Credit sweeps are a heavily advertised and promoted service among credit repair companies. Unfortunately for many unsuspecting consumers looking to improve their credit, the credit sweep is a fraudulent and illegal practice.

John Ulzheimer, one of the nation’s most prominent credit experts, explains why you need to watch out for credit sweep scams in an episode of Credit Countdown.

Disclaimer: The views and opinions expressed in this article are strictly those of John Ulzheimer and do not necessarily reflect the official stance or position of Tradeline Supply Company, LLC. Tradeline Supply Company, LLC does not sell tradelines to increase credit scores and does not guarantee any score improvements. Tradelines can in some cases cause credit scores to go down.

Credit Repair: Legal vs. Illegal

To be clear, credit repair as a whole is not illegal. Credit repair—the legal kind at least—is simply the process of removing inaccurate or unverifiable information from a consumer’s credit report. This is done by disputing the negative items with the credit reporting agencies (CRAs, AKA credit bureaus). Alternatively, credit report information may be challenged through the financial institution that is furnishing the data to the CRAs.

Credit repair is legal as long as it complies with federal and state rules and laws that govern the industry of credit repair.

Hiring a Credit Repair Company to Fix Your Credit

Although the credit dispute process is free to everyone, consumers who want help repairing their credit can choose to pay a credit repair company to try to get negative information removed from their credit reports.

Although trustworthy credit repair professionals do exist, there are also plenty of “scumbags,” in John’s words, in the industry who take advantage of consumers and use illegal and fraudulent practices to make money.

For this reason, it’s extremely important to do your due diligence before deciding to work with a credit repair company.

The Credit Dispute Process

Typically, the credit repair process involves sending letters on the behalf of consumers to challenge the validity of the data in question and ask the CRAs to validate the items. This process is not illegal; it is commonly used and has been around for decades.

Disputes Under the Fair Credit Reporting Act

The Fair Credit Reporting Act (FCRA) gives you the right to dispute information on your credit reports that you believe to be incorrect. If you do challenge an item on your credit report, the credit bureaus are required to perform an investigation. They then look into your claim and determine if the dispute is valid or if the challenged information can be verified as correct.

Section 605B of the FCRA

Section 605B of the FCRA is a section that is entitled “Block of Information Resulting From Identity Theft.”

This section of the FCRA states that if you have been the victim of identity theft and someone else has fraudulently opened accounts in your name, then you have the right to have the fraudulent information resulting from identity theft removed from your credit reports.

In addition, in the event of identity theft, Section 605B obligates the CRAs to do two things that are not normally required as a part of removing negative information:

They have to remove the fraudulent information from your credit report within four business days of receiving all of the valid documentation that proves identity theft has occurred. This is a very short period of time in comparison to the 30-45 days that are typically allowed for the credit bureaus to complete their investigations and remove the information. They have to block the information from ever appearing on your credit reports again.

Scammers have abused this section of the FCRA by selling a service that takes advantage of these policies even when identity theft is not the cause of negative information appearing on someone’s credit report.

What Is a Credit Sweep?

This particular scam that disreputable credit repair companies often engage in is called the credit sweep.

The goal of a credit sweep is to cause the credit bureaus to remove negative information from your credit reports prior to the time that they are legally required to do so. The FCRA mandates that negative information must be removed from a credit report after seven years (with the exception of a Chapter 7 bankruptcy, which can stay on your credit report for up to 10 years).

A credit repair company tries to get the negative marks deleted from your credit report immediately rather than waiting until it is seven years old, when it will automatically be taken off of your credit report.

How Do Credit Sweeps Work?

The way a credit sweep works is the credit repair company asks you to pretend that you have been the victim of identity theft so that they can get the credit bureaus to remove accurate, valid negative information from your credit report.

The credit repair company has you go to an enforcement agency such as the police and file a police report claiming that your identity has been stolen. They can then show the identity theft report to the credit bureaus as “evidence” that the negative information on your credit report is there as a result of your identity being stolen.

If the credit sweep is successful, the CRAs have to remove all of the implicated negative information within four business days and prevent it from ever reappearing on your report, thus “sweeping” all the negative items off of your credit report.

Credit Sweep Fraud

As John puts it, it is clear that credit sweeps are fraudulent and illegal.

Not only are you lying to the CRAs, but also to the police, and filing a false police report is against the law.

In addition, lying to the credit bureaus and then defaulting on your credit obligations can land you in court, criminally charged with fraud.

Conclusions on Credit Sweeps

Is it worth it to try to fix your credit by purchasing a credit sweep and possibly being prosecuted for fraud? Or is it a better idea to pay your bills on time so that negative information does not hit your credit report in the first place? It’s up to you to consider the pros and cons.

If you learned something from this article, please share it so that others can be aware of the dangers of credit sweep scams.

You can watch the Credit Countdown video below. Find more content like this on our YouTube channel and in our Knowledge Center!

Derogatory entries on your credit report, such as 30-day late payments, 60-day late payments, collections, and more, can seriously damage your credit score. Is there a way to get derogatory items removed from your credit report so that your score can bounce back? Let’s find out.

What Are Derogatory Entries on Your Credit Reports?

The term derogatory simply means negative, so derogatory items on your credit report are any items that reflect negatively on your credit. In other words, they indicate that you have failed to make timely payments on your debt.

Derogatory entries can be divided into two categories: minor derogatories and major derogatories. They both can hurt your credit substantially and contribute to bad credit, but major derogatory items have a greater negative impact on your credit score than minor derogatory items.

Examples of Derogatory Items on Your Credit Reports Minor Derogatory Entries

30-day late payments 60-day late payments

Major Derogatory Entries

90, 120, 150-day late payments, etc. Charge-offs Collections Foreclosures Settlements Short sales Repossessions Public records (bankruptcies)

A bankruptcy on your credit report counts as a major derogatory entry.

The Good News: You Can Dispute Inaccurate Derogatory Information on Your Credit Reports

As a consumer, you have the right to have your credit reports be accurate, as dictated by the Fair Credit Reporting Act (FCRA).

Therefore, if there is information on your credit reports that is wrong, then you have the right to ask for the incorrect information to be either corrected or removed from your credit reports.

In order to challenge inaccurate information on your credit reports, you can file a direct dispute with the party that furnishes your data to the credit bureaus (e.g. a lender, financial services company, debt collector, etc.) or an indirect dispute with the credit reporting agencies (CRAs).

If you choose to go the route of an indirect dispute, you contact the CRAs about the problematic information and they then investigate the dispute with the company that is furnishing the data.

You can use either type of dispute to ask for the inaccurate derogatory information on your credit report to be corrected or deleted altogether.

The Bad News: You Do Not Have the Right to Have Accurate Negative Information Removed From Your Credit Reports

According to the FCRA, accurate and verifiable negative information can remain on your credit reports for up to seven years.

Unfortunately, that means if the derogatory information on your credit reports is accurate and verifiable, then the CRAs are under no obligation to remove it before the 7-year clock runs out.

Derogatory information that is accurate and verifiable can stay on your credit report for up to seven years.

How to Dispute Derogatory Entries on Your Credit Reports

It is free to dispute inaccurate information on your credit reports, and you can do this process yourself. Another option is to hire a reputable credit repair company to do this work on your behalf.

If you choose to complete the dispute process yourself, you can do this in a few different ways:

Go to the CRAs’ websites and file your dispute online

Mail your dispute through the postal services Contact the CRAs over the phone Dispute the information directly with the furnishing party

You can submit your disputes online on the CRAs’ websites.

Which Dispute Method is Most Effective?

While there is not necessarily a “best” way to file a dispute, often, plaintiff’s lawyers advise consumers to file their disputes with the credit bureaus because this method may leave you in a better positioned to take legal action if the credit bureaus fail to remove the incorrect information.

The Benefits of Disputing Directly With the Furnishing Party

When you file a direct dispute with the company that is furnishing the inaccurate information to the credit bureaus, you are addressing the information at its source. For this reason, the data furnisher has an obligation to correct the error with all of the CRAs they report to.

If a mistake is showing up on more than one of your credit reports, the direct dispute strategy can save you some time since you are only filing one dispute to have the information corrected on each of your credit reports where it is applicable.

Working With a Credit Repair Company to Remove Derogatory Information

Although the consumer credit dispute process is free to use, some consumers may choose to work with a credit repair company to accomplish their goals.

In this case, the credit repair company goes through the dispute process on your behalf.

While a credit repair organization cannot charge you in advance of providing a service as per the Credit Repair Organizations Act (CROA), if they successfully get the information corrected or removed, they can then charge you for this service that has been fully performed.

How Do You Know if You Need to Dispute Incorrect Information on Your Credit Reports?

To find out if there are errors on your credit reports, you need to get copies of your own reports.

Typically, you can do this for free once every 12 months with each of the three credit bureaus. However, due to the COVID-19 pandemic, the CRAs have made it easier to check your credit more often by making it free to check your credit reports every week until April 20, 2022.

To order your free credit reports, go to annualcreditreport.com, which is the only website that is federally authorized to provide your free credit reports, and request them there.

How Long Does the Dispute Resolution Process Take?

The credit bureaus are technically allowed to take 30 days to complete their dispute investigation process, but this rule is decades old. These days, with the technology we have now, it is more likely that your dispute will be resolved in only 10-14 days.

Consumer disputes are usually resolved within two weeks.

We hope this article has been informative for those wondering about how to get derogatory information removed from your credit reports! To learn more about how to use credit report disputes effectively, check out our article on How to Fix the Most Common Credit Report Errors.

Want to see the video version of this article, featuring credit expert John Ulzheimer? Watch it below and then subscribe to our channel on YouTube to see more helpful videos about the credit system!

Most of us have credit reports assembled about us by the credit bureaus, yet few of us know about the surprising history of credit reporting.

The credit bureaus as we know them today grew from small, local organizations that formed as far back as the 1800s. In contrast, modern credit bureaus market themselves as expansive repositories of consumer information that can be used for an ever-growing number of applications.

Unfortunately, the early credit bureaus were known to use unethical tactics to collect information on consumers and sell this information to businesses.

While it may seem that the problems of these early credit bureaus have been addressed by legislation such as the Fair Credit Reporting Act, the credit reporting system still has serious flaws, some of which we highlight in “What Happened to Equal Credit Opportunity for All?”

In this article, we will explore the story of how credit reporting began, including how the credit bureaus originated and evolved into what they are today, and the many scandals that have taken place along the way.

What Is a Credit Report?

A credit report contains information about a consumer’s credit history. This includes a list of current and past credit accounts, along with the age, credit limit, balance, and payment history of each account.

It also contains identifying information such as your name, address, and social security number.

This information helps lenders evaluate the creditworthiness of potential borrowers so they can decide whether to extend credit and what the terms of the loan should be.

Credit bureaus, also known as credit reporting agencies or CRAs, are the companies that gather credit-related information about consumers and distribute it to lenders—and increasingly, other types of businesses who have an interest in checking people’s credit history.

In the United States today, there are three major credit bureaus: Experian, Equifax, and TransUnion. While there are many other credit bureaus, these three companies dominate the industry.

But it wasn’t always this way. The first credit reporting organizations were a far cry from the modern credit bureaus of today, and the unsavory tactics they used to run their businesses may surprise you.

Early Credit Reporting Agencies

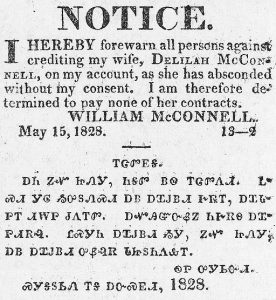

The first recorded group that shared credit information about consumers was the colorfully named “Society of Guardians for the Protection of Trade Against Swindlers and Sharpers,” which was founded in London in 1776. The Society produced reports for its members on the credit history of individual customers, which were often full of gossip in addition to credit information.

The earliest credit reporting “agencies” were groups of merchants who would get together to gossip about customers. Painting by Joseph Highmore, public domain.

Credit bureaus would check local newspapers for news about consumers.

Like the Society, the early credit reporting agencies were small, local organizations that were essentially groups of merchants sharing information about consumers. This allowed them to offer credit to more people and avoid lending to high-risk individuals.

These organizations were industry-specific and did not share information with each other. In 1960, it is estimated that about 1,500 independent local credit bureaus were in operation in the United States.

The bureaus didn’t just collect the information you might expect, such as name and loan information. They also gathered sensitive personal information such as marital status, age, gender, race, religion, employment history, and driving records.

The credit bureaus didn’t stop there. They checked the local newspapers for announcements of promotions, marriages, arrests, and deaths, and attached news clippings to consumers’ credit reports. They would even go so far as to ask someone’s neighbors and colleagues for testimonies about that person’s character.

Even the local “Welcome Wagon” was working undercover for the credit bureaus. This organization would surreptitiously gather information on new residents of an area under the guise of welcoming them to the neighborhood.

The “Welcome Wagon” would secretly collect information on new neighbors for the credit bureaus. Photo by John Fowler on flickr, CC BY 2.0.

The credit bureaus were focused solely on serving the local creditors that belonged to their respective organizations. As such, they typically only reported derogatory information.

Furthermore, there was no standardized way to evaluate a person’s creditworthiness. It was all based on the subjective whims and prejudices of the creditor looking at their credit file.

What’s worse is that the credit bureaus did not allow consumers to view the information that was being reported about them. There was no way for consumers to verify whether the information was correct or where it came from.

Modernization of Credit Reporting

According to the Harvard Business School paper, over the course of the 1960s, many of these small, local credit bureaus started to join together, forming networks that spanned the nation.

In 1971, the Fair Credit Reporting Act (FCRA) was passed to ensure the “accuracy, fairness, and privacy of information in the files of consumer reporting agencies.”

By establishing requirements as to the accuracy and of consumer credit files and access to their information, the FCRA was intended to protect consumers from the unfair practices that were rampant in the credit reporting industry.

The Fair Credit Reporting Act

The FCRA enacted the following rights for consumers:

Consumers must be notified if negative action is taken against them because of the information in their credit file. Consumers must be able to find out what is in their credit file. Consumers must be able to dispute inaccurate information and have it corrected or deleted. Outdated information (generally more than 7-10 years old for negative information) cannot be reported. Consumers must provide consent for employers to check their credit reports. Consumers must have the option to request to be excluded from lists for unsolicited credit and insurance offers. Consumers who appear on a list of prospects requested by a lender must be extended a firm offer of credit.

As a result of the passing of the FCRA, credit bureaus stopped recording events such as marriages and arrests and started focusing more on verifiable credit history information. They also started reporting positive information in addition to negative information.

In 1996, the FCRA was amended to extend additional protections to consumers, including the following:

Consumers have the right to take legal action against anyone who obtains their credit report without a permissible purpose. Credit bureaus can be held liable for knowingly reporting misinformation. Credit bureaus must investigate disputes within a certain period of time, usually 30 days. Banks can share credit information with affiliates, but consumers must be given the opportunity to prohibit this sharing of their information.

The transition to computerized databases allowed some credit bureaus to expand and dominate the industry.

The advent of computer-powered databases allowed some credit reporting agencies to become more efficient and do more business, while smaller agencies that could not afford to make the change got out of the industry.

This consolidation eventually led to the domination of the market by the three major bureaus we know today.

Experian

While Experian did not officially come about until 1996, according to creditrepair.com, the story of Experian can be traced back almost 200 years.

The Manchester Guardian Society was formed in England in 1826 to share information on customers who didn’t pay their debts. This organization eventually became a part of Experian, as did a group of merchants that later formed in Dallas for a similar purpose.

These groups were both acquired by TRW, an engineering and electronics conglomerate that also launched their consumer credit reporting branch as Experian.

Experian was acquired by the British retail company Great Universal Stores Limited (GUS) and became part of their consumer credit reporting arm. In 2006, it demerged from GUS and began trading on the London Stock Exchange.

Although Experian as we know it today did not come along until after the FCRA was passed, the bureau has certainly not been free of controversy.

In 1991, a TRW investigator incorrectly reported that 1,400 people in Vermont had not paid their property taxes, which ruined the credit of those consumers. Several similar cases were discovered throughout New England.

Experian became infamous for their atrocious customer service and was hit with several lawsuits.

Later, Experian settled with the Federal Trade Commission (FTC) for operating a credit reporting scam in which consumers were led to believe they were signing up for a “free credit report” and were not told that they would automatically be enrolled in Experian’s $80 credit monitoring program.

The offending for-profit website, FreeCreditReport.com, is still in operation. As a reminder, the only site authorized to provide free credit reports as required by federal law is annualcreditreport.com.

They settled with the FTC again in 2005 for violating their previous settlement.

In 2015, Experian announced a data breach that existed for over two years and affected as many as 15 million consumers.

The bureau was then fined $3 million in 2017 for deceiving customers about their credit scores, along with TransUnion and Equifax.

TransUnion

TransUnion originally began as the holding company for a rail transportation equipment company in 1968. One year later, they entered the credit reporting industry by acquiring regional credit bureaus. The bureau has expanded steadily since then, although it is the smallest of the three major credit bureaus.

TransUnion has also been guilty of taking advantage of consumers.

Two consumers have sued TransUnion for refusing to remove inaccurate information on their credit reports.

They have also been accused of scamming consumers by not notifying them that they would be charged $18 a month for having a TransUnion account.

In June 2017, the largest FCRA verdict to date forced TransUnion to pay $60 million in damages to consumers who were erroneously included on a government list of terrorists and security threats.

Later in 2017, one of TransUnion’s websites was hijacked and made to redirect consumers to websites that attempted to download malware onto visitor’s computers.

Equifax

Equifax was started as Retail Credit Company by a grocery store owner. Photo by Charles Bernhoeft, public domain.

Equifax was started in 1898 by a grocery store owner who created a list of creditworthy customers and sold the list to other businesses. This business grew and became known as the Retail Credit Company.

The company expanded quickly throughout North America, amassing credit files on millions of Americans by the 1960s.

The Retail Credit Company developed a reputation for collecting extensive personal information on consumers and selling it to just about anyone who wanted it.

Critics accused them of reporting “facts, statistics, inaccuracies and rumors’…about virtually every phase of a person’s life; his marital troubles, jobs, school history, childhood, sex life, and political activities.”

Buyers of these reports would use them to judge the morality of individuals and avoid lending to those who they perceived as morally corrupt.

Consumers were not allowed to see their information, and many had no idea that the company had files on them in the first place.

When the company started planning to computerize their records, which would make consumer information more widely available, the U.S. Congress intervened, holding hearings that led to the Fair Credit Reporting Act being passed.

Equifax had to stop scamming consumers by lying about their identity and their motives when collecting information, among many other changes.

The Retail Credit Company changed its name to Equifax in 1975, which many speculate was a move to improve their damaged reputation after the congressional hearings.

Unfortunately for consumers, Equifax’s issues didn’t end with the Fair Credit Reporting Act. In recent years they have betrayed consumers’ trust even more egregiously.

Equifax ruined their reputation again in 2017, when their systems were breached by hackers twice, impacting hundreds of millions of consumers in the United States, Canada, and Britain.

The scam left the names, social security numbers, birth dates, addresses, driver’s license numbers, and credit cards numbers of consumers exposed for months, from May 2017 until July 2017.

Not only that, but Equifax did not disclose the breach until September of that year, giving top executives plenty of time to sell their shares of the company before going public with the announcement.

They continued to bungle their response to the breach by setting up websites that were supposed to allow consumers to determine whether they were affected by the Equifax breach but instead returned random results.

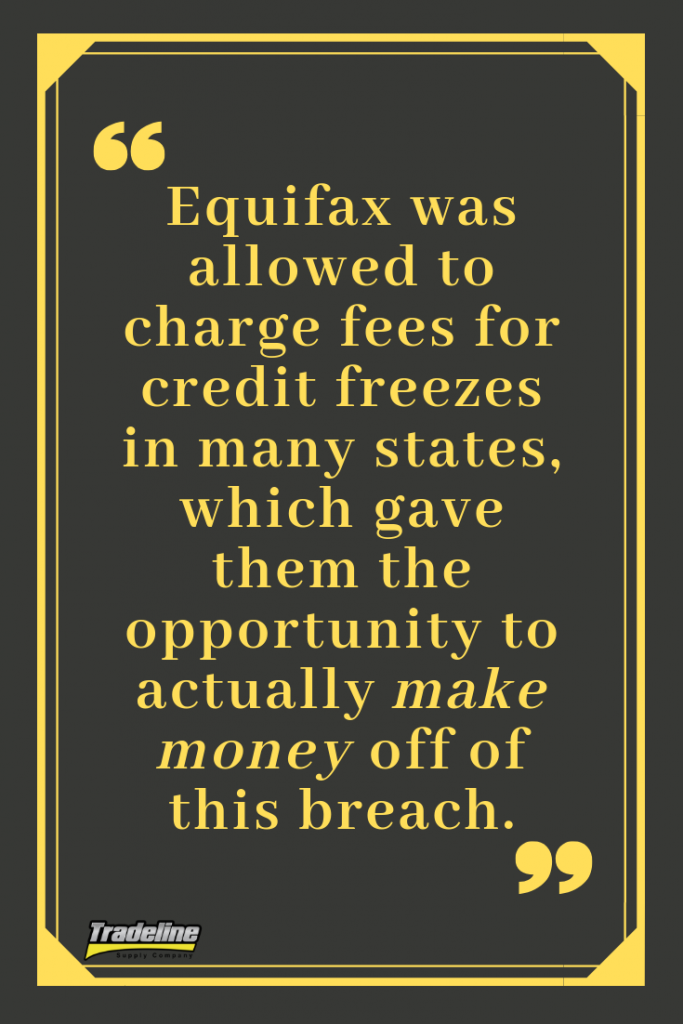

In addition, Equifax was allowed to charge fees for credit freezes in many states, which gave them the opportunity to actually make money off of this breach.

Nearly two years later, Equifax has still not been penalized or held accountable for this horrific failure in any way. In fact, they just went back to selling credit monitoring, and they are now making more money than ever.

For a fascinating in-depth investigation of the 2017 Equifax breach, listen to the podcast “Breach.”

There is virtually no end to the list of disastrous errors committed by Equifax, but here are some more of the highlights:

The bureau repeatedly tweeted a link to a fake Equifax phishing website, directing consumers to enroll in fraud prevention services at the imposter site.

Equifax left their systems vulnerable to a series of cyberattacks that affected hundreds of millions of people.

Equifax left the private data of approximately 14,000 Argentinian consumers and staff members open to anyone who entered “admin” as the username and password for one of its online portals. The company removed its mobile apps from app stores in 2017 because they had security flaws that left them vulnerable to cyber attacks. A website operated by Equifax exposed the salary histories of tens of thousands of people to anyone that had someone’s Social Security number and date of birth, both of which were in the hands of criminals after the security breach. In October 2017, Equifax’s website was hacked and made to serve malware disguised as a software update, leaving visitors to the site at risk of having their computers infected by the malware. The company has been sued hundreds of times and fined millions of dollars by the Federal Trade Commission for violating the FCRA.

Sadly, it seems Equifax has not changed for the better since their early days of selling people’s private information to anyone and everyone, since they have allowed criminals to easily access consumer data on a massive scale.

Innovis: The Fourth Credit Bureau

Many people are completely unaware that there is actually a fourth major credit bureau called Innovis. It was founded as Associated Credit Bureaus in 1970 and changed its name to Innovis in 1997. The company is now owned by CBC companies, which purchased Innovis in 1999.

In contrast to the other consumer reporting agencies (CRAs), credit reporting is not the primary function of Innovis. In fact, Innovis does not even offer credit scores.

Innovis instead serves businesses by providing “consumer data solutions” such as identity verification, fraud prevention, receivables management, and credit information. According to finance writer Sarah Cain, Innovis’ credit reports are used primarily to compile lists of pre-approved consumers to sell to lenders for marketing pre-screened offers.

Innovis also states on their website that as a CRA, they “enable” personal solutions such as credit reports, credit disputes, fraud alerts, active duty alerts for consumers in the military, credit blocks, security freezes, and opt-outs.

What Is In Your Innovis Credit Report?

Your Innovis report, like your other credit reports, contains your personal information as well as your credit history. However, they do not receive credit information from all of the same lenders that report to the other three major credit bureaus. If you pull your Innovis credit report, you may notice that some of your credit accounts are missing, particularly revolving accounts.

Your credit report will also show inquiries if any businesses have pulled your file from Innovis.

While you can’t get your Innovis credit report from annualcreditreport.com, you can order a copy directly from the company for free once a year.

Who Uses Innovis Credit Reports?

While there are some anecdotal reports of credit card companies pulling consumers’ Innovis credit reports for lending decisions, it seems that their reports are used mostly for pre-screened marketing offers. Innovis’ services are also used by companies such as cell phone service providers.

Is CBCInnovis the Same Company?

Confusingly, there is another company owned by the same parent company as Innovis called CBCInnovis. Although CBCInnovis and Innovis share similar names, they are different companies with different functions.

Unlike Innovis and the other credit bureaus, CBCInnovis does not maintain a repository of consumer credit data. Rather, it serves as a third-party company that pulls consumers’ credit reports from Experian, Equifax, and TransUnion and compiles the information into one “tri-merge” credit report. These tri-merge reports are sold to lenders such as banks and mortgage companies.

Discrimination in Credit Reporting

Unfortunately, historical discrimination is still baked into the credit system.

You might think that discrimination in the credit system is a thing of the past, left behind with the shady information-gathering tactics of the earliest credit bureaus.

Unfortunately, although discrimination is officially prohibited by the Equal Credit Opportunity Act, inequality is still rampant in the credit industry today.

Past and present discrimination against minorities in the United States affects consumers in ways that have dramatic effects on credit scores. A study by the Federal Reserve Board revealed that on average, blacks and Hispanics have lower credit scores than non-Hispanic whites and Asians, even after controlling for personal demographic characteristics, location, and income.

The credit system further burdens those who are less privileged and provides very few opportunities for disadvantaged consumers to improve their situation.

Conclusion on the History of Credit Reporting

Credit reporting agencies have a surprisingly long and sordid history. From the 1800s to today, the consumer credit reporting industry has been plagued with bias, inaccuracies, and serious security issues.

While technological advancements have allowed the credit bureaus to expand and improve, and government regulation has been enacted to protect the rights of consumers, the system is still far from perfect.

Ultimately, the credit bureaus were built to serve lenders, not consumers, and that remains their primary purpose. We are reminded of this every time consumers are harmed by the incompetent or even outright malicious actions of the credit bureaus.

Have you been affected by a credit reporting scam or a security breach? Let us know in the comments, and please share this article if you liked it!

Credit sweeps are a heavily advertised and promoted service among credit repair companies. Unfortunately for many unsuspecting consumers looking to improve their credit, the credit sweep is a fraudulent and illegal practice.

Credit sweeps are a heavily advertised and promoted service among credit repair companies. Unfortunately for many unsuspecting consumers looking to improve their credit, the credit sweep is a fraudulent and illegal practice. Derogatory entries on your credit report

Derogatory entries on your credit report