There are plenty of articles out there about the fastest ways to raise a credit score, but the focus of this article and infographic is a bit different. Rather than giving you shortcuts on how to boost your credit score, we’re talking about the fastest ways to build credit for long-term success.

While raising a credit score can be accomplished in various ways, not all of them involve actually building your credit profile by adding more accounts. Credit repair companies may offer tactics on how to raise credit scores by removing negative, inaccurate information from your credit file, but this strategy doesn’t do anything to build your credit history by establishing new accounts. They may remove harmful inaccurate information, but they often lack in assisting with credit re-establishment.

Opening a mix of several different accounts and keeping them in good standing is crucial for building a good credit record, but this process takes time. It is well-known that a credit account needs at least two years of history to be considered “seasoned,” which is when it has enough age to show that you can properly handle the account and therefore begins to improve your credit score.

Before this point, when an account is still young, it represents a risk to the lender because they don’t know if you will use the credit responsibly. They don’t know if you are going to max out your cards, miss payments, etc. That’s why new accounts often hurt your credit temporarily.

So what can you do if you don’t have 2+ years to open new accounts and wait for them to age? What if you can’t get approved for credit on your own to begin with? How do you build good credit fast?

Piggybacking: The Fastest Way to Build Credit

The answer to how to build credit fast is piggybacking. This term refers to the practice of building credit by becoming associated with someone else’s credit accounts.

This might sound surprising, but studies have shown it is a very common practice. A study of over 1 million consumers by the Consumer Financial Protection Bureau showed that nearly a quarter of consumers transitioned out of credit invisibility by piggybacking on the creditworthiness of others. According to a survey by creditcards.com, 86 million Americans have shared a credit card account with someone else!

Additionally, a study by the Federal Reserve Board found that about 30% of consumers with a scorable credit record have at least one authorized user account on their credit record.

There are three main ways that piggybacking occurs: getting credit with a co-signer, being a joint credit account holder, or becoming an authorized user.

Build Credit Fast With a Cosigner or Guarantor

One very common strategy for someone who needs help building credit fast is to apply for credit with a cosigner or guarantor, which is a person who can be responsible for the debt in the event that the primary borrower cannot repay it. The cosigner or guarantor does not typically receive access to the funds or make payments on the debt unless the primary borrower is no longer able to.

A cosigner or guarantor can help a borrower get credit by pledging to be responsible for the debt if the primary borrower cannot repay it.

Pros:

Since the cosigner or guarantor’s credit record and income are considered when applying for credit, the primary borrower may be able to piggyback off the cosigner’s good credit to qualify for credit or get better terms.

Cons:

Getting credit with a cosigner or guarantor means opening a new account, which dings credit temporarily. It is still going to take a few years for the account to age enough to help build your credit score.

It may be difficult to find someone willing to cosign on a loan or credit card since it is a risky proposition without much benefit for the cosigner.

Some lenders, particularly credit card issuers, may not even allow cosigners.

It may be difficult or impossible to remove the cosigner in the future, so the cosigner must be willing to potentially be permanently associated with the account.

Building Credit as a Joint Account Holder

As joint account holders, two parties apply for one account that they can both use. Both parties have full access to the account and both are held fully responsible for the account. Joint accounts are most commonly used by spouses with shared finances.

Joint accounts can help build credit, but they are most commonly used by spouses with shared finances.

Pros:

Both applicants are considered by the lender when issuing credit. By pairing with someone with good credit, a person with less-than-perfect credit may be able to open an account that they wouldn’t have qualified for on their own, or get more favorable terms.

If the joint account is kept in good standing over time, it can continue to help build the credit of the user who needs to improve their credit profile.

A joint account can make it easier for two people to manage their finances together.

Both account holders have access to the privileges associated with the account, such as rewards.

A joint account is also considered a primary account since each borrower has full access to the account and full liability for the debt.

Cons:

Opening a joint account means adding a new account to your credit report, which decreases the average age of accounts and can temporarily hurt your credit. The account will still need at least two years to age enough to help improve your credit score.

Both users are fully responsible for the debt. If one person maxes out the account, the other can legally be held responsible.

It’s always possible that an event such as a breakup could change the relationship between account holders, which could make it difficult to manage the account.

Disagreements over the account could damage the relationship between account holders.

It might be difficult to find someone to open a joint account with you if you do not have a spouse or if your spouse does not want to combine finances.

Not all lenders provide joint credit accounts, so options for opening a joint account are limited.

Many joint accounts do not provide the option of removing a joint account holder, so both users are often attached to the account permanently unless they decide to close it altogether.

Authorized user credit piggybacking is one of the fastest ways to build credit. Photo via seniorliving.org.

How to Build Credit Fast as an Authorized User

You’re probably already familiar with the concept of piggybacking credit as an authorized user. The classic example is parents who add their children as authorized users of their credit cards for the purpose of helping them build a credit history. Often, the young adult does not even get a credit card, so they can’t make charges to the account—the goal is solely to have the account show up on their credit report.

Pros:

The account can show up on the authorized user’s credit report as soon as the next reporting date for that credit card, which means it can build your credit fast.

Only the primary account holder is responsible for the debt incurred, not the authorized user.

Only the primary cardholder’s credit file is considered when the credit card company issues the card. Therefore, many times, an authorized user may be added to the account even if their credit is not as pristine as the primary cardholder.

The authorized user’s credit score does not affect the credit of the primary cardholder (as long as the authorized user does not increase the utilization of the account by making charges). Being an authorized user can be a great way to build credit fast, since the full history of the account is often shown in the credit reports of both the primary cardholder and the authorized user, regardless of when the authorized user was added (with some exceptions depending on the bank).

The authorized user can remove themselves from the account if they no longer want the account to appear on their credit report, such as if the account becomes delinquent.

Cons:

Authorized users don’t have the ability to make changes to the account like the primary cardholder. The primary cardholder does not even have to give the authorized user a credit card.

If the account shows any negative behaviors such as a late payment or high utilization, this will be reflected on the authorized user’s credit report, which may be counterproductive to the goal of building credit. If you buy an authorized user tradeline from a reputable company, however, the tradeline should have a perfect payment history and low utilization.

What Is the Best Way to Build Credit Fast?

While there are many ways to increase your credit score quickly, not all of them are conducive to building credit, which means strengthening your credit profile with additional accounts.

Credit repair techniques may promise to boost credit scores fast, but removing information from your credit report doesn’t help you build credit. To truly build or rebuild credit, you need to add positive credit history to your credit report.

Building credit for long-term success involves establishing a mix of different credit accounts, including credit cards and loans. These foundational accounts, with time, will aid in boosting your credit score to its highest potential.

However, if you need to build credit fast, you’ll have to take a different approach. Primary accounts need time to age and accumulate positive payment history before they can start to increase your credit score. And if you are starting with bad credit or no credit at all, it can be hard to get approved for credit accounts on your own.

The only shortcut we have seen to building credit fast is piggybacking credit. Through credit piggybacking, you can benefit from someone else’s good credit, whether that is by getting a cosigner to sign on with you, opening a joint account with someone, or becoming an authorized user on an existing account.

While the first two options are still restricted by the limiting factor of time, being added as an authorized user to a seasoned account can add years of positive credit history to your credit report almost instantly.

Therefore, if you need to build credit fast, consider adding one or more authorized user accounts to the mix, whether by asking a trusted family member or friend or purchasing them online from a reputable business.

Have you tried any of these ways to build credit fast? Share your experience with us in the comments!

Use our list of common mistakes below to make sure you get the most out of your authorized user tradelines. Don’t make the same mistakes we’ve seen before!

1. Having fraud alerts or credit freezes on your account

If you have fraud alerts or credit freezes on your account, new tradelines simply will not post on your credit report.

Fraud alerts essentially freeze your account, so new information cannot be added. If you have fraud alerts on your credit file, you must contact each credit bureau directly to have the fraud alerts removed before you will be able to add new tradelines to your file.

2. Not knowing how tradelines work

The most important factor in purchasing tradelines, in our opinion, is to understand how tradelines work. Without this understanding, it is easy to let commissioned salespeople lead you astray and sell you tradelines that are not the best for your particular situation.

If you are new to tradelines, then be sure to check out our Tradelines 101 infographic for a crash course on the basics as well as the large library of educational articles in our Knowledge Center.

3. Not understanding how credit scores work

Before buying tradelines, it is vital to have a general understanding of how your credit score works. There are tons of useful resources online that can walk you through what factors affect your credit score, such as our guide to building credit with tradelines. Knowledge is power, and understanding how credit scores work is worth the investment since your credit score can affect everything from your finances to your job.

The power of a tradeline does not necessarily depend on its price tag.

4. Judging the power of a tradeline strictly by price

When buying tradelines, putting price first is not wise. It is easy to assume that the more expensive a tradeline is, the more powerful it is, but this is not always the case.

For example, someone with a very established credit profile might look at a $1,000 tradeline and just assume that it is the one they want. However, if that $1,000 tradeline does not significantly improve their current average age of accounts or lower their already low utilization ratios, it may not have very much of an effect, or it could even hurt their credit!

Simply adding more of what you already have is not necessarily an improvement. Our Tradeline Calculator is the perfect tool to calculate where your numbers currently stand and how they may be affected by new tradeline data. Make sure to only select tradelines that will actually help you.

5. Not realizing that the power of a tradeline is always going to be relative to what is in your credit report

The power of tradelines is always going to be relative to what is already in your credit file.

For example, if your average age of accounts is already 10 years old, an 8-year-old tradeline may not necessarily help you very much, since you are not improving that variable.

On the other hand, if someone’s average age of accounts is only 1.2 years old, an 8-year-old tradeline may be more powerful for that person. Tradelines do not affect people in the exact same way because everyone’s credit file is unique.

For more information on choosing the best tradelines for your particular situation and goals, our buyer’s guide to choosing a tradeline is a valuable resource.

6. Relying strictly on buying tradelines

It is not smart to rely only on purchasing authorized user tradelines when building or rebuilding credit. In general, tradelines that you can purchase are usually authorized user positions on credit cards, which are revolving accounts.

While this can be very powerful, almost all credit scoring models will take into account your total mix of credit, and it is more favorable to have a good mix of different kinds of credit accounts.

Some additional examples of different types of credit accounts may include auto loans, mortgage loans, installment loans, etc. Having a good mix of credit types is ideal. For more detailed information on how to optimize your credit mix, check out our article, “Credit Mix: Do You Need to Care About Types of Credit?“

In addition, if your credit report has delinquencies such as collections or late payments, tradelines may not solve your problems. You may need to consider repairing your credit before adding tradelines or in tandem with your tradeline strategy. [Disclosure: This article contains affiliate links.]

The age of a tradeline, also referred to as “seasoning,” is often even more important than its credit limit.

7. Valuing limit more than age

Many people initially focus only on how large of a credit limit a tradeline has. They often think that the tradeline with the largest credit limit is automatically the best tradeline.

For example, they might ask, “Should I get the $30,000 tradeline, or do you think the $20,000 one is enough?” However, this question is flawed from the start.

As a real-life example, it is not uncommon for someone to open a new credit card (possibly with a high limit) and that person’s credit score drops initially. Perhaps the reason the person’s score goes down is a new account has no payment history and may pose a higher risk in the eyes of the credit bureaus until a pattern of on-time payments is established. In this example, a new high-limit primary account actually made their credit score go down initially.

It could be the case that a tradeline with a $1,000 limit is actually the best for them because maybe that one has a lot of age and meets their strict budget. Everyone should consider the age and the limit together when buying tradelines and use the Tradeline Calculator as the first step in assessing your situation.

8. Buying cheap tradelines as a test

Some people will use the strategy of buying a cheap tradeline to see what that does first, and if it works a little, then they will buy a better one next time. We feel this strategy is a mistake.

For one, it ends up costing more in the long run, because now they have to buy two tradelines (one cheap one and one better quality one) when the person would probably be better off just getting one high-quality tradeline to begin with.

Also, buying that cheap tradeline may be working against the goal of improving the average age of accounts because in general, cheap tradelines do not have very much age. So when you add a tradeline with little to no age and then later add a tradeline with age, the first tradeline with little to no age ends up lowering the average age of accounts, thus making it more difficult to improve that average.

Calculating your average age of accounts is crucial when choosing the best tradelines for your credit file.

9. Not doing the math on the average age of accounts

You would be surprised to find how difficult it is to significantly change an average, especially when there are multiple accounts in the equation.

As an experiment, imagine there are 5 accounts that are all 2 years old so the average age of accounts is 2 years old. Now guess how old a new 6th account would have to be in order to make the average age of accounts be 5 years old. (Take some time to guess this answer.)

The answer: 20 years old! Seriously, do this math. 2 + 2 + 2 + 2 + 2 + 20 = 30 divided by 6 accounts = 5 years average age of accounts. The easiest way to do the math for yourself is by using our Tradeline Calculator.

Even most “experts” at other companies do not do this math correctly and often guess wrong, and therefore give bad advice to customers as to which tradelines to buy.

10. Not getting old enough tradelines

If you look at the example above, you will see how easy it is to underestimate how old of a tradeline you may really need in order to significantly improve your average age of accounts. Age is essential. Do not underestimate how difficult it is to significantly change an average. Use the Tradeline Calculator to know for sure.

11. Not buying your tradeline far enough in advance before the reporting date

When you place an order for a tradeline, there is a processing time in order for the tradeline company to receive the funds. For example, with our eCheck payment method, it may take up to 5 business days to receive the funds.

Then, the credit partners have up to two days to add the authorized user. The credit card company may then have their own processing time for updating their records internally. Next, the banks update the credit bureaus, and finally, the credit bureaus publish their records.

For this reason, our “Purchase By Date” is typically around 11 days prior to the beginning of the reporting period. So as long as you purchase the tradeline by the Purchase By Date, we guarantee that your tradeline will post in the next reporting cycle.

12. Urgently needing a tradeline to post, but only buying one tradeline and betting your entire outcome on that one posting

Our posting success rate is the highest in the industry, but even given this fact, credit report data is not always going to be perfect.

In other words, although rare, non-postings do occur, and if you are betting your entire outcome on the results of one tradeline, you may want to consider hedging your bets and buying two tradelines to be safe.

In short, two is often better than one for many reasons. If it is extremely critical to get a tradeline to post, it is safer to just buy two.

13. Buying tradelines instead of paying down your debt

If you have credit cards with high utilization, it is usually best to pay those debts down before buying tradelines.

Having credit cards with high utilization ratios is a negative factor in your credit report. This negative factor will always play a part in your overall credit picture as long as it exists.

The only real way to solve this problem is to pay down your credit cards. You should do the math using our Tradeline Calculator to see where your money is better spent, but in general, paying down your debt is usually the best advice.

14. Thinking tradelines will fix high utilization

Tradelines should not be thought of as the solution to high utilization on your credit cards. While tradelines can affect your overall utilization ratio, having individual cards with high utilization will still be a factor in your overall credit picture.

In other words, you should not only take into account your overall utilization ratio, but also the individual utilization of each of your credit cards and the number of cards that have high utilization vs. low utilization. Again, the solution to the problem is paying your cards down.

15. Not factoring in closed accounts when calculating your average age of accounts

Many credit scoring models factor closed accounts into their equation. For example, some people with zero open accounts can still have a good credit score. Clearly, the closed account data is still part of the equation.

If you end up needing your tradeline to stay active on your credit report for longer than two reporting cycles, you don’t have to buy a whole new tradeline when the time is up. We offer unlimited extensions in 1-cycle increments at half the cost of the original purchase price.

Simply let us know at least 2 weeks before the scheduled removal date if you’d like an extension.

Make sure to use trusted platforms that provide secure online transactions.

17. Buying tradelines from an unethical company

Unfortunately, in this industry, it can be hard to know who to trust. It is essential to do your research and choose a company you trust so you don’t waste your money on low-quality tradelines, tradelines that don’t post, or tradelines that are overpriced.

You also need to be sure to only use reliable platforms that provide secure online transactions. Warning signs that could indicate that a company lacks integrity include fake reviews, unavailable or poor customer service, and websites that are not secure or do not look professional.

18. Asking what the average boost of credit score is

We do not guarantee any boost of your credit score and we also cannot say what the average credit score boost from tradelines is. Tradelines affect everyone differently. One tradeline may help one person while that same tradeline may hurt another, and have no effect on someone else.

All tradelines will be relative to what you already have in your credit file. There is no meaningful average effect of tradelines in general.

Although we do not guarantee any boost of your credit score, often when we hear a variation of the following question. The request goes something like this… “I currently have a 520 credit score but I want to be over 700. What tradeline do you recommend to accomplish this?”

Again, we are unable to answer these kinds of questions, but in talking about this topic in general, who says that it is even possible to go from a 520 to over 700 anyway? Not us. (Although we are not saying it is impossible either.) We just do not advise on these types of credit score requests.

But going back to talking in general, if someone has a 520 credit score they probably have some serious derogatory accounts in their credit. If they have such derogatory accounts in their credit file, their credit score will probably not be a 700 regardless of what other tradelines may exist in their credit file. So in this example, the question itself is flawed, since it may be impossible to begin with.

Even in less extreme examples, no one knows the exact credit score algorithms, so no one can say with certainty. Therefore, it is best to not ask that question, because whoever answers that question is making a wild guess and they could easily be wrong and give you bad advice.

Steer clear of CPNs, which could get you caught up in felony identity fraud.

20. Buying tradelines for a CPN

We do not sell tradelines to those trying to use CPNs.

The reason for this is that the Social Security Administration and the Federal Trade Commission have both stated that CPNs are not legitimate and that the use of CPNs to obtain credit is fraud and a federal crime. We highly recommend avoiding any person or business trying to sell you a CPN.

21. Thinking that buying a high-limit tradeline automatically means that you will also get approved for a high-limit credit card

Having a high-limit authorized user tradeline does not automatically guarantee that you will get approved for your own high-limit credit card. Most banks that offer credit cards will typically also consider your income, expenses, credit score, and possibly several other factors relating to your ability to repay debt in order to make a decision on whether or not they are willing to extend credit to you.

22. Mistaking tradelines for credit repair

Buying tradelines is not credit repair. Credit repair seeks to correct inaccurate items on your credit report. If you have inaccurate items on your credit report, you definitely want to get those items removed. [Disclosure: This article contains affiliate links.]

If you have bad credit, you may need to fix your credit in order to get the maximum benefit possible from tradelines.

Occasionally we get a call from someone who might tell us that they are currently 90-120 days late on 2-3 accounts and their credit score is in the dumps. Can we help someone with extremely bad credit? The answer is probably no.

Again, we are not able to advise on credit scores (only general information) but in our opinion, if they are currently that far behind on bills and have multiple major derogatories on their credit report, there is no way they can have good credit without correcting the situation.

After all, a credit score is meant to calculate the likelihood of someone defaulting on a credit account, and if they are proving that they are currently in default, then their credit score is going to reflect that. The best advice is to pay those accounts current if they are trying to improve their credit.

24. Buying tradelines from the wrong banks that don’t post well

The truth is that most banks across the country do not post authorized user data very reliably. In other words, with most banks, the odds of a non-posting are very high.

Our company has tried out almost all of the common banks, and due to our high volume of tradeline sales, we have amassed a large amount of data. We know which banks post well and which ones do not. In fact, just about every other tradeline company out there sells tradelines from many more banks than we do.

The reason for this is not because we do not have that inventory available. It is because our integrity level when it comes to the reliability of our postings is so important to us.

The truth is that any company who sells tradelines from more banks than we do automatically has a higher non-posting probability and a lower integrity level. Saying it bluntly, we have the highest posting success rate in this industry because we only work with the best of the best banks that post the most reliably. All other tradeline companies have a lower posting success rate because they work with banks that are less reliable.

If you have a bankruptcy or collection with a bank, tradelines from that bank may not post for you.

25. Having filed bankruptcy with the bank you are ordering a tradeline with

It is possible that some banks will not work with a person if they have filed bankruptcy with that bank. They may be in a sort of “blacklisted” status with that bank.

This can also apply to authorized user positions. Therefore, if you owed a debt to a particular bank when filing for bankruptcy, it is best to choose a tradeline from a different bank as a precaution.

26. Having outstanding collections against the bank you are ordering a tradeline with

Similar to the point made above regarding bankruptcies, having outstanding collections with a certain bank could also pose an issue. The collection status is probably less of a risk of non-posting than the bankruptcy status, but it is still worth mentioning as a potential problem.

27. Thinking that primary tradelines are the best option

Since there are many different credit scoring algorithms, everyone actually has many different credit scores.

Often the main goal of someone shopping for tradelines is to eventually open their own primary accounts. However, we regularly get calls from people asking if we sell primary accounts. The answer is no, we do not.

Being the primary borrower on an account means someone extended credit to that individual and they are financially responsible for that account. In other words, that person is actually issued credit.

We know of some options within the tradeline industry where companies really will issue credit and that accomplishes the “primary tradeline” desire that some consumers have, however, they are usually relatively low limits, and of course, they have no age since it is a brand new account.

So is a primary account with a low limit and no age better than an authorized user tradeline with a high limit and lots of age?

From what we have seen, if we had to choose between these two scenarios above, we believe the authorized user tradeline with age and a higher limit would be the more powerful choice.

28. Not realizing that you have many different credit scores

Each major credit bureau has its own algorithms and reporting methods, and even within each credit bureau, there are many different versions of credit scoring models. Often, the score that is used depends on what kind of company is ordering the report.

For example, not only might your credit score be different at each credit bureau, but the score might also be different depending on whether you are applying for a mortgage, a credit card, a car loan, or trying to rent an apartment.

The credit scoring algorithm used might be one of many different versions of the FICO score, or it could be a VantageScore.

It is possible that each person has over 30 different credit scores. If you google “how many credit scores do I have,” you can read more about this.

The authorized user must use the correct address that is on file with the credit bureaus to ensure the tradeline will post.

29. Not using the correct address that is on file with the credit bureaus

When adding an authorized user to a credit card, it is important that the authorized user provides the correct address that is on file with the credit bureaus. The authorized user’s address is a data point that helps identify the person, and if that does not match up, there can be issues with the tradeline posting.

Check your credit reports to confirm that the address in your file is correct and then make sure to provide this same address when purchasing your tradelines.

30. Having no credit score at all

There are instances where some people do not have any credit score at all. There may be several reasons why this is the case.

For one, maybe the person just never had any credit at all. If this is the case, then getting a tradeline to post should not be a problem.

Another possibility is that the person had derogatory items on their credit report and participated in some sort of aggressive credit sweep or credit repair deletion service that essentially deleted everything from their credit report.

In these types of scenarios, getting a tradeline to post can be a problem. Sometimes there may be blocks on that person’s credit file that prevent the new authorized user account from posting.

31. Not having enough tradelines or having only authorized user tradelines in your credit file

As we mentioned, having a good mix of various credit types is important to building good credit. Therefore, you do not want your entire credit profile to be made up of authorized user tradelines exclusively.

In general, the best credit profiles belong to people who have multiple tradelines from a variety of different types of credit, including credit cards, auto loans, mortgages, installment loans, etc.

A tradeline alert is a notification that a new or updated tradeline has posted to your credit file. To set one up, you will need to sign up for a credit monitoring service.

We ask our customers to make an account with Credit Karma, a free online service that automatically notifies you when new accounts have been added to your TransUnion or Equifax credit report. Credit Karma is also how you will verify whether or not your tradeline has posted.

33. Entering your personal information incorrectly when placing an order

As we alluded to above, there are certain pieces of information that need to match up in order for a tradeline to post to your credit report, such as your name and address. In order for the banks and credit bureaus to verify your identity and link the tradeline to the correct credit profile, the personal information you provide when buying tradelines needs to be 100% accurate, or else there is a chance that your tradelines will not post.

Unfortunately, people often make mistakes when typing in their names and addresses, which can result in their tradelines not posting. Be sure to double-check all of your information for accuracy and correct any typos before placing your order to ensure that your tradelines post to your credit report.

Although we are proud to have the best posting rate in the industry, we can’t prevent the occasional non-posting because unfortunately, the banks and the credit bureaus are not always 100% accurate in their reporting processes.

If your Credit Karma credit report has been updated after the last date within the reporting period and your tradelines still haven’t posted, you can follow these instructions to request a refund or exchange for the non-posting tradeline.

When buying tradelines, use some best practices to get your tradelines to post so there is a lower chance of having to deal with a non-posting.

Still feeling unsure about tradelines? Check out our Tradeline FAQs.

What mistakes have you seen when it comes to authorized user tradelines? Are there any common mistakes that you would add to this list?

Credit repair can be a long and arduous process, especially if you have very bad credit. Getting results from credit repair can take months, and it takes years to build or rebuild a solid credit history.

However, there are some “credit hacks” that you can use to improve your credit on a much shorter time scale.

In this article, we’re going to tell you the best credit hacks to improve your credit score as well as credit card hacks that work to help you save you money on interest. In addition, we’ll also provide some credit-building hacks for those with thin credit files and credit repair hacks to help you fix bad credit.

Here are the credit hacks we’ll be covering in this article. You can click on the bulleted list items below to jump directly to each hack.

Now let’s delve deeper into each credit of these credit hacks.

Credit Score Increase Hacks

Pay down high-balance cards first to improve your credit utilization

If your focus is primarily on boosting your credit score fast, you may want to consider paying down your high-balance cards first. The reason for this can be explained by the importance of individual credit utilization ratios, which refers to the utilization ratios of each of your revolving accounts.

From what we have seen, individual utilization ratios may be even more important than your overall utilization ratio. Having one or more maxed-out accounts, for example, can drag down your score even if your overall utilization ratio is low.

Therefore, by paying down your high balances first, you can get those accounts out of the high-utilization danger zone and into a utilization range that is less damaging to your credit score.

Pay off low-balance accounts to reduce the number of accounts with balances

One of the factors that are considered within the overall “credit utilization” category is the number of accounts that have balances. Having fewer accounts with balances is better for your score. In fact, the ideal credit utilization scenario is having a zero balance on all but one of your accounts and having one account with a utilization ratio in the 1-3% range.

Therefore, if you can pay some of your accounts down to zero, you should see a boost to your score. Accounts with small balances are low-hanging fruit because you don’t have to spend as much money to get them to a zero balance.

Time your payments so that you have a $0 balance on your statement date

To ensure that your credit report shows low credit utilization, time your payments so that you have a low balance (or no balance) when your accounts report to the credit bureaus.

When it comes to credit utilization, you might think that as long as you pay your credit card balance in full by the due date every month, then you should show a 0% utilization for that account. However, this assumption is not necessarily correct. The reason for this is that the date when your credit card issuer reports to the credit bureaus is often not the same as your due date.

That means that your account is reporting at some other time during the month when your card does have a balance on it. If you use a significant portion of your credit limit, that utilization could be hurting your score.

To correct this, if you want to have your accounts show a 0% utilization ratio, try using this credit hack: Instead of waiting for your statement to arrive and then paying your balance on the due date a few weeks later, you need to pay your balance to $0 before the statement closing date. Then, your statement will close with a $0 balance and that’s what will report to the credit bureaus.

Alternatively, you can pay your bill on your normal schedule and then refrain from using your card for the next entire billing cycle. Since you have paid off the balance and not made any new charges, your account will show a $0 balance at the end of the reporting cycle.

Either way, if you can shift the timing of your payments so that your account reports a 0% utilization, that could provide a significant benefit to the credit utilization portion of your credit score.

Credit-Building Hacks

Build credit fast by piggybacking on someone else’s good credit

One of the easiest and fastest ways to build credit is called credit piggybacking, which refers to the practice of becoming associated with someone else’s good credit for the purpose of helping you build your own credit history.

Piggybacking credit can help you build credit quickly, whether you open a joint account, get a cosigner, or become an authorized user.

There are three main ways to piggyback credit.

Get a co-signer or guarantor

Having a co-signer or guarantor with good credit can go a long way toward helping you qualify for credit because the co-signer or guarantor is essentially promising to assume responsibility for the debt if you default.

The downside of this strategy is that since the position of the co-signer or guarantor comes with a lot of risks, it can be difficult to find someone to take on this role for you.

Open a joint account

Since both applicants are considered when opening a joint account, you can benefit from your partner’s good credit as well as the fact that the income of both applicants can be counted. If you maintain the joint account for a while, this can allow you to build up a credit history with a primary account.

However, many banks no longer offer joint credit cards, so your options for opening a joint account may be limited. Plus, if your relationship with the other account holder ever takes a turn for the worse, it can make managing the account difficult, and you may end up needing to close the account altogether.

Become an authorized user

Becoming an authorized user on a seasoned tradeline (i.e. a credit account that already has at least two years of positive payment history associated with it) is the fastest way to build credit. Instead of opening your own primary account and waiting for it to age, you can add years of credit history to your credit profile within a few weeks or even days.

Consider applying for a credit-builder loan

If you have bad credit or if you have never used credit before, you might be feeling discouraged about the prospect of getting credit anytime soon. It can feel impossible to get credit if you have a thin credit file or a history of derogatory marks on your credit report.

A credit-builder loan can be a useful tool for those struggling to build credit. Here’s a summary of how they work:

Credit-builder loans are typically for small amounts (e.g. a few hundred to a thousand dollars).

A credit-builder loan functions like a backward version of a traditional loan: instead of receiving the funds upfront and paying the money back later, you first make all of the monthly payments and then receive the loan disbursement once you have already paid off the loan. For this reason, these types of loans are low-risk for lenders, which is why even those with bad credit or thin credit can still qualify (provided your income is sufficient for you to make the monthly payments).

The lender reports your payment history to one or more of the major credit bureaus, which allows you to build a credit history.

For more information on how these loans work and whether a credit-builder loan might be a good strategy for you to consider, check out our article, “Credit-Builder Loans: Can They Help You?”

Credit Card Hacks

Increase your credit limit

Increasing your credit limit is one of the best credit hacks. Check out our article for more tips on how to request a credit line increase.

Increasing your credit limit can be one of the easiest and fastest ways to boost your credit score. However, you’ll want to strategize a little before requesting credit line increases from your lenders.

If your financial situation has improved since opening your credit cards, it might be a good time to request a credit line increase. For example, if you have received a raise at work or your credit score has increased, that could indicate to lenders that you can handle a higher credit limit responsibly.

Wait until you have been a responsible cardholder for at least six months and you don’t have too many inquiries on your credit report to make your request. Also, don’t request an increase if you have already requested one within the past six months.

Check with your credit issuer to see whether they will need to do a hard inquiry or soft inquiry. If you don’t want to get a hard inquiry on your credit report, ask if there is an amount they may be able to approve without doing a hard pull on your credit.

You can make your request for a credit limit increase online or over the phone. Be prepared to provide some financial information and to explain why you are asking for additional credit. Calling your bank and talking to a representative may give you more opportunities to negotiate than if you make the request online.

So, how does this hack improve your credit score?

Your credit utilization ratio, also called your debt-to-credit ratio, makes up about 35% of your FICO score and about 20% of your VantageScore. It’s defined as the ratio of how much debt you owe to the amount of credit you have available. This can be calculated for your revolving credit accounts in aggregate by adding up all of your balances and dividing by the sum of all your credit limits for those accounts.

Ask your credit card issuers for lower interest rates

This is another credit card hack that is easier and quicker than you might think. All you need to do is call up each of your credit card issuers and ask them to lower your interest rate.

Try calling your credit card issuers and asking for lower interest rates—odds are good that they will grant your request.

Again, you’ll want to do a little homework before asking for a lower interest rate. Research interest rates on cards from other issuers and see if your bank can match a lower number. Explain why you’ve been a good customer and why you feel your rate should be lowered. Also, describe how your financial situation may have improved since you opened the card.

You can find a detailed script to help you negotiate on creditcards.com.

Although this tip doesn’t directly affect your credit score, it can still be hugely beneficial, especially if you are one of the 37% of American households that carry balances on their credit cards from month to month.

Lowering your interest rate decreases the debt burden that comes from interest charges each month, allowing you to pay off your debt faster. Paying off your debt faster means improving your utilization ratio, which leads to a better credit score!

Although this hack isn’t guaranteed to work, the worst that could happen is that your lenders deny your request and your interest rates stay the same. On the other hand, it could save you hundreds or even thousands of dollars in interest. Plus, you can be optimistic about your chances: polls show that over three-quarters of consumers who ask for a lower interest rate are successful in their request.

Set up automatic bill payments

Setting up automatic payments is one of the best things you can do for your credit, especially if you struggle to remember due dates or if you have accidentally missed payments in the past. Payment history is the number one factor that influences your credit score, so even one late payment can have a serious impact on your credit.

Setting up automatic payments for all of your accounts can help prevent you from accidentally missing a payment.

Take human error out of the equation by setting up automatic payments for all of your loans and credit cards. That way, you’ll never accidentally miss a payment, so you can continue to build up a positive payment history each month without even thinking about it.

Pay down high-interest balances first to save money on interest and pay off debt faster

When it comes to paying off debt, the way to save the most money on interest is to pay off your high-interest balances first. This method is called the “debt avalanche” because you’re starting with the highest interest rates and working your way down from there. (In contrast, the “debt snowball” method involves paying your debt in order of smallest to largest balances).

Transfer your balances to a card with a lower interest rate

Another popular way to get some relief from paying those astronomical interest charges every month is to transfer your credit card balances to another credit card that has a lower interest rate.

This hack works best if you have good enough credit to qualify for a balance transfer credit card. These credit cards are marketed specifically for this purpose and they typically come with special introductory offers, such as 0% APR on balance transfers for a certain number of months.

A balance transfer can help you save money on interest charges and may improve your credit utilization ratio.

Here’s how the balance transfer process works:

When you apply for the balance transfer credit card, you tell the credit card issuer the amount you want to transfer and which bank(s) you want to transfer a balance from.

Once you have been approved for the balance transfer card, the credit card issuer essentially pays off your balances at the other banks with the credit on your new card.

Your debts (plus a balance transfer fee, usually around 3-5%) have thus been transferred to your new card.

Since your balance transfer card likely has a low promotional interest rate or perhaps even zero interest for a while, you have some extra time to pay off your debt without being crushed by interest, which means you can pay off your debt faster.

As a bonus, this credit card hack can also help your credit utilization, because you are adding some available credit to your credit profile by opening a new account.

The pitfall to watch out for with this method is that it opens up the possibility of you running up your credit cards again and potentially ending up even deeper in debt than you were before. If you think having access to additional credit is going to tempt you to spend more, then it’s probably best for you to avoid this credit hack.

Credit Repair Hacks and Bad Credit Hacks

Dispute inaccurate information on your credit report (such as inquiries or derogatory items)

Check your credit report for errors that could be damaging your score and dispute them with the credit bureaus.

If you have any errors on your credit report that are bringing your score down, such as credit inquiries or derogatory items that don’t belong to you or are otherwise being reported incorrectly, then this hack could definitely give your credit a boost.

First, you need to obtain a copy of your credit report to check for errors. You can order one from each of the three credit bureaus for free once a year at annualcreditreport.com and you can order your Innovis credit report for free directly from their website.

Then, thoroughly check your credit report for any inaccuracies, such as late payments that you actually made on time, duplicate accounts, or negative information that is more than seven years old (which means it should have been deleted by the credit bureaus already).

To fix the errors on your credit report, you can dispute the items with the credit bureaus by following the instructions found on each of your credit reports. However, there are a couple of other things you should keep in mind in order to ensure your dispute process goes smoothly.

Look up a sample credit dispute letter, such as the sample letter offered by the Federal Trade Commission, that you can use as a model for writing your own letters.

Write one dispute letter for each credit report error and send in your letters one at a time. If you try to dispute several items at once, you run the risk of the claim being dismissed as “frivolous.”

Be sure to include as much evidence as possible that supports your claim when submitting your dispute. Without documentation proving that the item is being reported incorrectly, the credit bureaus could dismiss your dispute.

Send your letters along with the necessary documentation via certified mail so that you can get proof that the bureaus received them. In addition, you should also talk to the creditor that is reporting the inaccurate date to the credit bureaus in order to fix the problem at the source and prevent the error from showing up on your credit report again in the future.

Once the credit bureaus receive your dispute letters, they have 30 days to investigate the issue. If they cannot verify the information to be accurate, then they have to either update the item with the correct information or remove the item from your credit report.

For this credit hack, dispute collection accounts on your credit report that are inaccurate or outdated to have the credit bureaus update them or delete the collections altogether.

As we discussed above, if a collection account on your credit report is being reported incorrectly or doesn’t belong to you, then you can certainly dispute the inaccurate information and have the credit bureaus update or remove the item.

If, on the other hand, the collection accounts on your credit report are legitimate, then your options for removing them are limited.

Some consumers try to negotiate a “pay for delete” arrangement with the debt collector, in which the debt collector agrees to stop reporting the collection to the credit bureaus in exchange for you paying some or all of the debt. However, this strategy is risky and it does not always work in the consumers’ favor. If you do try this approach, be sure to get the agreement in writing from the collection agency.

In addition, deleting a paid account might not even increase your credit score depending on which credit scoring algorithm is being used. Simply paying the collection may be enough to boost your credit score, since some scoring models (FICO 9, VantageScore 3.0, and VantageScore 4.0) don’t penalize you for having paid collections on your credit report.

If you want to delete a collection account without paying it, unfortunately, your only legitimate option is to wait for the collection to be removed from your credit report automatically, which happens seven years after the date that you were first delinquent on the account.

Time your credit inquiries carefully when shopping for credit

If you’re planning to shop for credit in the future, you’ll probably be getting some hard inquiries from lenders on your credit report.

Lenders typically need to check your credit history before they can decide whether or not to extend you credit, so when you apply for a loan or credit card, the lender will often request a “hard pull” of your credit report from one or more of the credit bureaus.

While it’s unlikely that inquiries alone will ruin your credit score, since each inquiry can potentially subtract a few points from your credit score, it is still important to be mindful of the frequency and the timing of your credit applications in order to minimize the impact of inquiries on your credit report.

Thankfully, though, you can still shop around for the best loan without being punished by the credit scoring algorithms. FICO and VantageScore know that it’s financially smart to shop for the best rates, not risky. Therefore, they each have ways of accounting for this behavior so that your loan applications don’t have an outsize impact on your credit score.

When applying for credit, try to minimize the impact of credit inquiries by grouping your applications within a specific time frame.

FICO scores group together inquiries that occur within a certain time frame for student loans, auto loans, and mortgages. Older FICO scores allow a 14-day window for consumers to apply for multiple loans of the same type (such as mortgages), while newer FICO scores allow a 45-day window.

Each inquiry for the same type of loan within the given time period gets grouped together and only counted as a single inquiry. However, note that this rule does not apply to credit cards, for which each inquiry will be counted separately.

With VantageScore, all inquiries that are made with a 14-day period are grouped together, regardless of the types of accounts—even credit cards.

To simplify this information into a general rule, if you can complete all of your hard credit inquiries for a given type of loan within 14 days of each other, then the inquiries will be grouped together and you can avoid ending up with way too many inquiries on your credit report.

Get a rapid rescore from your mortgage lender

Once you’ve tried some of these credit hacks and optimized your credit report, the fastest way to see your results reflected in your credit score is to get a rapid rescore. For those who are about to apply for a mortgage but need to quickly update their credit report first, a rapid rescore can be an extremely valuable tool.

To trigger a manual update of your credit report, obtain verification of your tradeline’s new status from your creditor and then forward the letter to the credit bureaus.

Since rapid rescores can only be provided by mortgage lenders, if you’re not in the market for a mortgage but you need to update your credit report in a hurry, you’ll need to update your tradelines manually.

To do so, once you have made the desired changes to your tradelines (e.g. paying down your balances or correcting errors), contact your creditors and ask them to send you a letter verifying the new account information. Then, forward this letter to the credit bureaus so they can update the information in your credit report.

By initiating the update manually, you can bypass the period of time that you would otherwise have to wait until your next reporting period.

Conclusions on Hacks to Improve Your Credit

While there is no substitute for the time and effort required to establish and maintain a respectable credit history, that doesn’t mean that you can’t try some of these credit-boosting hacks to help you improve your credit right away and perhaps even save some money on credit card interest and fees.

Just make sure not to lose sight of the most important goal, which is to build good credit over time and keep your credit report in good condition long-term.

Let us know what you think of these credit hacks! Which are the best credit hacks in your opinion? Do you have any creative credit hacks that you would add to this list?

What is the difference between your overall credit utilization ratio and individual utilization ratios and why does it matter to your credit? Keep reading to find out.

Credit utilization makes up 30% of a FICO score.

What Is Credit Utilization?

To put it simply, credit utilization is the amount of debt you owe compared to the amount of your available credit. In other words, it is the amount of your available credit that you are actually using.

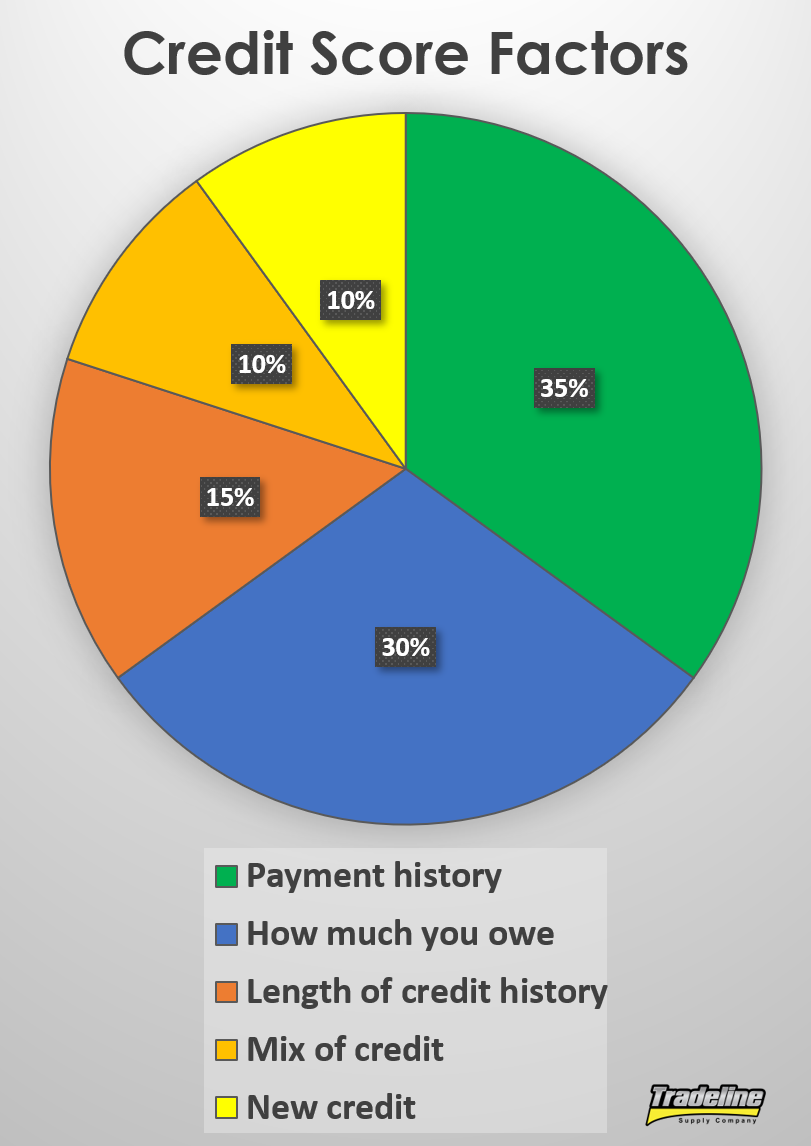

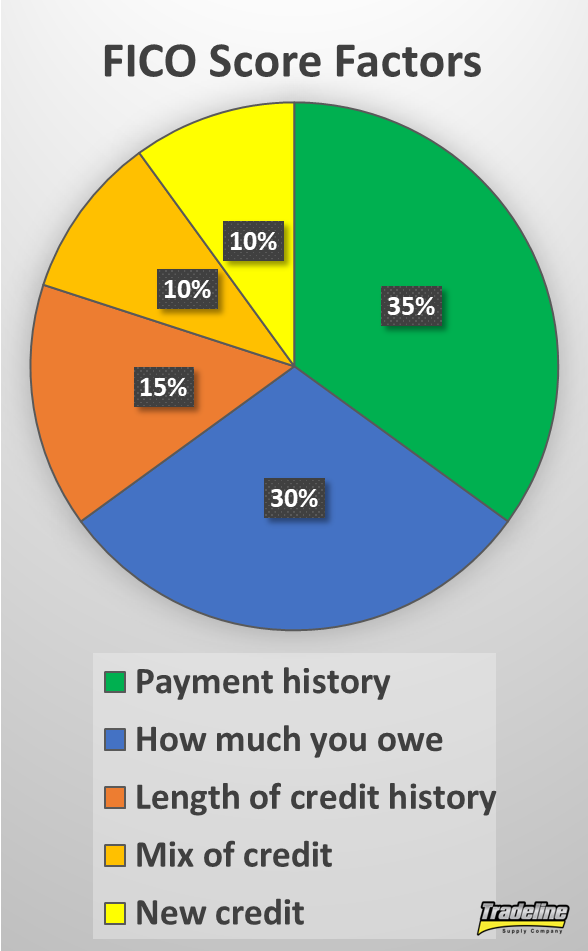

In terms of your credit score, credit utilization makes up 30% of your score, second only to payment history.

The reason credit utilization is such an important part of your credit score is that the ratio of debt someone has is highly indicative of whether they will default on a debt in the future. The more you owe, the harder it becomes to pay off all that debt on time every month, which makes you a riskier bet for lenders.

Components of Credit Utilization

According to FICO, there are several components that fall within the category of credit utilization, such as:

The total amount you owe on all accounts (overall utilization)

The amount you owe on different types of accounts

The utilization ratios of each of your revolving credit accounts (individual utilization)

The number or ratio of your accounts that have balances

The amount of debt you still owe on your installment loans (e.g. mortgages, auto loans, student loans)

What Is the Difference Between Individual and Overall Utilization?

Your overall utilization ratio is the amount of revolving debt you have divided by your total available revolving credit.

For example, if you have one credit card with a $450 balance and a $500 limit and a second credit card with a $550 balance and a $3,500 limit, your overall utilization ratio would be 25% ($1,000 owed divided by $4,000 available credit).

However, the individual utilization ratios of your respective credit cards are 90% ($450 balance / $500 credit limit) and 16% ($550 balance / $3,500 credit limit).

Since credit scores consider individual utilization ratios, not just overall utilization, having any single revolving account at 90% utilization is going to weigh negatively on the credit utilization portion of your score.

Overall Utilization May Not Be as Important as You Think

Typically, when people think of the effect that credit utilization has on credit scores, they often assume that overall utilization is the only important variable.

By this assumption, it would be fine to have individual accounts that are maxed out as long as the overall utilization is still low.

Individual utilization ratios may be more important than the overall utilization ratio.

However, we have seen that this is often not true.

For example, sometimes clients with maxed-out credit cards will buy high-limit tradelines in order to reduce their overall utilization ratio, but then they don’t see the results they were hoping for.

This means that the individual accounts with high utilization are still weighing heavily on the clients’ credit scores, despite the fact that they have improved their overall utilization. In other words, the decrease in the overall utilization ratio did not make much of a difference.

Cases like this seem to indicate that overall utilization may not play as big a role as traditional wisdom has led us to believe and that the individual utilization ratios may be more important.

Although the age of a tradeline is often its most valuable asset, tradelines can still help with some of the credit utilization variables.

Since our tradelines are guaranteed to have utilization ratios that are at or below 15%, this means that at least 85% of that tradeline’s credit limit is going toward your available credit, which helps to lower your overall utilization ratio. In fact, most of our tradelines tend to maintain utilization ratios that are much lower than 15%.

Buying tradelines also allows you to add accounts with low individual utilization to your credit file, which can help to improve the number of accounts that are low-utilization vs. high-utilization.

As a general rule of thumb, simply aim to keep your utilization as low as possible. However, you might be surprised to learn that having a zero balance on all revolving accounts is actually not the best scenario for your score.

According to creditcards.com, “…the ideal scenario tends to be having all but one card show a zero balance (zero percent utilization) and having one card with utilization in the 1-3 percent range.”

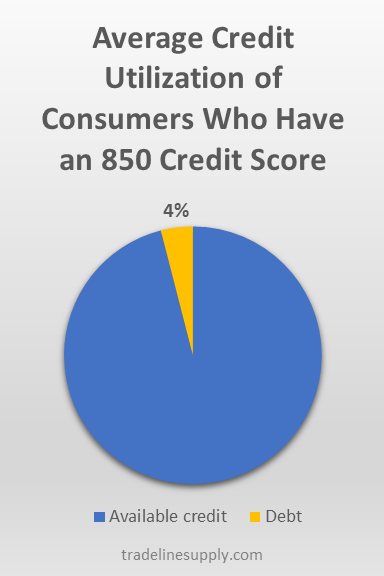

The average credit utilization ratio of consumers who have an 850 FICO score is about 4%.

Why? As it turns out, consumers with a 0 percent utilization ratio actually have a slightly higher risk of defaulting than those with low (but more than 0) utilization. A 0 percent utilization indicates that a consumer may not use credit regularly, which leads to the consumer having a higher risk of default in the future.

However, your utilization doesn’t necessarily have to fall in line with the above scenario in order to have a perfect credit score. In “How to Get an 850 Credit Score,” we found that consumers with FICO credit scores of 850 have an average utilization rate of 4.1%.

For those of us who use credit regularly, however, maintaining a minuscule balance may not always be practical. So what is a realistic threshold to shoot for?

While you may hear the figure 30% cited frequently, many credit experts say this is a myth and that you should aim for 20%-25% instead.

Tips to Avoid Excessive Revolving Debt Utilization

Spread out your charges between different cards

Since we have seen that it’s important to keep individual utilization ratios low, one strategy to accomplish this is to make your purchases on a few different credit cards instead of charging everything to one card. Spreading out your charges helps to prevent an excessively high balance from accumulating on any one individual card.

Pay off your balances more frequently

If you spend a lot on one of your cards, consider spreading out your charges between different cards or paying down the balance more often.

If you do spend a lot on one card, it helps to pay off your balance more than once a month. If your card reports to the credit bureaus before you have paid off your balance, it will show a higher utilization than if you had paid some or all of the balance down already.

You can either time your payment to post just before the reporting date of your card or you can make payments several times per month. Some people even prefer to pay off each charge immediately so their card never shows a significant balance.

Set up balance alerts to monitor your spending

To prevent mindless spending from getting out of control, try setting up balance alerts on your credit card. Your bank will automatically notify you when the balance exceeds an amount of your choosing, so you can back off of spending on that card or pay down your balance.

Don’t close old accounts

Even if you don’t use some of your old credit cards anymore, it’s often a good idea to keep the accounts open so they can continue to play a positive role in your overall utilization ratio and the number of accounts that have low utilization vs. high utilization.

Ask for credit limit increases

Another way to decrease your utilization ratios is to call your credit card issuers and ask them to increase your credit limit. By increasing your amount of available credit, you decrease your utilization ratio, both on individual cards and overall.

Keep in mind that your bank may do a hard pull on your credit to decide whether or not to grant your request, which could ding your score a few points temporarily. However, the small negative impact of the credit inquiry could be offset by the benefit of the credit line increase.

Also, this might not be an ideal strategy if you think you will be tempted to spend the new credit available to you, which could leave you even worse off than you started.

If you want to learn more about how you can successfully ask for credit line increases, check out our article, “How to Increase Your Credit Limit.”

Open a new credit card

Like asking for a higher credit limit, opening a new credit card can also lower your credit utilization, provided you leave most of the credit available.

Again, this will add an inquiry to your credit report, as well as decrease your average age of accounts, so this could have a negative impact on your score temporarily, which may be outweighed by the decrease in your credit utilization.

Transfer your credit card balances to different cards

A balance transfer is when you use available credit from one credit card account to pay off the balance on another credit card, thus “transferring” your debt balance from one card to another.

There are two ways to do this: you can transfer a balance to another credit card you already have, as long as it has enough available credit, or you can transfer a balance by applying for a new credit card and letting the card issuer know in your application which account you want to transfer a balance from and how much you want to transfer.

The latter option is best for your credit utilization, since opening a new credit card means you are adding available credit to your credit profile. In addition, it gives you the opportunity to apply for specific balance transfer credit cards, which usually come with low promotional interest rates on the balances you transfer.

However, using an existing account to do a balance transfer can still be beneficial if done properly, because it can help your individual utilization ratios. Just make sure the account you are transferring the balance to has a higher credit limit than the account that is currently carrying the balance in order to keep the individual utilization ratios as low as possible on each account.

Pay down smaller balances to zero

Having too many accounts with balances can bring down your score since credit scores consider the number of accounts in your credit file that are carrying a balance. If you have any accounts with smaller balances, paying those down to zero will decrease the individual utilization ratios on those accounts, reduce your overall utilization ratio, and reduce the number of accounts with balances, thus improving your credit profile in multiple ways.

People who are serious about improving their credit often wonder what it takes to get the highest possible credit score. For the FICO 8 credit scoring model, the perfect credit score is 850.

As of April 2019, only about 1.6% of scorable consumers in the United States have the elusive 850 credit score, which is actually an increase from 0.98% in April 2014 and 0.85% in April 2009.

There are many other credit scoring models that are used for different purposes and may have different credit scoring ranges. However, since FICO 8 is the most commonly used credit score, we will use the number 850 as the benchmark for the ideal credit score.

Check out the infographic below for some fast facts on how to get the highest credit score possible, then keep reading the article for even more tips on getting the coveted 850 credit score.

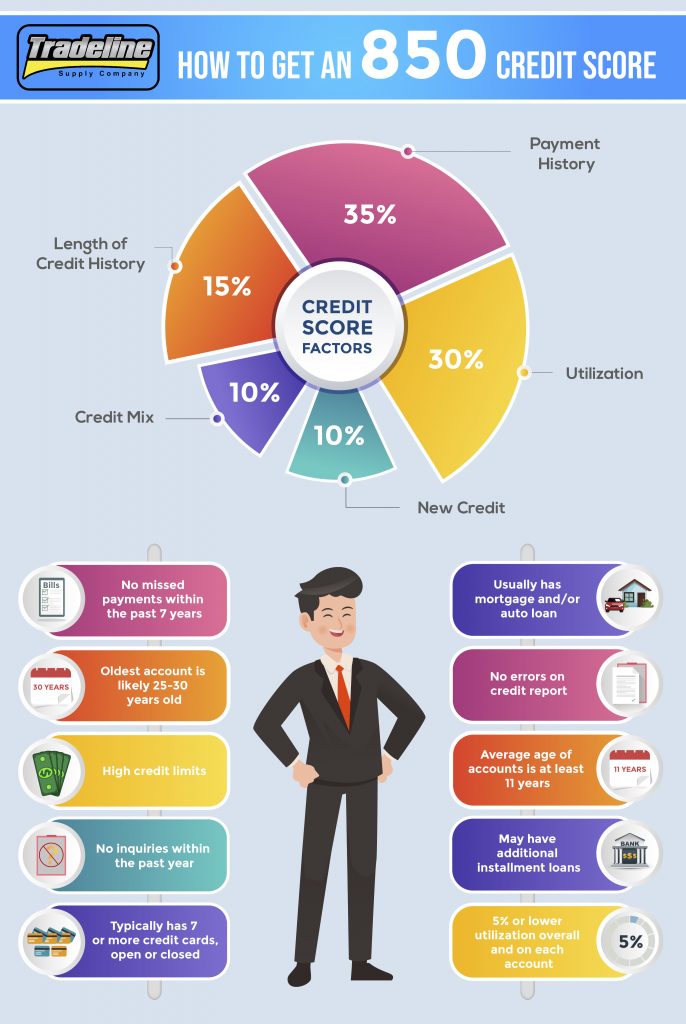

Payment History — 35%

Most people who have an 850 credit score have seven years of perfect payment history.

Your payment history is the biggest slice of the credit score pie, so even one late payment or missed payment can significantly affect your score. Negative items can stay on your credit report for up to seven years, so if you miss a payment, you may not be able to achieve a perfect 850 credit score until at least seven years have passed!

To safeguard against the possibility of forgetting to make a payment, consider setting up automatic bill pay for all of your accounts. Be sure to continue to check your accounts regularly in case of any system errors.

If you do miss a deadline once in a blue moon but have otherwise been an upstanding customer, try negotiating with your creditor to see if they will forgive the late payment and wipe it from your record.

FICO says that 96% of “high achievers,” or those with FICO scores above 785, have no missed payments on their credit report.

Essentially, to get an 850 credit score, you just need to follow one simple strategy: make all of your payments on time for a long time. We will further discuss the connection between payment history and time in the “Length of Credit History” section below.

Credit Utilization/How Much You Owe — 30%

The amount of debt you owe compared to your total credit limit is your credit utilization ratio. To get a perfect credit score, you’ll want to keep this ratio as low as possible, both overall and on each of your individual tradelines.

A study by VantageScore and MagnifyMoney found that people with the best credit scores and people with the worst credit scores actually had similar amounts of outstanding debt. However, those with the best scores had an average total credit limit of $46,700—16 times the credit limit of those with the worst scores!

Therefore, for the high scorers, that outstanding debt made up a much smaller percentage of their total available credit than those with low credit limits and poor scores, which highlights the importance of the overall utilization ratio.

This study reported that the average credit card user has an overall utilization ratio of 20%, which is generally considered to be a safe number for maintaining decent credit. To become someone who has an 850 credit score, however, you’ll need to keep it around 5% or lower. As of 2019, FICO says that the average revolving utilization for those with the “850 profile” is 4.1%.

While consumers with 850 credit scores do use credit cards, they tend to keep their utilization ratios around 5% or lower. Photo by Ellen Johnson.

In addition, keep in mind that even if you have a low overall utilization ratio, individual cards with high utilization could still bring down your score. You can read more about this in our article on individual vs. overall credit utilization ratios.

As a hypothetical example, let’s say you have two cards: one with a $10,000 limit and a $0 balance and the other with a $1,000 limit and a $900 balance. Your total available credit is $10,000 + $1,000 = $11,000 and your total debt is $900. Therefore, your overall utilization ratio is $900 / $11,000 = 8% utilization, which is a very good number.

However, your account with the $1,000 limit has a 90% individual utilization ratio! Since you only have two accounts, that means 50% of your accounts have high utilization, and that could negatively affect your credit. According to creditcards.com, maxing out just one credit card can reduce your score by as many as 45 points.

To get around this problem, if you have any individual cards with high utilization, consider transferring the balance to other accounts to keep the utilization ratio on each account as low as possible.

You could also request credit line increases from your creditors, which can lower your utilization ratios and benefit your score. Try using the tips we provide in “How to Increase Your Credit Limit.”

Another way to help with overall utilization is to add low-utilization tradelines to your credit file.

Optimizing this factor also means not closing old accounts even if you don’t use them very often, because their credit limits could be helping your score. To ensure old accounts don’t get automatically closed by the banks for inactivity, try to use them every 1-2 months, perhaps for small, recurring bills.

Length of Credit History (Age) — 15%

This category takes into account age-related factors such as the average age of your accounts, the age of your oldest account, and the ratio of seasoned to non-seasoned tradelines. (A seasoned tradeline is an account that is at least two years old, which is when the account is believed to have a more positive impact on your credit.)

Age goes hand-in-hand with payment history, because the more age an account has, the more time it has had to build up a positive or negative payment history. Together, age (15%) and payment history (35%) make up 50% of your credit score, which shows how important it is to open accounts early and make every single payment on time.

According to FICO, the age of the oldest account of people who have 650 credit scores is only 12 years, compared to 25 years for people who have credit scores above 800. In addition, individuals with fair credit have an average age of accounts of 7 years, compared to 11 years for those with excellent credit.

Cultivating an 850 credit score takes years of maintaining a positive credit history.

FICO reports that the average age of the oldest account of consumers who have 850 credit scores is 30 years old.

We have an in-depth discussion of which age tiers are most significant in our article, “Why Age Is the Most Valuable Factor of a Tradeline,” but the bottom line for getting the best credit score is simply to get as much age as possible. Seasoned tradelines can help by extending the age of the oldest account and the average age of accounts.

Also, keep in mind that it may be impossible to achieve an 850 credit score without a certain amount of age, even if you do everything else perfectly. So if you have stellar credit habits but haven’t yet been able to join the 850 credit club, you may just need to wait patiently for your accounts to age.

Credit Mix — 10%

While the mix of credit is one of the least important factors in a credit score, to get a perfect credit score of 850, you will still need to consider this factor.

In this category, credit scores reward having a balanced mix of several different accounts, including both revolving credit and installment loans. This is because creditors want to see that you can successfully manage a variety of different types of credit.

As an example, a credit file that includes an auto loan, a mortgage, and two credit cards has a better credit mix than a credit file that has four accounts that are all credit cards.

About the “credit mix” credit score factor, FICO says, “Having credit cards and installment loans with a good credit history will raise your FICO Scores. People with no credit cards tend to be viewed as a higher risk than people who have managed credit cards responsibly.”

The total number of accounts is also considered, with more accounts generally being better, up to a certain point.

FICO also states that high score achievers have an average of seven credit card accounts in their credit files, whether open or closed.

Auto loans are common among people who have 850 credit scores.

If you are looking to improve your credit mix statistics, adding authorized user tradelines can increase the total number of accounts and help diversify one’s credit file.

850 scorers also have installment loans in their credit files. According to Experian, the average mortgage debt for consumers with exceptional credit scores (800 or above) is $208,617. In addition, people who have FICO scores of 850 have an average auto-loan debt of $17,030.

Experian says, “In every other debt category except mortgage and personal loan, people with perfect scores had more open tradelines but less debt than their counterparts with average scores—underscoring the value of being able to manage debt while having numerous credit accounts.”

The “new credit” category of your credit score refers to how frequently you shop for new credit. This includes opening up new credit cards and applying for loans, for example. This “new credit” activity is reflected in the number of inquiries on your credit report.

Since seeking new credit makes you look like a higher risk to creditors, each hard inquiry has the potential to drop your score by a few points. Therefore, if you are going for a perfect 850, it’s best to avoid applying for new credit for a while.

However, it is possible to score an 850 with hard inquiries on your record. FICO recently stated that around 10% of 850 scorers had one or more inquiries within the past year, and about 25% had opened at least one new credit account within the past year.

If you need to shop for an auto loan or mortgage, be sure to complete all your applications within a two-week window in order for all of the credit pulls to count as one inquiry. For credit cards, however, each inquiry will be typically be counted individually.

Fortunately, inquiries only remain on your credit report for two years, and FICO scores only consider inquiries that occurred within the past year, so it shouldn’t take long for your credit to recover if you do have new inquiries on your credit report.

Inquiries aren’t the only thing that matters when it comes to the new credit factor of your credit score, however. It also includes data points such as the number of new accounts you have, the ratio of new accounts vs. seasoned accounts, and the amount of time that has passed since opening new accounts. The main idea if you want to maximize your credit score is to not open too many new accounts at once, which can make you look riskier to lenders and bring down your score.