Can Inquiry “Bumpage” and “Choppage” Help Your Credit?

Some folks in the field of credit repair claim that hard inquiries can be “bumped” or “chopped” off of your credit report through the processes of inquiry “bumpage” and “choppage.”

Some folks in the field of credit repair claim that hard inquiries can be “bumped” or “chopped” off of your credit report through the processes of inquiry “bumpage” and “choppage.”

What do these terms mean, and do they actually work?

Credit expert John Ulzheimer, who has worked in the credit industry for 30 years, gave us his take on this trend in a Credit Countdown video on our YouTube Channel. We’ve outlined the main points of the video for you in the article below.

How Much Do Inquiries Impact Your Credit Score in the First Place?

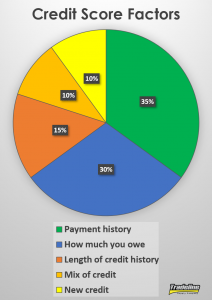

Credit scores factor in five categories of information when calculating your score, and they are not all given equal weight.

The most important piece of the credit score pie chart is your payment history, or in other words, your track record of making your payments on time. This factor accounts for 35% of your FICO credit score.

The next largest piece is how much debt you owe, which relies heavily on your revolving utilization metrics, among other factors. Your debt comprises 30% of your credit score.

Your length of credit history, AKA your credit age, represents 15% of your score, while credit mix, or your diversity of types of credit accounts, makes up 10%.

Finally, the last 10% of your credit score comes down to the new credit category, which includes hard inquiries.

For this reason, focusing on trying to remove inquiries from your credit report usually does not make sense as a credit improvement strategy. Even if you are 100% successful in removing all of the hard inquiries that may be bringing down your credit score, you will only move the needle a small amount relative to what you could accomplish by focusing on the more important credit score factors.

What Is Inquiry Bumpage?

The concept behind credit inquiry “bumpage” is the idea that the credit bureaus only have a certain amount of space allocated for each consumer’s credit report. Therefore, the theory goes, if you can fill that limited amount of space with new information, you can “bump” the oldest inquiries off of your credit report.

What Is Inquiry Choppage?

Inquiry “choppage” is theoretically what happens when the soft inquiries get “chopped” or removed from your credit report before the hard inquiries can be “bumped” off.

Do Inquiry Bumpage and Choppage Really Work?

According to John Ulzheimer, aside from the speculation and marketing tactics you may see in credit repair space online, there is no reason to believe that bumpage and choppage even happen in the first place, let alone that they are effective strategies to help get hard inquiries removed from your credit report.

Better Ways to Increase Your Credit Score

While the methods of bumpage and choppage are not recommended when trying to improve your credit, fortunately, there are more legitimate and effective things you can try.

Remove inaccurate derogatory information. If there is damaging information on your credit report that is not supposed to be there, filing a dispute to get it removed or corrected should be your top priority.

Pay your bills on time. Since your payment history has the greatest amount of influence on your credit score, getting more on-time payments onto your credit report will go a long way toward attaining a higher credit score.

Maintain low balances on your credit cards. Factors having to do with the amount of debt you owe also play a sizeable role in determining your credit score, and your credit card utilization ratios are the key metrics in this category. The lower your credit card balances are, the higher your credit score can climb.

Limit the number of accounts that have balances on your credit report. In addition to utilization ratios, credit scoring models also consider how many of your accounts have balances on them. Even if the balances are small, if you have too many accounts with balances, this can bring down your credit score.

Increase your credit age. All you have to do to increase your credit age is wait patiently for your accounts to get older!

Plus, try some of the other credit tips we’ve published in our Knowledge Center, such as our list of easy credit hacks that will actually get you results.

Read more: tradelinesupply.com