO scores.

Barclays

FICO scores from TransUnion are available to all Barclays credit card customers through the bank’s online banking system.

Once you have had your Barclays card for three months, you can see a chart of your FICO score history over the time you have had an account open with Barclays, according to SmartAsset.

Plus, Barclays will send you alerts via email if your credit score changes, including an explanation of why your score has changed.

Wells Fargo

Wells Fargo account holders who use their online banking platform can view their FICO credit score within their online account.

Additional features include your credit score history, information on your credit score factors, and personalized credit tips from Wells Fargo.

According to the bank, they offer your FICO score for free in order to “support your awareness and understanding of FICO® Credit Scores and how they may influence the credit that’s available to you.”

The FICO score you get through Wells Fargo is calculated using Experian credit report data and is updated once a month.

Experian

Experian is the only major credit bureau that offers consumers their FICO 8 scores for free along with their Experian credit reports.

In addition, Experian offers an alternative credit data program called Experian Boost, which can add positive payment history from certain bills to your credit report, such as utilities and Netflix.

Sign up on Experian’s website to start using these free services.

Your Local Bank or Credit Union

Not all banks and credit unions offer customers the ability to check their FICO scores for free, but it is worth asking if you do not have access to the previous options. If your local bank or credit union does not offer free FICO scores, they may be able to help direct you toward somewhere that does.

Will Checking Your FICO Score Hurt Your Credit Score?

Although this is a common concern, checking your own credit score should never hurt your credit.

This credit myth likely arises from the fact that hard inquiries on your credit report can have a small negative effect on your score.

However, hard credit inquiries only happen when you are actively seeking credit and a lender has to pull your credit report to decide whether or not to loan you money.

All other credit checks, including those you conduct yourself for educational purposes, are considered to be soft inquiries, which do not affect your score at all.

Final Thoughts on How to Get Your FICO Score for Free

If you want to be able to see your FICO score for free, there are many options available to you, especially if you have credit card accounts with major banks such as those listed above.

FICO also has a program called FICO Score Open Access that aims to enhance consumer access to FICO scores and educate consumers about the topic. FICO has a list of additional lenders and credit and financial counseling organizations that participate in this program, which you can browse in case you do not have any accounts with the banks mentioned here.

Keep in mind that lenders use many different versions of FICO scores, including older generations and versions that are specific to certain industries. That means that when you check your FICO score for free, it is not guaranteed to be the same exact FICO score that a lender will use when you apply for credit.

When you check your FICO score using one or more of the methods in this article, take note of which credit bureau is supplying the information as well as which FICO score version is being used to calculate the result so that there is no confusion if you see a different FICO score somewhere else.

Finally, remember that you can also get your VantageScore for free in many places as well. While it’s not the same as your FICO score, it can still provide educational value as it uses the same general principles to calculate your score.

Let us know if this article helped you find a way to get your FICO score for free by commenting below!

One question we often hear in the tradeline industry is “Do tradelines still work in 2021?”

Fortunately, we can say with certainty that tradelines do still work in 2021, and we are confident they will continue to be effective for years to come.

To explain our answer, we will delve into the history of authorized user tradelines and the policies that regulate the tradeline industry.

Why Do Tradelines Work?

Although the term “tradeline” could refer to any account in your credit file, usually in our industry people use the word as shorthand for authorized user tradelines, or accounts on which you are an authorized user.

Credit card companies allow cardholders to add authorized users (AUs) to their accounts, which are people who are authorized to use the account but are not liable for any charges incurred. For example, a business owner could add an employee as an AU of their credit card, or a parent could add their child.

When someone is added as an AU, often the full history of the account is shown in the credit reports of both the primary user and the AU, regardless of when the AU was added to the account. Therefore, the AU may have years of credit history associated with the account reflected in their file as soon as they are added.

This is why obtaining an AU tradeline through a family member or friend is a common way for people to start establishing a credit history. In fact, studies estimate that 20%-30% of Americans have at least one AU account.

Why are authorized users able to share the benefits of the primary user’s credit rating, even though they are not liable for the debt? This policy is a result of the Equal Credit Opportunity Act of 1974 (ECOA).

Before ECOA was passed, creditors would often report accounts shared by married couples as being only in the husband’s name. This prevented women from building up a credit history and credit score rating in their own names, which in turn prevented them from being able to obtain credit independent of their husbands.

In response to this unequal treatment, ECOA was passed to prohibit discrimination in lending. The federal law made it illegal for creditors to discriminate on the basis of sex, marital status, race, color, religion, national origin, age, or receipt of public assistance.

This means that creditors may not consider this information when deciding whether or not to grant credit to an applicant or determining the terms of the credit.

ECOA was passed in large part to prevent creditors from discriminating against women and to provide equal credit opportunities to women.

Regulation B is a section of ECOA that specifically requires that creditors report spousal AU accounts to the credit bureaus and consider them when lenders evaluate a consumer’s credit history.

Generally, creditors do not distinguish between AUs that are spouses and those that are not when reporting to the credit bureaus, which effectively requires the credit bureaus to treat all AU accounts in the same way.

As a result of this policy, the practice of “piggybacking credit” emerged as a common and acceptable way for individuals with good credit to help their spouses, children, and loved ones build credit or improve their credit.

The practice of piggybacking is the foundation of the tradeline industry. In a piggybacking arrangement, a consumer pays a fee to “rent” an authorized user position on someone else’s tradeline. The age and payment history of that tradeline then show up on the consumer’s credit report as an authorized user account.

Are Tradelines Legal?

It is understandable that there is some confusion about this since not many people are aware of the idea of tradelines for sale, although the practice has been in use for decades.

While Tradeline Supply Company, LLC cannot provide legal advice, we can refer to several official sources, including the Federal Trade Commission, who have indicated that it is legal to buy and sell tradelines.

While tradelines are not illegal, historically, they have not been accessible to everyone. The high cost of tradelines meant that only the wealthy could afford to purchase tradelines for credit piggybacking. Today, however, innovations in the industry have lowered the cost of tradelines, making them affordable to a much wider audience.

Tradeline Supply Company, LLC is proud to be leading the tradeline industry in automating the process of buying and selling tradelines, offering some of the lowest tradeline prices in the industry, educating consumers on the credit system, and making tradelines accessible to everyone.

Our goal is to provide equal opportunities to those who do not have access to authorized user tradelines through friends and family by providing an online platform that allows for a greater network of connections.

But Didn’t Credit Card Piggybacking Get Banned?

Fair Isaac Corporation (FICO), the creator of the widely used FICO credit score, did try to change its scoring model to eliminate the benefits of authorized user tradelines, although they were ultimately unsuccessful. The firm announced that they were planning to devise a way to allow “real” AUs to keep the benefits of their AU tradelines while at the same time discounting the value of AU tradelines for consumers who FICO deemed to be “gaming the system.”

FICO admitted to Congress that they could not legally discriminate between AUs based on marital status due to ECOA.

While this statement understandably caused a lot of concern among consumers of tradelines, as it turns out, FICO was never able to implement this change in their scoring system.

At a congressional hearing in 2008, Fair Isaac’s president admitted that they could not legally distinguish between spousal AUs and other users, because discriminating based on marital status would unlawfully violate ECOA.

After consulting with Congress and multiple federal agencies, FICO was blocked from discriminating against AU account holders. Consequently, all AU accounts are still being considered in FICO 8, the most widely used credit scoring model.

In addition, studies have shown that accounting for AU data helps make credit scoring models more accurate, so it is actually in FICO’s best interest to continue including all AU accounts in their credit scoring models.

In working with thousands of consumers over the years, our results prove that in 2021, AU tradelines still remain an effective way to add information to an individual’s credit report, regardless of the relationship between the primary user and the authorized user.

Here’s another piece of evidence that proves that authorized user tradelines still work in 2021: many banks actually promote the practice of becoming an authorized user for the specific purpose of boosting one’s credit score. To see this for yourself, all you need to do is go to any major bank’s website and search for “authorized user.” You are almost guaranteed to see several articles pop up that talk about becoming an authorized user in order to build a credit history.

How Do We Know Tradelines Will Continue to Work in the Future?

Most widely used credit scoring models still include authorized user “piggybacking” accounts.

Given that FICO has already targeted the tradeline industry before, it makes sense to wonder whether tradelines will still work in the years to come if FICO eventually does succeed in coming up with a way to discriminate against certain AUs.

Thankfully, we can rest assured in knowing that the tradeline business will be around for a long time. The reason that we can be sure of this is that the credit industry is extremely slow to adapt, so even if FICO were to roll out a new credit score model that can tell which AUs purchased their tradelines, it would take years, if not decades, for this new credit score to be adopted across the entire financial industry. Let us explain why this is the case.

Credit scoring is a complicated process, and all lenders have their own guidelines when it comes to underwriting. FICO has many different scoring models, and the specific versions used to evaluate credit applicants vary widely between different industries and even between individual lenders within the same industry.

Currently, the three major credit bureaus (Equifax, Experian, and TransUnion) use the version called FICO 8, which debuted in 2008. Consequently, this is also the version that most lenders use for measuring consumer risk for various types of credit, such as personal loans, student loans, and retail credit cards.

However, according to FICO, the mortgage industry still relies on the much older FICO score models 2, 4, and 5. Auto lenders sometimes use FICO 8, while many still use FICO 2, 4, and 5. Credit card companies may use versions 2, 3, 4, 5, and 8.

As if this isn’t complicated enough, many lenders also use proprietary credit-scoring guidelines specific to their businesses. As FICO’s website says, “It is up to each lender to determine which credit score they will use and what other financial information they will consider in their credit review process.”

As you can see from the wide range of versions used, lenders are extremely slow to adapt to changes in FICO’s credit scoring model. In addition, their underwriting processes have been built around previous versions of FICO. All of the credit score data they have accumulated over time is only accurate for the particular version that was used to calculate it.

Transitioning to a completely new credit score model would require businesses to expend significant resources on updating their technological systems, collecting and analyzing new consumer data, training employees, and possibly incurring financial losses as a consequence of not being able to rely on the consumer data they collected while using older credit score models.

For these reasons, most lenders tend to be very reluctant to introduce the latest FICO credit scoring model.

Lenders use credit scoring models that are specific to their industries, so they tend to resist changing to newer models. Photo by InvestmentZen.

So, even if FICO were to successfully eliminate authorized user data in future credit scoring models, it is likely that it would take years or even decades for lenders to adapt to this change.

In addition, as the 2008 congressional hearing showed, FICO will face pushback from the federal government if they try to eliminate authorized user benefits again. It is highly unlikely that a large company like FICO would want to risk being shut down by the federal government for violating the law.

Consumers wouldn’t stand for it, either. In the Washington Post, J.W. Elphinstone wrote, “Other consumers besides credit renters stand to lose with the change, namely those for whom authorized user accounts were designed… there’s no way to distinguish these from the latest crop of strangers trying to augment their scores. Lenders who want to find out more information about others on credit card accounts are hindered by the Fair Credit Reporting Act and privacy laws.”

Final Thoughts

When FICO took the issue of piggybacking all the way up to Congress in 2008, they made headlines in their fight against the practice.

This was also during the same time that the subprime mortgage meltdown began which preceded the Great Recession. The entire mortgage industry had to be overhauled and many people assumed that the tradeline industry went down along with it.

What did not make headlines is that FICO’s push to do away with the authorized user tradeline industry actually failed due to the government upholding ECOA and the FTC affirming that the practice of buying and selling tradelines is allowed.

The banks themselves even promote credit card piggybacking among friends, family, and co-workers.

26 million consumers in America have no credit record whatsoever. On top of that, there are an additional 19 million consumers who do have credit files, but they do not contain sufficient credit information to be scored by a widely available credit scoring model. These consumers—in total making up nearly one in five American adults—are the “credit invisibles” and “credit unscorables.”

Due to a lack of credit history, these consumers are virtually invisible to the credit system. That means credit can be very hard or even impossible to obtain when it is needed. After all, we all know that “it takes credit to get credit,” since lenders often don’t want to take the chance of lending to someone with no prior credit record.

“Alternative data,” which involves using data sources other than traditional credit reporting information to make lending decisions, is a concept that is becoming increasingly popular as one possible solution to the problem of credit invisibility.

Let’s shed some light on the emerging topic of alternative credit data and how it could help or hurt consumers.

What Is Alternative Credit Data and How Does It Differ From Traditional Credit Data?

Traditional credit data refers to your credit report, credit scores, and the information they contain. In other words, traditional credit data primarily consists of information about how you manage your tradelines, which are the credit accounts you own.

When we are talking about credit, we are almost always discussing traditional credit data since that is what is used to make most lending decisions.

In contrast, alternative credit data is financial information about consumers that is not typically included in traditional credit reports. Examples of alternative credit data sources include rent payments, utility payments, full-file public records, and data from alternative financial service providers (ASFPs), such as payday lenders.

Traditional Credit Data

Alternative Credit Data

Contains information about the tradelines in your credit report

Information comes from other sources since there is insufficient credit data

Payment history for loans and credit cards

Data from alternative financial service providers (e.g. payday lenders)

Credit utilization ratio

Utility payment history

Delinquencies

Rent payment history

Credit mix

Consumer-permissioned data

Credit inquiries

Full-file public records information

What Is the Purpose of Alternative Credit Data?

Alternative data includes data that consumers may choose to allow credit reporting companies to access, such as bank account balances.

For the millions of consumers who lack credit reports based on traditional credit data, building credit and obtaining credit is a challenge. Without a verified credit history, lenders cannot make an informed decision about whether to extend credit to a consumer.

One way the credit scoring industry is trying to address this problem is by creating new types of credit scoring algorithms that utilize different sources of data that are not contained within a consumer’s traditional credit report but still have predictive power with regard to a consumer’s credit risk.

These alternative data sources, such as rent and utility bill payments, are more accessible and more commonly used among those who are credit invisible.

The idea behind alternative credit data is that a consumer’s non-credit financial information can still be used to predict whether the consumer is financially responsible and creditworthy. This information can help lenders provide credit to consumers who may have a thin credit file or no credit file at all but who may still be creditworthy.

Therefore, using alternative data to make lending decisions could theoretically allow lenders to expand their customer base and earn more revenue while providing more credit to consumers who lack a traditional credit history.

How Do Consumers Benefit From Alternative Data?

The benefit to consumers, of course, is that many consumers who may be creditworthy but are invisible to the traditional credit system could potentially use alternative data as a path to building credit where they lacked one before.

For example, a consumer who gets a good credit score using an alternative data scoring method might now be able to get approved for an unsecured credit card, whereas they might have had to put down a deposit to get a secured credit card if the lender had only been able to use traditional credit data. This would allow the consumer to hold onto the cash they would have had to put down as collateral and instead save it for emergencies or some other use.

Applications of Alternative Credit Data

Consumers who are “credit invisible” but have a history of being financially responsible in other areas may benefit from the use of alternative credit data.

Although alternative credit data is still a relatively new field, major players in the credit industry are already working on developing new credit scoring tools that make use of alternative data.

FICO XD and FICO XD 2

FICO is working on developing new credit scoring models that can reliably assess the credit risk of consumers who are unscorable using traditional credit scoring methods.

The FICO Score XD “leverages alternative data sources to give [bankcard] issuers a second opportunity to assess otherwise unscorable consumers.”

Nerdwallet reports that the FICO XD model uses phone, utility, and cable payment data as well as things like information about your home if you are a homeowner, occupational licenses you may have, and your bank records.

Compared to traditional FICO scores, this model has the same credit score range of 300 to 850 and the same expected credit risk for each score group within that scale.

According to FICO, the XD scoring model can provide a score for more than half of all credit applicants that had previously been unscoreable, which adds millions of consumers to the scorable population.

Although only about a third of applicants that can be scored with FICO XD receive scores higher than 620, which is considered to be fair credit, the company claims that almost half of borrowers with higher FICO XD scores later go on to obtain credit and achieve traditional FICO scores of 700 or greater.

FICO XD’s newer version, FICO Score XD 2, works similarly but has been further refined to provide more accurate results.

Similarly, the FICO Score X incorporates alternative data sources for credit scoring, such as telecom payments, mobile payments, “digital footprint” data, and even data from psychological surveys to provide a way for international lenders to score previously unscorable consumers.

UltraFICO

The UltraFICO score, currently being pilot tested by Experian, will use “consumer-permissioned” banking data to enhance its scoring capabilities. In this case, what that means is that consumers can choose to contribute data about their checking, savings, and money market accounts in order to allow lenders to assess their creditworthiness by looking at their overall financial profile.

Some of the specific financial factors considered by the UltraFICO score include:

A history of positive bank account balances is a beneficial factor with the UltraFICO credit score.

How long you have had your bank accounts open

How often you make banking transactions

When your most recent bank account transactions occurred

Verification that you often have money saved in your bank accounts

A history of having positive bank account balances

FICO says this credit scoring model can help increase access to credit for “nontraditional borrowers” who have limited credit histories, particularly young consumers, immigrants, and those who are rebuilding their credit after experiencing financial distress.

The company also states that UltraFICO could potentially improve credit access for most Americans and could be especially helpful for those whose credit scores are in the “grey area” of the upper 500s and lower 600s or those whose scores just barely miss a lender’s credit score cutoff.

Seven out of 10 consumers who have had consistently positive banking habits in the past three months could get a higher UltraFICO score than their traditional FICO score, according to the company’s website.

Experian Boost Credit Score

Experian has also come up with their own alternative data solution called Experian Boost, which is a free service that allows users to provide access to their bank accounts in order to get credit for their on-time payments of bills such as electricity, water, gas, phone plans, cable, and even Netflix.

One major advantage with Experian Boost is that it only counts positive payment history, so missed payments will not hurt your score. If the program detects that you have missed a payment, it will remove that account from your credit file so that the late payment will not hurt your score.

Experian Boost lets you add positive payment history from your utility bills and some streaming services.

The New York Times has reported that the reason why Experian Boost does not consider negative information about your bills is that anything negative on your record will most likely end up on your credit report anyway, either because your utility provider may start reporting it to the credit bureaus or the account may get sold to a collection agency which then reports the collection account.

In addition, Experian says that you can disconnect your bank accounts if your FICO score decreases because of Experian Boost and that you can always reconnect your account later once your finances have improved.

According to Experian, consumers who sign up for Experian Boost receive an average boost to their FICO score of 13 points. Those who do not see a boost initially may see a larger effect over time if they keep their account connected as the program continues to check your account for payments you made on time and adding those to your credit profile.

If Experian Boost helps your credit but you later decide for whatever reason that you no longer want to use it, be aware that the positive payment history that was helping you will be removed from your credit profile, so it’s likely that your credit score will fall.

TransUnion FactorTrust

In 2017, TransUnion acquired FactorTrust, a company that provides lending data on short-term and small-dollar loans (e.g. payday loans), which are not reported in traditional credit reports and are often utilized by underbanked and credit invisible consumers.

This information will allow TransUnion to assess credit risk for a larger group of consumers.

In addition, TransUnion says that their small-dollar loan data will help lenders comply with the Consumer Financial Protection Bureau’s recent changes to payday lending rules meant to protect consumers.

Equifax DataX

In 2018, Equifax acquired a specialty credit reporting agency and provider of alternative credit data called DataX. Equifax stated that they plan to use DataX to help lenders improve financial inclusion and access to credit, especially for consumers who are underbanked.

DataX claims that they can help lenders better evaluate the credit risk levels of prospective customers by utilizing a “massive, proprietary consumer database that provides valuable insights on consumers not covered by traditional credit information sources.” This database contains demographic, financial, and credit data on millions of consumers.

The Downsides of Alternative Credit Data

In theory, alternative data sounds like a promising solution to the credit catch-22 and the problem of credit invisibility. According to FICO’s white paper on the subject, the use of alternative data allows millions of previously unscorable consumers to achieve credit scores that are high enough to get access to credit.

However, while the credit scoring and credit reporting companies only talk up the positives of their alternative data products, there are some drawbacks to this approach that also need to be considered.

Alternative Data May Perpetuate Credit Inequality

Although alternative data is marketed as a solution to credit invisibility, it’s possible that it could actually worsen credit inequality.

Despite FICO’s impressive claims, in the company’s white paper, we can clearly see how alternative data in credit scoring might not be so helpful to many consumers.

According to their research, about a third of the “newly scorable” consumers scored 620 or above using the alternative data score. These are the millions of consumers they refer to that may now be able to access credit.

But if only a third of consumers scored 620 or above, that means two-thirds of consumers now fall below 620 with the alternative data score, which is considered bad credit. That means there are twice as many of the newly scored consumers who end up with bad credit than those who end up with good credit after the alternative data model has been applied.

In many cases, having bad credit is even worse than having no credit, because instead of starting from scratch, you have derogatory information on your credit report that is going to weigh down your credit score. This can make it even more difficult to get your credit to a good place than if you had started with no credit history at all.

The results of FICO’s alternative data research bear out the concerns presented by the National Consumer Law Center (NCLC). According to the NCLC, if utility payments become part of the credit reporting system, this could result in millions of consumers getting negative marks and would disproportionately impact low-income consumers and people of color.

Although alternative credit data is pitched as a way to lift millions of consumers out of credit invisibility, in reality, it is another profit-generating tool created by the credit scoring and reporting companies to sell to financial institutions. Any benefit or harm to consumers is incidental to the primary goal of the banks making more money by lending to more consumers.

As you know from our article, “What Happened to Equal Credit Opportunity for All?” the credit scoring system was built upon and continues to perpetuate a history of financial inequality in our country.

Unfortunately, although it has the potential to help millions of consumers if implemented in the right way, it seems likely that alternative credit data may just end up being used to continue the legacy of inequality and discrimination that is still firmly entrenched in the credit industry and in our society in general.

Data Privacy Concerns

Another major concern with alternative data is privacy. In recent years, major data breaches have been happening left and right, including the 2017 Equifax breach that compromised the information of around 148 million consumers. The credit bureaus have shown with multiple egregious security breaches that consumers cannot trust them to safeguard their personal information.

Experian Boost, as well as other similar “consumer-permissioned” data reporting systems, require users to allow access to their bank account in order to report bill payments. For many, it may be hard to stomach the idea of giving FICO or the credit bureaus access to their personal information when they have repeatedly mishandled sensitive consumer data. Those who do choose to use such services do so at the risk of their information potentially being compromised.

Some Lenders May Not Use Alternative Data Credit Scores

Since alternative credit data is still a relatively new development, one downside is that many lenders may not be using alternative data or credit scores based on it in order to make their lending decisions.

The credit industry is slow to change, as we talked about in “Do Tradelines Still Work in 2020?”, so it may take several years for alternative credit data to be widely adopted.

Therefore, at this time, there is no guarantee that your lender of choice will have the ability to access and use your alternative credit data.

Conclusion: Is Alternative Data Helpful or Harmful?

Alternative data has the potential to lift millions of consumers out of credit invisibility, which is a step toward providing equal credit opportunity to these consumers.

However, it has just as much potential to harm consumers and perpetuate credit inequality due to the issues we discussed above.

As with any credit reporting or credit scoring tool, we have to remember who these tools are designed for and who they are intended to serve: the banks.

Ultimately, the purpose of alternative credit data is to help lenders make more money by lending to a greater number of consumers. For consumers, the benefits and risks are not so clear cut.

If you have no credit record or a thin credit file, alternative credit data scoring systems may be worth considering and trying out. As with any major credit moves, be sure to do your due diligence as a consumer by researching how these programs work and how you can protect yourself and your credit if you do not get the results you are looking for.

What is your take on the issue of alternative credit data? Have you tried any of these alternative data services yourself? Drop a comment below to let us know your thoughts!

It’s a question we hear all the time from people who are new to the tradeline industry. Perhaps you have even asked it yourself. In this article, we explain how tradelines work and how they can affect your credit.

What Are Tradelines to Your Credit?

While the term “tradeline” simply means any credit account, in our business, it usually refers specifically to authorized user (AU) tradelines, or authorized user positions on someone’s credit card. An AU tradeline is an account on which you are designated as an authorized user, which means you are not liable for the charges incurred on the account. However, the tradeline can still affect your credit file.

How Do Tradelines Work?

When someone is added as an authorized user to someone else’s account, often the full history of the account is then reflected in the records of both the primary account holder and the AU. This is because credit records do not report the date the AU was added to the account. So, as soon as the AU is added, their credit report may begin to show years of history associated with the account.

Therefore, authorized user tradelines can be used as a way to add credit history to someone’s credit report.

One common example of this is when a parent designates their child as an authorized user of one of their credit cards as a way to help them start building credit early in life. In fact, this practice of building credit as an authorized user, often called “credit piggybacking,” is frequently promoted by banks and financial education sites.

What Are Tradelines Used For?

Parents often use piggybacking as a strategy to help their children build credit early in life.

As we mentioned, tradelines can add years of credit history to your credit report. The power of a tradeline is always relative to what is already in your credit file, so if you are interested in building credit as an authorized user, make sure to choose a tradeline that surpasses what you already have in your credit profile.

How Do Tradelines Affect Your Credit?

Adding quality tradelines to your credit file can influence many of the variables that are related to your credit, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more.

The most important factor that tradelines bring to the table is age, because with age also comes perfect payment history. These two factors combined are the most significant influence on one’s credit.

Due to the power of these factors, adding AU tradelines to your credit file is often preferable over opening new primary tradelines. This is because new primary tradelines will have no age and will probably have relatively low credit limits, which can drag down important metrics in your credit file.

Authorized user tradelines, which are authorized user positions on someone’s credit card, can be used to build credit history.

In contrast, authorized user tradelines already have significant age and high credit limits.

Can You Buy Tradelines?

The tradeline industry took this concept of “piggybacking credit,” as it is often called, and created a marketplace where tradelines could be bought and sold. Essentially, people who want to add tradelines to their credit file can pay a fee to be an authorized user on someone else’s credit card, even if the two parties are complete strangers.

Tradeline companies serve as the intermediary, protecting the privacy of both the cardholders and the authorized users and facilitating the transaction.

A marketplace now exists where consumers can pay a fee to piggyback on others’ tradelines as authorized users.

Tradelines have been around since the advent of the modern credit system. Virtually as long as credit cards have existed, people wanted to be able to share access to their account with others, such as spouses, children, or employees.

However, the role of authorized users was not always considered equally by the credit bureaus. Until the Equal Opportunity Credit Act of 1974, creditors often used to report accounts that were shared by married couples as being only in the husband’s name. This prevented women from building up a credit history in their own names.

In response to this unequal treatment, ECOA was passed to prohibit discrimination in lending.

Regulation B is a section of ECOA that requires creditors to report spousal AU accounts to the credit bureaus and consider them when evaluating credit history. Since lenders generally do not distinguish between AUs who are spouses and those who are not, this effectively requires that credit bureaus must treat all AU accounts the same.

The Equal Credit Opportunity Act prohibits credit discrimination.

It was as a result of this policy that the practice of “piggybacking credit” emerged as a common and acceptable way for consumers with good credit to help their spouses, children, and loved ones build credit.

Thanks to ECOA, authorized user tradelines are still weighted very heavily in credit scoring models.

For more on the history of AU tradelines and the policies and regulations that govern our industry, read our article, “Do Tradelines Still Work in 2019?”

Are Tradelines Legal or Illegal?

While Tradeline Supply Company, LLC does not provide legal advice, we can answer this common question by referring to official proceedings and statements from the authorities.

The issue of tradelines and credit piggybacking went all the way up to the U.S. Congress in 2008, when FICO tried—unsuccessfully—to eliminate authorized user benefits from its credit scoring model. They ultimately reversed their stance and decided to keep factoring AU benefits into credit scores thanks to the Equal Credit Opportunity Act of 1974.

The Federal Trade Commission and the Federal Reserve Board have also weighed in on this topic. In 2010, the Federal Reserve Board conducted a large-scale study on piggybacking and found that over one-third of the credit files that could be scored had at least one AU account in their credit profile, which shows that piggybacking credit is an extremely common practice.

After the issue of piggybacking credit was discussed in Congress, FICO admitted that it could not legally eliminate authorized user benefits.

Learn more about your legal right to use authorized user tradelines in our article, “Are Tradelines Legal?”

How Do I Add Tradelines to My Credit Report?

To add tradelines to your credit report, you can either open your own primary accounts or you can be added as an authorized user to someone else’s credit account. For many people, it is difficult to start building credit on their own because creditors are hesitant to lend to someone with no credit history, which is why the authorized user route is an appealing option.

If you are seeking to add authorized user tradelines to your credit report, you can either ask someone you trust to add you to one or more of their accounts or purchase tradelines from a tradeline company. The benefit of buying tradelines as opposed to asking for a favor from someone you know is that all of our tradelines are guaranteed to have perfect payment histories and low utilization.

How Much Does It Cost to Buy Tradelines?

Our tradelines range in price from $150 to around $1,500 depending on two main variables:

The tradeline’s age

The tradeline’s credit limit

Our tradelines stay on your credit report for about two months.

Generally, the older the tradeline is and the higher the credit limit is, the more powerful it will be and the higher the price will be (and vice versa). We delve into further details and examples of the cost of tradelines on our FAQ page, “How Much Do Tradelines Cost?”

How Long Does a Tradeline Stay on Your Credit Report?

Our tradelines stay on your credit report for two reporting cycles, which is approximately two months.

After the two months of being an active authorized user is complete, you will be removed from the account and the tradeline will then appear as closed. A closed tradeline will often remain on your credit report for several years.

However, your strategy may vary depending on your specific goals. There are some situations in which the credit limit can be more important. Our in-depth tradeline buyer’s guide that has all the information you need to help you choose a tradeline.

In choosing the right tradelines for you, It is helpful to be able to calculate how a tradeline could affect your average age of accounts and utilization ratios. Try out our custom tradeline calculator, which does the math for you!

How many tradelines you need depends on your specific situation. There are different cases in which buyers may want to get two or three tradelines, or sometimes even more, but there are other cases in which one tradeline will suffice.

If you really want to maximize your results and you have the budget to do so, buying multiple high-quality tradelines is the way to go. However, if you have budget constraints to deal with, it is usually best to focus your resources on one excellent tradeline.

Historically, only those with privilege and wealth have been able to use the strategy of credit piggybacking. Those who do not have family members with good credit to ask for help, or could not afford the high cost of tradelines, had nowhere to turn, so their options for building credit are often extremely limited and very costly.

To us, it does not seem fair that some people have the option of credit piggybacking but others do not. By offering tradelines at affordable prices, we aim to bridge this gap and help provide a chance at equal credit opportunity for all.

With the recent killings of yet more Black people at the hands of police, the long-held rage and grief of America’s Black communities have boiled over into nationwide civil unrest and protests demanding justice, equality, and the end of police brutality.

As our nation collectively reckons with its history of slavery and its legacy of violence toward Black people that continues today, we want to shed some light on the economic inequalities faced by Black Americans.

We do not pretend to have all the answers or solutions to these large, structural issues that are deeply embedded within the fabric of American society. However, we feel that it is our responsibility to provide educational resources on these topics so that each citizen can understand the issues we are facing and make informed decisions about how to combat inequality in our own lives and in our society as a whole.

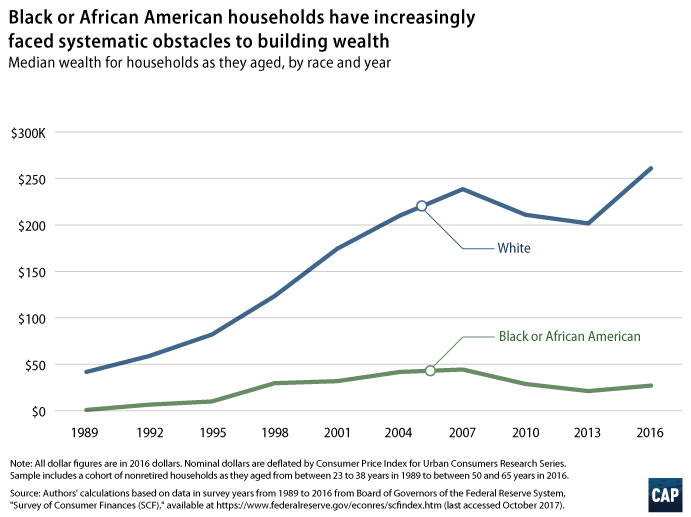

The Racial Wealth Gap

Get ready for this staggering statistic: according to data from the Federal Reserve, the typical Black household has only about 10 cents for every dollar of wealth held by the typical White household.

According to the U.S. Joint Economic Committee, Black Americans are more than twice as likely to live below the poverty line as White Americans, with Black children, in particular, being three times as likely to live in poverty as White children.

Not only that, but the chasm between Black and White household wealth, instead of getting smaller, is actually getting wider and wider over time, even for Black Americans with higher education.

This chart from the Center for American Progress shows the racial wealth gap widening over time.

Origins of the Racial Wealth Disparity

The racial wealth gap in America has existed from the moment that the first Africans were taken from their land and brought to the colonies in 1619.

For over two and a half centuries, enslaved Black people were used as a source of wealth by White enslavers who claimed them as property, but they had no way of accumulating wealth for themselves. They were forced to work for nothing and were not allowed to keep any of the wealth they generated.

Even after slavery was legally abolished in 1865, that certainly did not create a level economic playing field.

For at least another century, various laws and policies continued to block Black people from attaining wealth, and discrimination is still pervasive today.

Government-Sanctioned Housing Discrimination

Take the National Housing Act of 1934, for example. Passed in the wake of the banking crisis that kicked off the Great Depression, this act created the Federal Housing Administration (FHA). The FHA made it easier for White Americans to afford homes by providing mortgage insurance to protect mortgage lenders from borrower defaults.

Unfortunately, the FHA outright refused to insure loans to Black consumers and even consumers who wanted to live in areas near Black neighborhoods. This practice of “redlining” not only restricted where Black families could buy homes, but it also affected the types of funding they could get and the terms of those loans. (Without FHA insurance, Black home buyers were forced to accept inflated prices and fees as well as predatory contracts pushed by deceitful contact sellers.)

Furthermore, it discouraged investment and development in primarily Black areas, which led to the decline of many communities and of property values in those areas.

While many White families were buying up houses using government-sponsored, low-interest mortgage loans, Black families did not have this luxury, which meant they were shut out of an important opportunity to accumulate wealth in the form of home equity.

Ultimately, the racial wealth gap cannot be explained or fixed by the behaviors or decisions of individual Black people. It is the result of 400 years of structural racism and oppression in America, and solving it likely requires dramatic and large-scale policy changes.

The Federal Housing Administration insured mortgages to help make it more affordable for consumers to obtain mortgages and purchase homes—but only for White Americans.

Employment

The rate of unemployment of Black people is twice as high as the unemployment rate of White people.

Racism and prejudice undoubtedly play a significant role in this, as research has shown that Black people today still face the same amount of hiring discrimination that they did in the 1980s.

The Center for American Progress wrote the following in 2011, when the economy was starting to slowly recover from the Great Recession; however, the information unfortunately still holds true today in 2020, especially in the midst of the COVID-19 recession:

“The unemployment rates for African Americans by gender, education, and age are much higher today than those of whites, and these unemployment rates for African Americans rose much faster than those for comparable groups of whites during and after the Great Recession. The unemployment rates for many black groups in fact continued to rise during the economic recovery while they started to drop for whites…It is now painfully clear that African Americans are still facing depression-like unemployment levels.”

“…there are unique structural obstacles that prevent African Americans from fully benefiting from economic and labor market growth—obstacles that deserve particular attention when unemployment rates for African Americans stand at the highest levels since 1984.”

In addition, Black workers are more likely than White workers to have low-wage jobs, which leads to Black families having lower average incomes than those of White families. White annual household incomes are about $29,000 higher than Black annual household incomes.

People of Color Are Bearing the Brunt of the Recession

It is impossible to ignore the effects of the economic recession that has begun as a result of the COVID-19 pandemic, which is disproportionately impacting Black and Hispanic communities, just like the Great Recession did in 2007 – 2009.

Job Loss

Pew Research Center reports that Hispanic and Black adults are being the most affected by the loss of millions of jobs due to the coronavirus.

This is primarily because people of color are overrepresented in many low-wage jobs within the industries that have had to shut down during the pandemic, such as food service, retail, and hospitality. These are also jobs that cannot be done remotely. Consequently, Black employees are especially vulnerable to being laid off.

Furthermore, not only are Black workers often the first to be let go during recessions, but they are often the last to be re-hired when the economy recovers. According to the Center for American Progress, it’s important to recognize “…that black labor market prospects are hit much harder by recessions and that it takes longer for African Americans to recover from an economic downturn.”

Business Closures

A study from the Stanford Institute for Economic Policy Research on the impact of COVID-19 on small business owners revealed that the percentage of Black-owned small businesses that have been forced to close due to the pandemic (41%) is more than twice the percentage of White-owned businesses that have closed for the same reason (17%).

The Paycheck Protection Program, which is part of the CARES Act, was intended to “provide small businesses with funds to pay up to 8 weeks of payroll costs including benefits.” However, some have pointed out that the program is likely to be perpetuating racial inequality by giving the role of distributing funds to banks that have a demonstrated history of discrimination against Black borrowers.

Housing Insecurity

Evictions have been temporarily paused in many areas since many renters have lost their jobs during the pandemic and can not afford to pay rent. Once these eviction bans are lifted, however, it is predicted that Black and immigrant tenants will make up the majority of those displaced by the coming housing crisis.

According to Politico, “Black and Latino people are twice as likely to rent as white people, so they would be most endangered if the protection from removal is ended.” Furthermore, Black and Latino households usually spend a greater portion of their income on rent than White renters. Any disruption in income could spell disaster for these vulnerable groups of tenants.

Poor women of color, specifically, are much more vulnerable to eviction than any other demographic group, with one in 17 being evicted each year, compared to only one in 150 for poor White women.

The consequences of having an eviction on your record are severe. It can be nearly impossible to find safe and affordable housing since many landlords refuse to rent to tenants who have previously been evicted. This leads to many low-income Black women being forced into homelessness and dangerous living conditions.

If the landlord passes the bill for unpaid rent onto a debt collector, then it becomes a collection account, which shows up on your credit report and can heavily impact your credit for up to seven years. Similarly, if a landlord seeks a court judgment against you for unpaid rent, the judgment could appear in the public records section fn your credit report.

Credit Difficulties

With less wealth and lower average incomes than White households, Black and Hispanic households are less equipped to weather financial emergencies without getting behind on bills, which is the number one cause of bad credit.

A recent Pew Research study determined nearly half of Black adults surveyed reported that they are worried about not being able to pay all of their bills over the next few months.

For a list of tips and resources on getting through the COVID-19 pandemic with your finances and your credit intact, even if you are having a hard time paying your bills, read “How to Protect Your Finances and Credit During the Pandemic.”

Medical Debt

It is well known that many Black communities deal with higher pollution levels and “food deserts” where access to affordable, healthy foods is often not possible.

And since Black Americans are more than twice as likely to be in poverty than White Americans, they are therefore more likely to experience food insecurity, inadequate nutrition, a lack of healthcare, and the stress of constantly worrying about money on a daily basis.

All of the stressors listed above have been shown to have lifelong consequences on the physical and mental health of poor people, including strong negative effects on the immune system. This means low-income individuals (especially low-income people of color, who also suffer from the effects of “weathering”) are less able to fight off infections and more likely to live with various chronic illnesses that can make the coronavirus more deadly.

As we mentioned, Black workers are overrepresented in lower-wage jobs and more likely to get laid off, which puts them at risk of losing their health insurance coverage or, often, not even having access to health insurance in the first place.

When you put all of these factors together, it creates the perfect storm for Black individuals to get sick with COVID-19, suffer more severe complications that could lead to being hospitalized, and not have the resources to cover extremely expensive hospital stays.

Even if the illness is less severe for some, who may be able to recover after staying at home for a few weeks, they still have to deal with the high cost of missing work while sick and isolated at home. Losing out on even one paycheck can be devastating for low-income households who have not had the option of building up savings.

Naturally, when you combine serious illness with no health insurance and no safety net, the result is massive medical debt. Research has shown that Black Americans are 2.6 times more likely to have medical debt than White Americans and are also nearly twice as likely as White people to be contacted by debt collectors and to borrow money due to medical debt.

When consumers cannot afford to service their medical debt, or if they have to stop paying other bills in order to be able to make their medical debt payments, they will inevitably end up missing payments, defaulting on debts, having accounts go into collection, and possibly even filing for bankruptcy in extreme cases.

All of these derogatory items are severely damaging to one’s credit and therefore tend to make credit more expensive and less accessible to consumers who struggle with medical debt. This impact is long-lasting since negative information stays on your credit report for seven years or even up to 10 years in some bankruptcy cases.

For those who cannot afford adequate healthcare, getting sick depletes scarce resources, limits future opportunities, and stunts financial growth for many years, thus continuing the downward financial spiral.

Racial Disparities in the Credit System

Since race and ethnicity are not legally allowed to play a role in credit scores, you might think that consumers of all races would have equal opportunity in the credit system. Unfortunately, however, this is not the case.

Black and Hispanic consumers, on average, tend to have lower credit scores than non-Hispanic White and Asian consumers, even after controlling for other variables such as personal demographic characteristics, location, and income.

Black borrowers pay higher interest rates on auto loans and other installment loans than non-Hispanic White borrowers who have the same credit score.

Black and Hispanic consumers experience higher denial rates than other groups with the same credit score.

Black and Hispanic Americans are more likely to be credit invisible (lacking a credit record) than White and Asian Americans—15% of Black and Hispanic consumers lack a credit record, compared to just 9% of White and Asian consumers.

Black and Hispanic consumers are also more likely than White consumers to have credit records that cannot be scored by widely used credit scoring models—13% of Black adults and 12% of Hispanic adults are unscorable, versus only 7% of White adults. (The Consumer Financial Protection Bureau (CFPB) did not provide the percentage of Asian consumers who cannot be scored but said that “the rates for Asians are almost identical” to those of White consumers.)

Since credit invisibility and unscorability are more common among Black consumers, it should not be surprising to learn that Black households are more than twice as likely as White households to use payday lending. Payday loans are an expensive and usually predatory type of credit, in contrast to traditional sources of credit, such as banks, credit unions, and credit card issuers.

Credit Options Are Limited by Circumstances

In our credit system, there are some people who have the privilege of starting out with good credit and stable finances simply due to the circumstances they were born into, while many others are not so fortunate.

As we talked about in our article about equal credit opportunity, there are five main factors, referred to as the “five C’s,” that influence a borrower’s performance when it comes to paying back debt:

Capacity: the amount of income that is available to pay off debts

Collateral: the value of assets backing a loan, such as your car or your house

Capital: the value of assets that do not explicitly back a loan, but may potentially be used to repay it

Conditions: events that can disrupt a borrower’s income or create unexpected expenses that affect a borrower’s ability to make loan payments, such as a job loss

Character: the financial knowledge, experience, and/or willingness of a borrower that is relevant to their ability to manage financial obligations

As much as some people may like to believe that getting good credit is simply a matter of determination and hard work, in reality, each of the five C’s is subject to external forces and influences that may be beyond the control of the borrower.

When it comes to your capacity to pay off debts, for example, your income may be limited by the availability of jobs where you live and the types of jobs you can qualify for. Hiring discrimination and other challenges prevent many Black individuals from earning to their full potential, which results in a reduced capacity to pay off debt compared to White folks.

In order to have collateral and capital, you need to have valuable assets, which is a privilege that not everyone enjoys.

A borrower’s “character” depends on their upbringing and education, which for many people does not include adequate financial education.

And while anyone could be faced with unexpected conditions that may lead to financial hardship, people who are financially and socially privileged are in a much stronger position to recover, while others who are less fortunate could face financial ruin from even a single emergency.

Lacking Access to Credit Has Consequences

The reality in our country is that centuries of systemic inequality continue to have an impact on all of these five C’s in countless ways, which contribute to higher rates of credit invisibility and poor credit in Black communities.

As the CFPB states, “…the problems that accompany having a limited credit history are disproportionally borne by Blacks, Hispanics, and lower-income consumers.”

For example, data show that 42% of consumers in communities of color have debt in collections, compared to only 26% of consumers in White communities. Delinquency rates or default rates for medical debt, student loan debt, auto loans, and credit card debt are higher for communities of color across the board.

This makes a lot of sense when you think about the fact that Black and Hispanic borrowers have lower incomes and less wealth that they can use to service their debts compared to White borrowers.

The consequences of these disparities are far-reaching. Here are just a few of the repercussions of having no credit or bad credit:

It is more difficult to obtain credit, from credit cards to installment loans.

Credit is more expensive—it comes with higher interest rates and fees and may require a larger down payment or security deposit upfront.

Insurance rates may be more costly for those with bad credit.

It may affect your employment opportunities since surveys have shown that around 20%-25% of employers conduct credit checks as part of the hiring process for some positions.

Who Has the Privilege of Receiving Financial Support From Others?

Perhaps another “C” could be added to the list: community.

Often, the difference between good credit and bad credit or no credit at all often comes down to having a strong financial support network.

If you think about the five C’s of credit performance (capacity, collateral, capital, conditions, and character) we described above, each factor can be influenced or controlled by the financial resources available to you within your social circle.

According to the Urban Institute, “Financial support received can be saved or invested in an education or a home and it can be used to cover unexpected costs, helping families remain stable through financial emergencies.”

Having been deprived of generational wealth for centuries, Black households have fewer financial resources to draw on when a friend or family member is in need, and they receive less financial support from those in their networks compared to the amount of support that White families receive.

The Federal Reserve reports that while 71% of White Americans say they would be able to get $3000 from friends or family if they needed to, only 43% of Black Americans could say they would be able to do the same.

Another example of uneven access to financial support by race has to do with large monetary gifts and inheritances. The same report by the Urban Institute quoted above states that Black and Hispanic families are five times less likely to receive large financial gifts or inheritances than White families. For those who do benefit from large gifts and inheritances, Black families receive an average of $5,013 less than White families. It is estimated that this disparity explains 12% of the racial wealth gap.

From these examples, we see how a person’s family connections can enhance their access to capital and collateral, which can then make it easier to obtain and successfully pay off credit obligations. Conversely, not having access to those resources and possibly even having to support your own friends and family makes it much more difficult to manage debt.

An article in Forbes about the racial wealth gap summed it up well: “Those who have neither emergency savings nor flush friends and family to tap are more likely to take high-rate loans from payday lenders, skip needed medical care, fall behind on rent, mortgage or other bills or even have trouble paying for food.”

Piggybacking for Credit: Only for “Friends and Family”?

Being part of a privileged community does not only make it easier to access capital. It also means that you may be able to acquire a positive credit history before you have even used credit or opened your own primary accounts, thanks to the help of friends or family.

Achieving good credit early on in life is often the result of having friends and family members who also have good credit and who can share their positive credit history with someone who is just starting out. This process is called credit piggybacking because you can “piggyback” on someone else’s good credit in order to build up your own credit profile.

Ways to piggyback for credit include opening an account with a cosigner or guarantor, opening a joint account with someone who has good credit, or becoming an authorized user on someone else’s tradeline. Becoming an AU on a seasoned account is usually the preferred method for building credit fast because you can add years to your credit history simply by being added to the account, whereas the other methods involve opening a new primary account and waiting for it to age.

Unfortunately, when it comes to credit piggybacking, we see the same patterns of inequality along racial lines.

Many Consumers Are Already Benefiting From Credit Piggybacking

A study on AU accounts conducted by the Federal Reserve Board revealed that over a third of scoreable consumers in the United States have at least one AU tradeline in their credit profiles.

However, when the prevalence of AU tradelines is broken down by race, twice as many White consumers have AU accounts as Black consumers: only 20% of Black consumers have AU accounts, compared to 40% of White consumers.

In addition, the statistics showed that Black individuals have fewer AU accounts, on average, than White individuals, and when Black consumers do have AU tradelines in their credit profiles, the tradelines have less age and higher utilization rates of the tradelines held by White consumers.

What About “Equal Credit Opportunity”?

Despite the fact that one in three scorable consumers in our nation are already taking advantage of authorized user tradelines, there are still some who oppose the tradeline industry because they feel that those who purchase tradelines are “cheating the system.”

Yet these same people and institutions usually have no qualms about recommending that parents help their children build credit by allowing their children to be authorized users on their credit cards, or that a spouse who has good credit designates their partner as an authorized user for the purpose of building credit.

Most, if not all, of the big banks promote this strategy, often even explicitly saying that the authorized user does not need to be given the card to use, which makes it clear that it is solely for the purpose of getting that tradeline to appear on the authorized user’s credit profile.

As you can see, just like in many other aspects of our society, there is a double standard when it comes to who is “allowed” to benefit from AU tradelines.

While the banks publicly encourage their customers and their customers’ “friends and family” to use this credit-building tactic, they also claim that this opportunity should not be available to others who turn to the tradeline industry because they simply do not have the option of going to family or friends for credit help.

It does not seem fair or equal to promote a powerful credit-building strategy for those who are already privileged enough to have support from their social network while at the same time saying that it is wrong or should not be allowed for those who have fewer opportunities to get ahead.

How Can We Create Equal Opportunity for All?

Unfortunately, the racial economic divide in this country runs deep, as it has been perpetuated by American systems for generations.

For this reason, Black consumers disproportionally struggle with low incomes, less wealth, poor credit or no credit, and fewer opportunities to get ahead in life financially. This makes it more difficult to simply pay the bills and stay afloat, let alone to save money, invest in assets, and build wealth.

So what can we do to start to bridge the divide?

To address the disparity fully, it’s clear that large-scale economic policy changes on a national level will be needed.

The actions of individual consumers and businesses, while they cannot solve the problem as a whole, can help people take steps to improve their finances and credit.

Education on the Credit System and Personal Finance

Sadly, basic financial education is not something that most people are exposed to, neither in school nor at home.

Research is mixed on the topic of whether enhanced financial education in school would significantly help with the issue of economic inequality in our country. However, it can make a big difference to individuals to educate themselves on money management and the credit system and become empowered with this information to make better financial decisions.

We understand the importance of being educated about credit, knowing what the weaknesses in the credit system are, and understanding the steps you need to take to improve your credit. When you become familiar with how the credit system works, you have more power to make it work for you, instead of the other way around.

You can start taking control of your financial future with the knowledge and the power of these resources at your fingertips.

Tradelines and Equal Credit Opportunity

For those who lack a positive credit history, there are not many options to get started on building their credit profile, since most lenders base their decisions on your credit score and your track record of successfully managing credit in the past. Just like trying to get a job with no work experience, It can seem nearly impossible to get credit if you have not already had experience with credit before.

This is why we are so passionate about what we do at Tradeline Supply Company. We fill the void that so many consumers are looking for in their quest to start building or rebuilding their credit.

Our goal is to help create equal opportunity by making tradelines affordable and accessible to all consumers, not just the wealthy and the privileged.

Conclusion

While the wealthy have always had easy access to credit and strategies for building credit, the same cannot be said for the many people in America who are on the other, less fortunate side of the massive wealth gap.

At the same time, income inequality and the racial wealth gap keep growing larger, leaving more and more people behind who are struggling to build credit, manage their finances, and create a strong financial foundation for themselves and their families.

Systematic, government-legitimized discrimination against Black folks deprived Black communities of the opportunity to grow and thrive economically for hundreds of years. To this day, even though we claim to value equality, there are serious financial disparities in our systems that Black families bear the brunt of.

Although we alone cannot repair this injustice, we will continue to do our part in helping to provide equal opportunity to all consumers and create a more level playing field in our economy.

Equality, fairness, and justice are all concepts that the United States promotes as some of its highest values.

In reality, the history of our country and society has not always lived up to those values. In fact, our history has proven to be so far from those ideals that we do not even need to mention how far off our society has been in our not so distant past.

Fast forward to now, and many people may believe that our country has worked out all those unfair and unequal practices. But the truth is that in our capitalist society, powerful private institutions provide the backbone of our economy, and the facts paint an interesting picture of how our financial systems really operate.

Do Credit Scores Actually Work?

For decades, lenders have been relying on automated underwriting tools that are largely or entirely based on the contents of one’s credit report. Do these tools succeed at their goal of accurately determining the creditworthiness of consumers?

What Do Credit Scores Do?

A credit score is a number that is supposed to symbolize the credit risk of a consumer. The scale usually ranges from 300 to 850, with lower scores indicating that you have a high risk of defaulting on a loan and higher scores indicating that you have a low risk of defaulting. Generally, credit scores that fall below 579 are considered bad credit, while scores that exceed 670 are considered good credit, and 850 is a perfect credit score.

Each type of credit score, such as a FICO Score or a VantageScore, has a different mathematical formula that uses the data in your credit report to produce your score, which represents the statistical likelihood of you defaulting in the future. The specifics of the credit scoring algorithms are trade secrets, so information about how exactly they work is not available to the public.

Credit Scoring Models Are Flawed

It is estimated that one-fifth of consumers have at least one error on their credit report that has the potential to make them look riskier than they are, which could result in higher interest rates, less favorable loan terms, or being denied credit. In other words, millions of people are negatively affected by inaccurate information on their credit reports.

Furthermore, it is well-known that in our credit system, consumers are rewarded for having debt and penalized for paying in cash, because taking on debt is one of the primary ways of establishing a payment history. You would think that being burdened with more debt would make you a higher credit risk, yet credit scoring models are designed to reward this behavior.