Using a credit card is easy — you use the card to buy things and then pay the credit card bill.

A credit card can sometimes be difficult, however, when dealing with your credit file.

From a missed payment to a loan that isn’t yours that’s incorrectly listed on your credit report, there are all kinds of ways your credit score can drop.

And not all of them are from something you did wrong.

What Is the Fair Credit Reporting Act?

Consumers have protections under the law regarding their credit reports — which is where credit scores and credit problems are listed for lenders to check before offering you credit.

Errors on a credit report can drop your credit score, making it harder to get a loan, credit card, rent an apartment, or qualify for insurance coverage, among other things.

The main law that protects consumers from credit errors is the Fair Credit Reporting Act, or FCRA.

Your Rights Under The FCRA

Here are some of the rights you have under this law and how to use it to protect your credit:

View Credit Reports

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months.

You can do one check every four months from each of the three — Equifax, Experian, and TransUnion — if you really want to be on top of it.

Start by going to AnnualCreditReport.com to request your credit file online.

Only use that website and don’t use a copycat site that charges fees for what should be a free service.

You’ll need to verify your identity to get online access. You can also request your credit file through an automated phone system or the mail.

The FCRA applies to all consumer reporting agencies.

You can also look at reports from other consumer reporting agencies that collect noncredit information about you.

These include rent payments, insurance claims, employers, and utility companies.

The Consumer Financial Protection Bureau lists the reporting companies and how to request a free report from each.

DISPUTING ERRORS

Getting a credit report in your hands can lead to all sorts of eye-opening concerns. Anything that’s listed as negative should be checked for accuracy. Here are some things to look out for:

Eviction that wasn’t legal.

Creditor listed that you didn’t have an account with.

Loan default.

Wrong name.

Wrong address.

Wrong Social Security Number.

Incorrect loan balance.

Closed account reported as open.

A loan you didn’t initiate.

Some errors may be simple to resolve and others you may need to do more research on before disputing them to ensure they’re incorrect.

For example, you may not recognize the name of a creditor and assume you don’t have an account with them. But it may just be a store credit card you recently applied for that is listed by the issuing bank’s name. Or maybe a home or auto loan was sold to a new loan servicer.

Other errors could be reason to suspect identity theft, or there could just be wrong information that’s bringing down your credit score.

If you suspect identity theft, such as someone taking out a credit card in your name, then file a police report and report it to your credit card company and the credit reporting agencies.

To dispute erroneous information, use certified mail to send the credit bureau a letter and copies of documents explaining the error. If a loan still shows an outstanding balance and you have written proof that it was paid off, for example, send a copy to the credit agency.

Credit agencies have 30 days to investigate and respond to your dispute, unless they deem it frivolous.

If it corrects an error, it must send you a free copy of your credit report through AnnualCreditReport.com so you can see that the corrections have been made.

Check Your Credit Score

The law allows you to request a credit score, though it’s legal for credit agencies and other businesses to charge you a fee for this service.

Some credit cards provide scores for free, so check with your credit card issuer first.

A credit score isn’t the same as a credit report.

Information in a credit report determines a credit score, and each credit bureau can use a different scoring model that requires it to provide different information.

You have different credit scores, depending on which factors are weighed more heavily.

Monitoring your credit is vital. Make sure that you review your credit report for any inaccuracies.

Know Who Can View Your Credit Report

The FCRA doesn’t allow a credit reporting agency to share your credit file with someone who doesn’t have a valid need.

Some inquiries, such as from a potential employer or landlord, require your written consent.

And, they can only check your credit report, not your credit score.

The credit reporting agencies can share your credit report for legitimate reasons, such as when you’re applying for credit, insurance, housing, or with a current creditor.

A Time Limit To Negative Information

The FCRA doesn’t allow credit bureaus to report negative information that’s more than seven years old, though it allows some forms of bankruptcy to remain on a credit report for 10 years.

There’s also a time limit for positive credit information such as on-time payments and low balances — up to 10 years after the last date of activity on the account.

Rejections Based on Credit Report

If your application for credit, job, insurance, or housing has been denied because of information in your credit report, the law gives you the right to know this information.

The landlord, employer or other entity that denied your application must notify you and give you the name, address and phone number of the credit reporting agency that provided the information.

The FCRA allows you to get a free copy of your credit report from that reporting agency within 60 days of the action against you. That’s in addition to the three free credit reports allowed annually.

To best deal with a potential rejection ahead of time, it’s smart to check your credit report before applying for credit, rental unit or related use of your credit report and check it for errors. Give yourself enough time to fix them.

The vast majority of lenders use your FICO credit score to evaluate your credit risk as a consumer when they are deciding whether or not to extend credit to you. And yet, historically, it has been costly for consumers to access their own FICO scores.

Popular websites such as Credit Karma and Credit Sesame offer free credit scores, but the scores provided are usually VantageScores, not FICO credit scores.

Knowing your VantageScore is still valuable information, but it is not directly tied to your FICO Score, so it is less useful when it comes to preparing to apply for credit. While it is often true that a consumer’s FICO score is similar to their VantageScore, in some cases, they may be vastly different, especially depending on which credit scoring models are used and which credit bureaus are providing the credit report information.

If you need to check your FICO score, where can you do so without paying a fee to access it?

Here are some of the best places to get your FICO score for free.

Your Credit Card Issuer

Several major credit card issuers now offer consumers the ability to check their FICO scores for free.

Discover Bank

Discover offers a free way to check your FICO score with their Credit Scorecard program. Even consumers who do not have a relationship with Discover Bank can freely use this feature.

Experian provides the credit report data that is used to calculate your FICO score. Your credit score updates once every 30 days and Discover notifies you when it is time to check your new FICO score.

In addition, Discover’s FICO Credit Scorecard keeps track of your credit score history so you can see how it changes from month to month.

The Credit Scorecard also provides a summary of what is going on with each of the five credit score factors that are influencing your FICO score: your payment history, credit utilization, length of credit history, mix of credit, and new credit (e.g. inquiries). You can find educational information about credit scores on the website as well.

To access your FICO score with Discover’s FICO Credit Scorecard, either visit their website or use the bank’s mobile app.

Bank of America

Bank of America is another widely used bank that offers free FICO scores to consumers. However, to enroll in this program, you must be a Bank of America credit card customer.

Much like Discover’s offering that we described above, Bank of America’s FICO Score Program provides customers not only with their FICO scores but also information on the major factors that influence your credit score, your month-to-month credit score history, and education about how to achieve and maintain good credit.

On top of this, Bank of America also compares your credit score to the national average.

Bank of America customers can view their FICO score for free on the company’s website or mobile app.

Citibank

Consumers who have Citibank branded credit cards can obtain their FICO score for free from Citi.

Citi states on their website, “We think it’s important to provide our cardmembers with free access to information that will help them understand and stay on top of their credit status. That’s why we’re providing you with your FICO® Score and information to help you understand it.”

Your FICO score from Citibank is determined using information from your Equifax credit report and the FICO Bankcard Score 8 credit scoring model. Unlike the standard version of FICO 8 that you may be used to seeing, which ranges from 300 to 850, the bank card model used by Citi ranges from 250 to 900. It is updated once a month.

You can find more information on Citi’s free FICO score program on their website.

American Express

Recently, American Express started providing access to free FICO scores to consumers who have American Express credit cards.

The bank uses the standard version of FICO 8, so the credit score range spans from 300 to 850. Experian provides the credit report data used to calculate your score.

As with the other free FICO score programs, you also get to see how your FICO score changes over time and you receive a summary of the factors affecting your credit score.

American Express credit cardholders can see their FICO scores in their online account or on their monthly statement.

Those who do not have credit cards with American Express can get their TransUnion VantageScore for free through the company’s MyCredit Guide program, but this does not include FICO scores.

Barclays

FICO scores from TransUnion are available to all Barclays credit card customers through the bank’s online banking system.

Once you have had your Barclays card for three months, you can see a chart of your FICO score history over the time you have had an account open with Barclays, according to SmartAsset.

Plus, Barclays will send you alerts via email if your credit score changes, including an explanation of why your score has changed.

Wells Fargo

Wells Fargo account holders who use their online banking platform can view their FICO credit score within their online account.

Additional features include your credit score history, information on your credit score factors, and personalized credit tips from Wells Fargo.

According to the bank, they offer your FICO score for free in order to “support your awareness and understanding of FICO® Credit Scores and how they may influence the credit that’s available to you.”

The FICO score you get through Wells Fargo is calculated using Experian credit report data and is updated once a month.

Experian

Experian is the only major credit bureau that offers consumers their FICO 8 scores for free along with their Experian credit reports.

In addition, Experian offers an alternative credit data program called Experian Boost, which can add positive payment history from certain bills to your credit report, such as utilities and Netflix.

Sign up on Experian’s website to start using these free services.

Your Local Bank or Credit Union

Not all banks and credit unions offer customers the ability to check their FICO scores for free, but it is worth asking if you do not have access to the previous options. If your local bank or credit union does not offer free FICO scores, they may be able to help direct you toward somewhere that does.

Will Checking Your FICO Score Hurt Your Credit Score?

Although this is a common concern, checking your own credit score should never hurt your credit.

This credit myth likely arises from the fact that hard inquiries on your credit report can have a small negative effect on your score.

However, hard credit inquiries only happen when you are actively seeking credit and a lender has to pull your credit report to decide whether or not to loan you money.

All other credit checks, including those you conduct yourself for educational purposes, are considered to be soft inquiries, which do not affect your score at all.

Final Thoughts on How to Get Your FICO Score for Free

If you want to be able to see your FICO score for free, there are many options available to you, especially if you have credit card accounts with major banks such as those listed above.

FICO also has a program called FICO Score Open Access that aims to enhance consumer access to FICO scores and educate consumers about the topic. FICO has a list of additional lenders and credit and financial counseling organizations that participate in this program, which you can browse in case you do not have any accounts with the banks mentioned here.

Keep in mind that lenders use many different versions of FICO scores, including older generations and versions that are specific to certain industries. That means that when you check your FICO score for free, it is not guaranteed to be the same exact FICO score that a lender will use when you apply for credit.

When you check your FICO score using one or more of the methods in this article, take note of which credit bureau is supplying the information as well as which FICO score version is being used to calculate the result so that there is no confusion if you see a different FICO score somewhere else.

Finally, remember that you can also get your VantageScore for free in many places as well. While it’s not the same as your FICO score, it can still provide educational value as it uses the same general principles to calculate your score.

Let us know if this article helped you find a way to get your FICO score for free by commenting below!

Using a credit card is easy — you use the card to buy things and then pay the credit card bill.

A credit card can sometimes be difficult, however, when dealing with your credit file. From a missed payment to a loan that isn’t yours that’s incorrectly listed on your credit report, there are all kinds of ways your credit score can drop. And not all of them are from something you did wrong.

Consumers have protections under the law regarding their credit reports — which is where credit scores and credit problems are listed for lenders to check before offering you credit. Errors on a credit report can drop your credit score, making it harder to get a loan, credit card, rent an apartment, or qualify for insurance coverage, among other things.

The main law that protects consumers from credit errors is the Fair Credit Reporting Act, or FCRA. Here are some of the rights you have under this law and how to use it to protect your credit:

View credit reports

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it.

Start by going to AnnualCreditReport.com to request your credit file online. Only use that website and don’t use a copycat site that charges fees for what should be a free service. You’ll need to verify your identity to get online access. You can also request your credit file through an automated phone system or the mail.

The FCRA applies to all consumer reporting agencies. You can also look at reports from other consumer reporting agencies that collect noncredit information about you. These include rent payments, insurance claims, employers and utility companies. The Consumer Financial Protection Bureau lists the reporting companies and how to request a free report from each.

Check your credit score

The law allows you to request a credit score, though it’s legal for credit agencies and other businesses to charge you a fee for this service. Some credit cards provide scores for free, so check with your credit card issuer first.

A credit score isn’t the same as a credit report. Information in a credit report determines a credit score, and each credit bureau can use a different scoring model that requires it to provide different information. You have different credit scores, depending on which factors are weighed more heavily.

Monitoring your credit is vital. Make sure that you review your credit report for any inaccuracies.

Know who can view your credit report

The FCRA doesn’t allow a credit reporting agency to share your credit file with someone who doesn’t have a valid need. Some inquiries, such as from a potential employer or landlord, require your written consent. And, they can only check your credit report, not your credit score.

The credit reporting agencies can share your credit report for legitimate reasons, such as when you’re applying for credit, insurance, housing or with a current creditor.

Disputing errors

Getting a credit report in your hands can lead to all sorts of eye-opening concerns. Anything that’s listed as negative should be checked for accuracy. Here are some things to look out for:

Eviction that wasn’t legal.

Creditor listed that you didn’t have an account with.

Loan default.

Wrong name.

Wrong address.

Wrong Social Security Number.

Incorrect loan balance.

Closed account reported as open.

A loan you didn’t initiate.

Some errors may be simple to resolve and others you may need to do more research on before disputing them to ensure they’re incorrect.

For example, you may not recognize the name of a creditor and assume you don’t have an account with them. But it may just be a store credit card you recently applied for that is listed by the issuing bank’s name. Or maybe a home or auto loan was sold to a new loan servicer.

Other errors could be reason to suspect identity theft, or there could just be wrong information that’s bringing down your credit score.

If you suspect identity theft, such as someone taking out a credit card in your name, then file a police report and report it to your credit card company and the credit reporting agencies.

To dispute erroneous information, use certified mail to send the credit bureau a letter and copies of documents explaining the error. If a loan still shows an outstanding balance and you have written proof that it was paid off, for example, send a copy to the credit agency.

Credit agencies have 30 days to investigate and respond to your dispute, unless they deem it frivolous.

If it corrects an error, it must send you a free copy of your credit report through AnnualCreditReport.com so you can see that the corrections have been made.

A time limit to negative information

The FCRA doesn’t allow credit bureaus to report negative information that’s more than seven years old, though it allows some forms of bankruptcy to remain on a credit report for 10 years.

There’s also a time limit for positive credit information such as on-time payments and low balances — up to 10 years after the last date of activity on the account.

Rejections based on credit report

If your application for credit, job, insurance or housing has been denied because of information in your credit report, the law gives you the right to know this information.

The landlord, employer or other entity that denied your application must notify you and give you the name, address and phone number of the credit reporting agency that provided the information.

The FCRA allows you to get a free copy of your credit report from that reporting agency within 60 days of the action against you. That’s in addition to the three free credit reports allowed annually.

To best deal with a potential rejection ahead of time, it’s smart to check your credit report before applying for credit, rental unit or related use of your credit report and check it for errors. Give yourself enough time to fix them.

Go to court

If these actions or a complaint with the CFPB doesn’t resolve your dispute, you may be able to sue for damages in state or federal court. You can sue a credit reporting agency or related parties for violating any of the above rights.

However, it’s worth knowing that your right to legal action doesn’t start until after the creditor or credit reporting agency has been notified of an error and has a chance to fix it. In other words, you’ll only be awarded damages if the adverse action happened after you reported the error.

So if you didn’t get approved for a mortgage because of a mistake on your credit report, it’s unlikely you’ll be compensated for losing out on the house if you lost out on it before reporting the mistake.

Did you know that a large proportion of consumers have errors on their credit reports? Unfortunately, it’s true. In 2017, the most common complaint received by the Consumer Financial Protection Bureau (CFPB) had to do with incorrect information being reported on consumers’ credit reports.

A study conducted by the FTC in 2012 found that about 25% of consumers had at least one error on one of their credit reports. Some of those consumers were paying higher interest rates on loans as a result of those errors bringing down their credit scores.

From this information, you can see that it’s all too likely that you may have an error in your credit report. Let’s go over some of the most common types of credit report errors and how to fix errors on your credit report.

How to Get Your Credit Report

The first thing you will need to do in order to identify errors on your credit report is, of course, obtain a copy of your credit report.

You can get your credit report for free from annualcreditreport.com, which is the only website authorized by the government to provide your annual free credit report.

Under the Fair Credit Reporting Act (FCRA), you are legally entitled to receive one free credit report from each of the three major credit bureaus once every 12 months. You can choose to order all three credit reports at the same time or order each individual report at different times throughout the year.

Watch out for other websites claiming to offer free credit reports or free trials, especially if they ask you for payment information.

However, there are some reputable websites where you can view a simplified version of your credit report for free, such as CreditKarma, CreditSesame, WalletHub, and Bankrate. They are able to offer this service by advertising credit products to users.

Inspect your credit report regularly to catch errors early.

You can also request a free credit report if you are denied credit because of information found in your credit report. The credit report must be from the credit bureau that provided the original report to the lender.

In addition, you can qualify for an additional free report if you are unemployed and planning to apply for jobs, if you receive government assistance, or if you are a victim of identity theft.

Credit experts recommend checking your credit reports at least once a year, so make sure to take advantage of any opportunities to get a free copy of your credit report.

You can also pay to get your credit reports directly from the credit bureaus.

Types of Credit Report Errors

Identity Errors

Your personal information is not accurate. For example, your name is misspelled or your address is incorrect. This is an indication that the credit bureau may be confusing you with another person. This can sometimes happen with family members who have similar names or live at the same address.

Your file has been mixed with someone else’s. If you see accounts on your credit report that belong to someone else who has a similar name or the same address, this could mean that your credit report has been merged with another person’s report due to having similar personal information.

There are accounts that you didn’t open. Accounts that you know you didn’t open but are listed in your name indicate that someone has stolen your identity and used it to fraudulently open accounts.

If there are accounts in your name that you didn’t open, your identity may have been stolen.

Account Information Errors

Accounts are reported more than once (duplicate accounts). Sometimes, the same account may be shown twice on your credit report. This can definitely hurt your credit if it’s a derogatory account that’s been duplicated.

An account reports that you are the primary owner of the account when you are actually an authorized user (or vice versa). It’s possible that the credit bureaus have mixed up who is the primary owner of the account.

Closed accounts are reporting as open (or vice versa). Sometimes, accounts that you have closed in the past will still be reporting as open. This can be problematic especially if it’s a negative account, such as a collection. On the other hand, if an open account is reporting as closed, that’s also a problem because it can hurt your utilization ratio.

There are late payments on your report, but you were on time. Late payments are highly damaging to your credit score, so if you’ve never been late paying your bills but your credit report indicates otherwise, that’s an error you’ll want to correct as soon as possible.

An account has an inaccurate open date or date of first delinquency (DOFD). If an account has an incorrect open date, this could change the age of the account, which could, in turn, impact your credit score. An incorrect DOFD on a derogatory account, such as a collection account, will affect when the negative mark falls off your credit report.

Accounts show incorrect balance or credit limit information. Some credit cards do not report a credit limit at all, which could hurt your credit utilization ratio. Alternatively, your credit report may not be showing the correct balance or credit limit, which could also potentially hurt your utilization.

Clerical Errors

Inaccurate data was added back into your credit report after being corrected. If you’ve corrected an error on your credit report but then see the same error pop back up again, it could be a clerical error on the part of the credit bureaus or the data furnisher.

Duplicate collection accounts with different debt collectors are all being reported as open accounts. As we explained in our article on collections, this situation is called “double jeopardy” on your credit report. If an account has been sold to a debt collector, there may legitimately be multiple accounts for the same collection on your credit report, but the original account should be updated to show that it has been transferred and should no longer show a balance owed. The collection agency that currently owns the debt should be the only entity reporting the collection as open with a balance owed.

There is negative information on your credit report that is more than seven years old. Negative information must be removed from your credit report seven years after the date of first delinquency, so if any derogatory information on your credit report is older than seven years, you can have it deleted.

How to Fix Errors on Your Credit Report

To get the best results, write a letter for each dispute and send your letters by certified mail.

If there are any errors on your credit report, you can contact the credit bureau that is reporting the inaccurate information to resolve the issue. Your credit report should contain information on how to file a dispute.

1. Gather All Necessary Information and Supporting Evidence

When you submit your dispute, it’s important to provide all the information the credit bureau will need to process your claim.

This may include the following:

An annotated copy of your credit report (circle or highlight the incorrect item) Documentation to verify your identity (copies, not original documents)

A letter containing additional information about the item, an explanation of why it is incorrect, and a request to update or remove the incorrect item

Copies of supporting documents that provide proof of the item’s inaccuracy

2. Submit Your Credit Dispute Letter Via Certified Mail

Although it is possible to dispute credit report errors online, many credit experts recommend instead writing a letter and sending it in the mail along with documentation to verify your identity and supporting evidence.

If you try to dispute an error online or over the phone, you may not have the chance to provide enough supporting evidence, and the credit bureau may dismiss your dispute as frivolous.

It’s also recommended that you send your letters by certified mail so that you have proof that the letters have been received. In addition, it’s a good idea to keep copies of your correspondence in case you need to get outside help.

3. Send a Separate Dispute Letter for Each Error

If there is more than one error on your credit report to deal with, it is best to send a separate letter for each dispute, since the credit bureaus may reject long lists of disputes as frivolous.

4. Consider Working With a Reputable Credit Repair Company

Annotate each error in your credit report and provide documentation supporting your dispute.

If you have a lot of errors to dispute or if you have been the victim of identity fraud, you may consider hiring a credit repair service to assist with the process. [Disclosure: This article contains affiliate links.]

5. Contact the Furnisher of the Incorrect Data

You should also contact the lender that furnishes the data to the credit bureaus to ensure the inaccuracy gets corrected at the source. The FTC also provides a sample dispute letter to send to data furnishers.

If you neglect this step, the error could show up on your credit report again the next time the lender reports to the credit bureaus.

6. If Your Identity Was Compromised, Consider Placing a Credit Freeze or Fraud Alert on Your Profile

If the error on your credit report was the result of identity theft, it might also be a good idea to contact the credit bureaus to place a fraud alert or credit freeze on your account.

A fraud alert requires lenders to take extra steps to verify your identity if someone is trying to open an account in your name, whereas a credit freeze blocks anyone from viewing your credit file except for businesses that you have existing relationships with.

Keep in mind that if you are planning to buy tradelines, you must have all fraud alerts and credit freezes removed first, or the tradelines will not post.

What Happens Next?

Once the credit bureau has received your dispute, they have 30 days to investigate your claim. If their investigation cannot verify the information on your credit report, they must update it with accurate information or delete the item.

In addition, the credit reporting agency is required to provide you with written documentation of the results of the investigation.

You are also entitled to get a free copy of your credit report from the company if your credit report has been changed as a result of the dispute. This free copy is not counted as one of your annual free credit reports from annualcreditreport.com.

Upon your request, the credit bureau must notify any entity who pulled your report in the past six months about the corrections made to your report. If anyone has pulled your report for employment purposes in the past two years, you can ask to have an updated copy of your report forwarded to them as well.

What To Do If You Disagree With the Dispute Results

Option 1: Add a Consumer Statement to Your Credit File

If your dispute is rejected and you don’t agree with the credit bureau’s decision, you have the option of adding a consumer statement to your credit report to explain the situation. However, this is not necessarily the best solution.

Firstly, the statement doesn’t get factored into your credit score, so it won’t help your chances when a lender uses an automated system to approve or reject applicants. If it’s a case where an underwriter is looking at your credit report, adding a consumer statement may just draw their attention to a negative item unnecessarily, especially if the item is older.

Option 2: File Another Dispute With Additional Information

Another option is to submit a second dispute with additional supporting documentation to try to get the credit bureau to investigate the dispute a second time.

Option 3: Submit a Complaint to the CFPB

If the credit bureau still fails to correct the information in your credit report, you can submit a complaint to the CFPB.

The CFPB may not be able to force the credit bureaus, as private companies, to do anything, but getting a government agency involved might encourage the credit bureau to rethink their position.

Option 4: Take Legal Action

Continuing to report inaccurate information after you have disputed it is a violation of the FCRA. If you feel that a credit bureau is violating your rights under the FCRA, you have the option of talking to a lawyer about potentially taking legal action.

Conclusions on Credit Report Errors

Unfortunately, errors on credit reports are very common, so we all need to be vigilant about monitoring our credit for fraud and inaccuracies.

Make sure to check your credit reports regularly by claiming your annual free credit reports as well as using a reputable free or paid service throughout the year. As soon as you spot any errors, try to get to the bottom of them and get them corrected both with the credit bureaus and with the data furnishers as soon as possible.

By making sure that your credit report only contains accurate and timely information, you are helping to protect your financial health and ensuring that credit report errors don’t stand in the way of future opportunities.

Nearly half of Americans believe a credit score and a credit report are the same thing, according to a study by the American Bankers Association. That’s a big problem because it means many of us are seriously misinformed about how the credit system works.

Since credit is such an integral part of our financial ecosystem, it affects nearly all of us at some point in our lives. Your credit health can determine not only your access to credit and the cost of using credit but also employment opportunities, housing options, and more. Not understanding how credit works, therefore, can have serious consequences.

We want to help address this problem by making it easy to understand what your credit report is and why it’s important, the difference between your credit report and credit score, how to get a free credit report, and how to dispute errors on your credit report.

What Is a Credit Report and Why Is It Important?

A credit report is a detailed report on your credit history prepared by a credit reporting agency, also known as a credit bureau. The three main credit bureaus are Experian, Equifax, and TransUnion, and we’ll discuss each below. What is in your credit report can be different for each bureau, since they are private companies that do not share information.

What Is in a Credit Report?

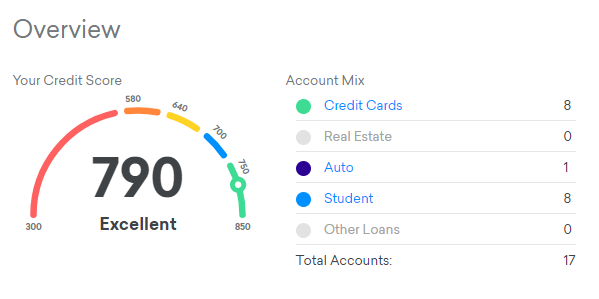

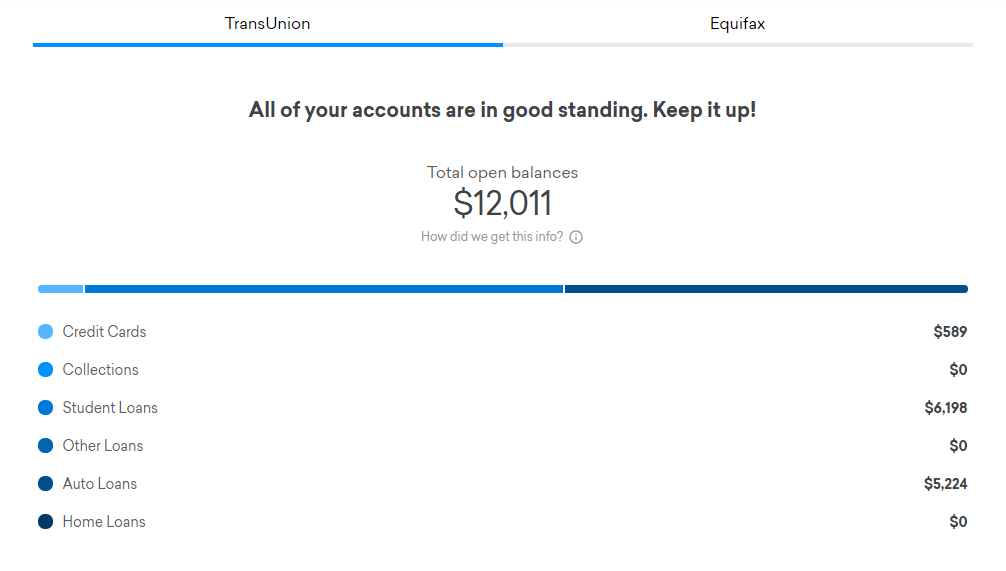

Credit reports contain identifying information such as your name, social security number, and current and previous addresses. They also contain a detailed summary of your credit history, which includes items such as the following:

Credit reports include a list of your credit accounts and financial records.

A list of current and past tradelines (credit accounts), along with the date opened, credit limit, balance, and payment history of each account Inquiries into your credit history

Public records of bankruptcies, foreclosures, tax liens, etc. Accounts in collections

How Far Back Do Credit Reports Go?

The information in your credit report usually goes back about 7-10 years.

Current accounts should show up on your credit report as long as they are open.

Negative information, such as collections, will fall off your credit report seven years after the delinquency occurred. Closed accounts that were closed in good standing fall of your credit report in 10-11 years.

What Is the Difference Between a Credit Report and a Credit Score?

A list of all your credit accounts and related personal information

A three-digit number between 300 and 850 meant to represent your creditworthiness

Information in your credit report is used to calculate your credit score

Reflects the information in your credit report

You are legally entitled to get a free credit report from each bureau once a year

You are not legally entitled to check your credit score for free (although some credit card companies may offer this to customers)

Does not include your credit score

Does not include information on your credit history

Does Checking My Credit Report Hurt My Score?

While this is a common misconception, you can rest assured that checking your credit report won’t lower your credit score. Checking your own credit is what’s known as a “soft inquiry” or “soft pull,” which doesn’t hurt your credit. “Hard” inquiries can ding your score, but these are used by creditors when making lending decisions, not for checking your own credit report.

How to Get a Free Credit Report

By law, everyone is entitled to receive one free credit report from each of the three major credit bureaus once every 12 months. You can order all three at the same time or order each individual report one at a time.

Some people like to spread them out and get a free credit report from a different bureau every four months so that they can regularly check their credit reports for errors and inconsistencies. Each credit bureau is a private, for-profit company, and they don’t share information, so you could have errors on one of your credit reports but not the others.

Free credit monitoring websites like CreditKarma provide free credit reports and scores.

The best way to check your credit report for free is to order your free credit report from annualcreditreport.com. In fact, this is the only website authorized to provide the annual free credit report you are legally entitled to, according to the FTC—so beware of other sites claiming to offer free credit reports or free trials, especially if they ask for your credit card information.

However, there are now several free credit report websites that earn money through advertising and are thereby able to offer free credit monitoring services. Sites that offer completely free credit reports include:

You can also check your credit report for free if you have been denied credit because of the information in your credit report. You are entitled to get a free credit report from the bureau who provided the report that the lender used to make their decision.

You are entitled to a free credit report if you are unemployed and applying for jobs.

For example, if the lender who denied you credit looked at your Experian credit report, you can request your Experian free credit report. The adverse action letter informing you of the reason for your denial should have instructions on how to request your free credit report.

There are a few more cases in which you can qualify for an additional free credit report, including:

If you are unemployed and planning to look for work.

If you receive government assistance.

If you are a victim of identity theft.

Although experts recommend checking your credit reports at least once a year, the Consumer Financial Protection Bureau (CFPB) estimates that less than one in five consumers get copies of their credit reports each year. Don’t miss out on this opportunity to get your credit report for free so you can make sure your credit report is accurate and identify any problems before they get worse.

Can I Get a Free Credit Report Directly From the Credit Bureaus?

You can also get your credit report directly from each of the credit bureaus, but you may have to pay a fee if you go this route. If you want to get a credit report for free, your best bet is to order from annualcreditreport.com.

However, some people may want to check their credit reports more than once a year, so we’ll discuss additional options for obtaining your credit reports below.

Experian Credit Report

You can get a free Experian credit report that refreshes every 30 days through Experian’s website. They also offer paid options that come with additional information. The Experian free credit report does not include a free credit score.

Equifax Credit Report

You can get your TransUnion and Equifax free credit reports on third-party websites.

While you cannot get an Equifax free credit report from the bureau directly, you can pay a fee to access your Equifax credit report and score. To get your Equifax credit report, visit their website.

You can also view your free Equifax credit report and score through CreditKarma, which updates once a week.

TransUnion Credit Report

Accessing your TransUnion credit report requires signing up for a paid monthly subscription service with TransUnion. However, you can get a free TransUnion credit report from CreditKarma or NerdWallet.

How to Dispute Errors on Your Credit Report

Unfortunately, studies have shown that as many as one in five consumers may have errors on their credit reports, and about one in 20 have errors that are significant enough to potentially lower their credit scores. This means it is crucial to monitor your credit reports regularly and be aware of how to fix errors on your credit report.

The credit bureaus offer online forms to submit credit report disputes, but experts warn against using this option, as it does not allow you to write a detailed explanation of why you are disputing the information or provide sufficient supporting evidence. This leaves room for the credit reporting agency to deny your claim because you did not provide enough information.

The best way to dispute a credit report is to write a detailed credit report dispute letter and mail it to the bureau along with plenty of documentation verifying your identity and supporting your claim.

Once a dispute has been filed, the bureaus typically have 30 days to investigate the claim. If they verify that the item is accurate, it will remain on your report; if not, they must either update the item with the correct information or delete it entirely.

Errors on your credit report can, unfortunately, lead to bad credit. For this reason, checking your credit report regularly and disputing any errors is an essential step in maintaining your financial health.

It’s important to check your credit report for errors regularly.

If you have a lot of errors on your credit report or if you have been the victim of identity theft, it may also be worth considering hiring a reputable credit repair service to assist you in the dispute process.

Which Errors Can You Dispute?

The law requires that the information in your credit reports must be accurate, complete, timely, and verifiable. Anything that does not meet these requirements can be disputed.

Technically, you can dispute anything in your credit file, but that doesn’t mean you should try to dispute things that you know are accurate. The credit bureaus are allowed to ignore “frivolous” claims, and if they verify something to be true, it will stay on your credit report.

For more tips on how to dispute a credit report, check out this article from creditcards.com.

Quick Credit Report Facts

A credit report is a detailed report on your credit history prepared by one of the credit bureaus: Experian, Equifax, and TransUnion.

The information in your credit report is used to calculate your credit score.

Checking your credit report does not hurt your score.

You are entitled to a free credit report from each of the three bureaus once a year, which you can order from annualcreditreport.com.

You can dispute errors on your credit report by mailing a credit report dispute letter and supporting documentation to the credit bureau.

Under federal law, you’re entitled to a free credit report if a company takes adverse action against you, such as denying your application for credit, insurance or employment, and you request your report within 60 days of receiving notice of the action. The notice will give you the name, address, and phone number of the consumer reporting company that supplied the information about you. You’re also entitled to one free report a year if you’re unemployed and plan to look for a job within 60 days; if you’re on welfare; or if your report is inaccurate because of fraud. Otherwise, a consumer reporting company may charge you up to $9.50 for additional copies of your report.

Under state law, consumers in Colorado, Georgia, Maine, Maryland, Massachusetts, New Jersey, and Vermont already have free access to their credit reports.

If you ask, only the last four digits of your Social Security number will appear on your credit reports.

Establishing a Credit History

If you’re denied a loan or credit card because you have no credit history, consider establishing one. The best way is to apply for a small line of credit from your bank or a credit card from a local department store. Make sure you list your best financial references. Make payments regularly and make certain the creditor reports your credit history to a credit bureau.

If Your Spouse Dies

Under the ECOA, a creditor cannot automatically close or change the terms of a joint account solely because of the death of your spouse. A creditor may ask you to update your application or reapply. This can happen if the account was originally based on all or part of your spouse’s income and if the creditor has reason to believe your income alone cannot support the credit line.

After you submit a re-application, the creditor will determine whether to continue to extend you credit or change your credit limits. Your creditor must respond in writing within 30 days of receiving your application. During that time, you can continue to use your account with no new restrictions. If you’re application is rejected, you must be given specific reasons, or told of your right to get this information.

These protections also apply when you retire, reach age 62 or older, or change your name or marital status.

Kinds of Accounts

It’s important to know what kind of credit accounts you have, especially if your spouse dies. There are two types of accounts — individual and joint. You can permit authorized persons to use either type.

An individual account is opened in one person’s name and is based only on that person’s income and assets.

If you’re concerned about your credit status if your spouse should die, you may want to try to open one or more individual accounts in your name. That way, your credit status won’t be affected.

When you’re applying for individual credit, ask the creditor to consider the credit history of accounts reported in your spouse’s or former spouse’s name, as well as those reported in your name. The creditor must consider this information if you can prove it reflects positively and accurately on your ability to manage credit. For example, you may be able to show through canceled checks that you made payments on an account, even though it’s listed in your spouse’s name only.

A joint account is opened in two people’s names, often a husband and wife, and is based on the income and assets of both or either person. Both people are responsible for the debt.

Account “Users”

If you open an individual account, you may authorize another person to use it. If you name your spouse as the authorized user, a creditor who reports the credit history to a credit bureau must report it in your spouse’s name as well as in yours (if the account was opened after June 1, 1977). A creditor also may report the credit history in the name of any other authorized user.

If You’re Denied Credit

The ECOA does not guarantee you’ll get credit. But if you’re denied credit, you have the right to know why. There may be an error or the computer system may not have evaluated all relevant information. In that case, you can ask the creditor to reconsider your application.

If you believe you’ve been discriminated against, you may want to write to the federal agency that regulates that particular creditor. Your complaint letter should state the facts. Send it, along with copies (NOT originals) of supporting documents. You also may want to contact an attorney. You have the right to sue a creditor who violates the ECOA.

The vast majority of lenders use your FICO

The vast majority of lenders use your FICO

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it.

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it. Did you know that a large proportion of consumers have errors on their credit reports? Unfortunately, it’s true. In 2017, the

Did you know that a large proportion of consumers have errors on their credit reports? Unfortunately, it’s true. In 2017, the