Bad credit is something we all fear, but what is actually considered poor credit and how could it affect you? In addition to explaining what bad credit is and why you need to avoid it, we’ll also provide some strategies in this article to help you fix bad credit.

What Is a Bad Credit Score?

The definition of “bad credit” varies depending on which credit scoring system you are talking about. Since FICO 8 is the scoring model most widely used by lenders, we will focus on FICO when discussing the question of what is considered bad credit.

The FICO 8 credit scoring system assigns consumers a number to represent their creditworthiness, with the lowest credit score possible being 300 and the high end of the scale being 850.

A high credit score shows lenders that they can be fairly confident that a consumer will repay debts because they have demonstrated responsible behavior when it comes to credit in the past.

A low credit score, on the other hand, means that someone represents a higher risk to lenders because they are thought to have a higher probability of defaulting on a loan.

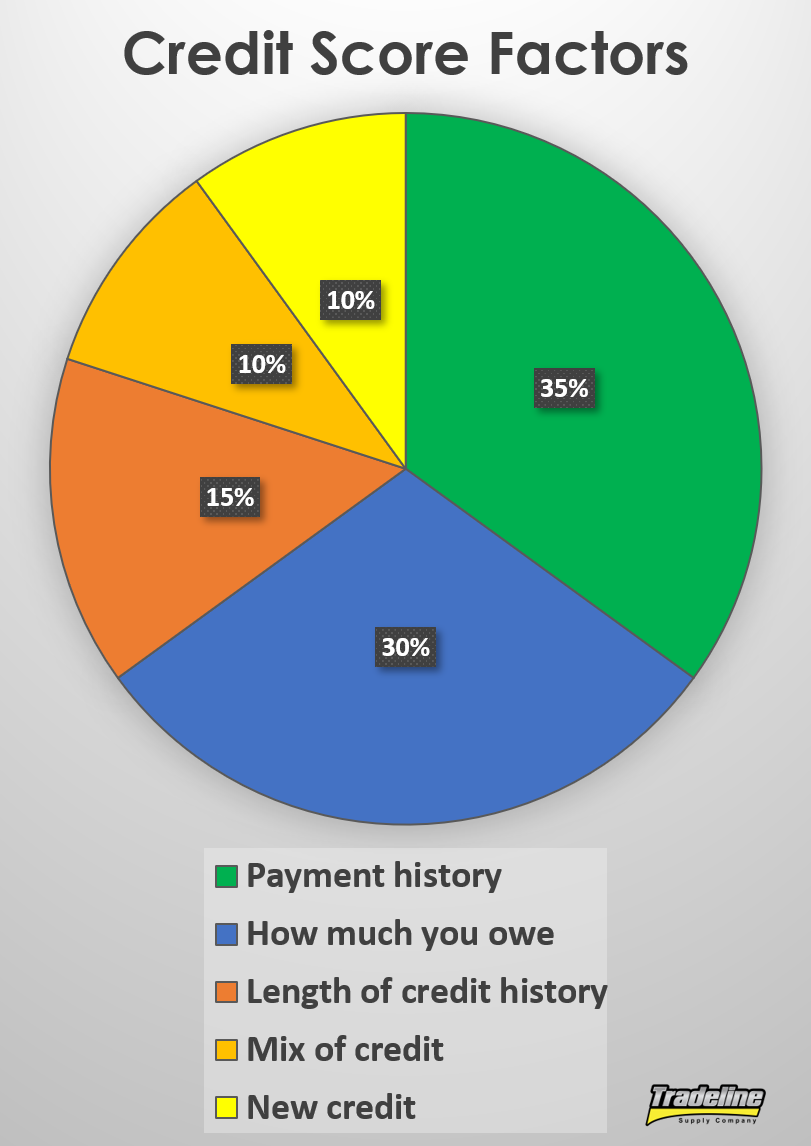

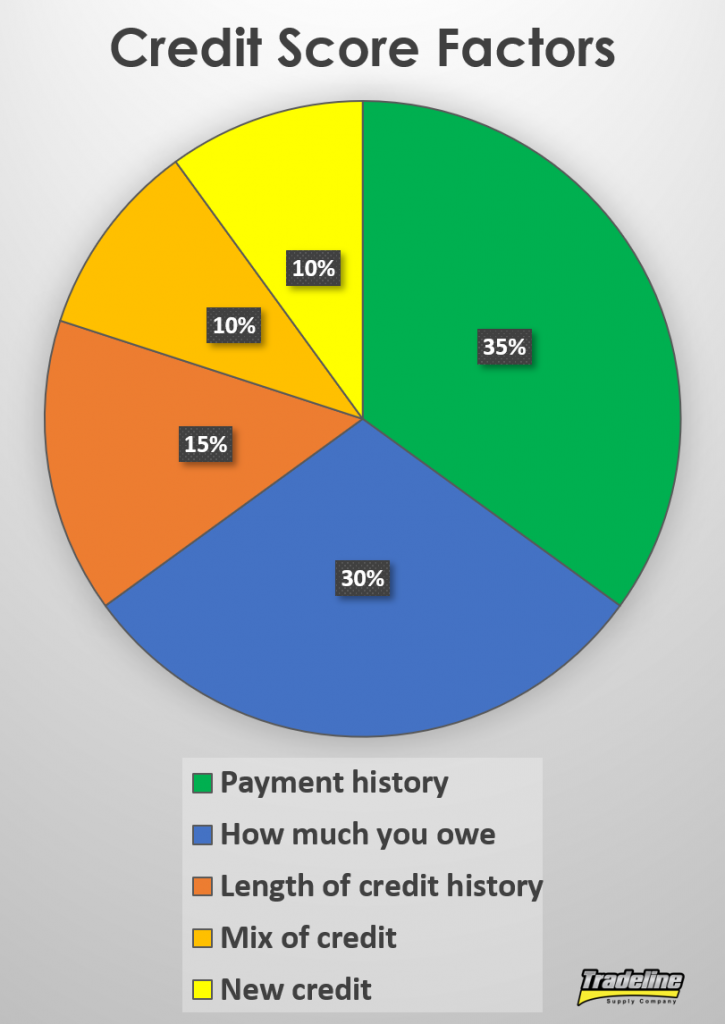

According to Credit Karma, a FICO score between 300 to 579 is considered a poor credit score, while a fair credit score is between 580 and 669. In contrast, an excellent credit score is between 800 and 850.

Credit scores between 300 and 579 are considered poor credit.

What Gives You Bad Credit?

As we mentioned, a bad credit score means lenders perceive you as a high-risk borrower. Therefore, what causes bad credit is poor management of credit and risky behaviors that indicate you may have a higher probability of default.

For example, being late on payments or missing payments altogether can really hurt your credit because payment history is the most important factor of a credit score.

High credit card utilization can lead to bad credit. Photo by Natloans

What causes bad credit specifically? Here are some more examples:

Late or missed payments

Defaulting on a loan

Charge-offs Collection accounts

Judgments

Settlements

Bankruptcy

Foreclosures or repossessions

Maxed out or high-utilization credit cards

Too many inquiries at one time

Too much new credit

Sometimes people have bad credit because of things they can’t control, like having a medical emergency that leads to huge hospital bills that they can’t afford to pay. In fact, the majority of consumer debt in collections is medical debt, according to Magnify Money.

Bad Credit Loans

If you have bad credit, you’re likely going to have a hard time getting loans with favorable terms or possibly even getting approved for a loan in the first place. Since a bad credit score represents a high risk for the lender, loans for people with poor credit typically have higher interest rates and may require collateral or a down payment—if the lender is willing to approve the loan at all.

Personal Loans for Bad Credit

Payday loans can come with interest rates of up to 400%. Photo by Aliman Senai.

Personal loans for bad credit are few and far between. Usually, at least fair credit is needed to be considered for a loan. Bad credit loan lenders may charge very high interest rates since they are taking on a lot of risk by lending money to someone with poor credit. These higher interest rates may translate into thousands of dollars of additional interest payments over the term of a loan.

Very bad credit loans such as payday loans often have astronomical interest rates of up to 400%, which makes it nearly impossible for many consumers to get out of debt.

Bad Credit Car Loans

Bad credit auto loans, also known as subprime auto loans, are often considered “second-chance” loans because they are typically the next option for those who have been rejected for traditional auto loans. Although there is not necessarily an official dividing line between which credit scores are considered prime and subprime when it comes to auto loans, credit scores below 620 tend to be considered subprime.

Car loans for bad credit, similar to personal loans for bad credit, are associated with much higher costs than prime auto loans. Since lenders of second-chance auto loans are taking on additional risk, these loans often have significantly higher interest rates and more fees than auto loans for consumers with good credit. Additionally, car loans for bad credit may come with penalties for paying off the loan early.

Bad credit car loans can have triple or more the interest rate as prime auto loans. Photo by QuoteInspector.com.

According to Investopedia, “While there is no official subprime auto loan rate, it is generally at least triple the prime loan rate, and can even be five times higher.”

Credit Cards for Bad Credit

If you have bad credit, your options for getting a credit card will be limited, and you will most likely not be able to get the perks associated with premium credit cards, such as low interest rates, high credit limits, and rewards. Credit cards for poor credit may also come with annual or even monthly fees.

Subprime credit cards often require you to make a deposit with the lender as collateral. These cards are known as secured credit cards since they are secured by your deposit, which the lender can keep if you fail to make payments on the card. Sometimes, the lender may be willing to switch you to an unsecured card after you have shown a history of consistent on-time payments.

As we’ve seen with loans for bad credit, credit cards for bad credit, both secured and unsecured, will likely have high interest rates, sometimes as high as 30% or more.

How to Fix Bad Credit

Having a bad credit score is expensive. It makes getting any kind of credit more difficult and more costly because bad credit lenders tack on high interest rates and fees to compensate for the higher financial risk of poor credit loans.

Bad credit doesn’t just dramatically increase the cost of credit. It can also affect other aspects of your life, such as your insurance premiums, your ability to find housing, and even your job, since many employers now check prospective employees’ credit reports. Therefore, most people with bad credit want to fix it as soon as possible.

Here are some strategies that you can try if you need to fix bad credit.

Credit Repair

If you have bad credit as a result of identity theft or extensive errors on your credit report, you’ll likely need to undergo credit repair in order to clean up your credit file.

Some people opt to try their hand at DIY credit repair, while others may prefer to hire a trusted credit repair company to get help with the dispute process and potentially faster results. [Disclosure: This article contains affiliate links.]

Either way, it’s important to be aware of best practices when disputing credit report errors. It’s best to submit your dispute by sending a letter along with documentation to verify your identity and support your claim. Trying to dispute errors online or over the phone may not yield the best results.

In addition to disputing inaccurate information with the credit bureaus, it’s also important to contact the company that is furnishing the data so that the error doesn’t get reported again in the future.

Rebuilding Credit

Improving bad credit takes time and patience. While credit repair companies may claim to have tactics that can boost your credit fast, the reality is that these tactics are usually limited to removing inaccurate information from your credit report. If you remove everything from your credit report, what are you left with?

The best way to fix bad credit, beyond correcting inaccuracies, is to rebuild it with more positive credit history over time. In other words, you need to add more positive accounts to your credit profile and keep them in good standing while they age. At certain age levels, these accounts should begin to boost your credit profile with that positive payment history.

Rebuilding credit with positive credit history helps to fix bad credit.

One option that can help people re-establish credit is opening a credit-builder loan, which works in the reverse order of a traditional loan. Instead of receiving the loan amount up front and then making payments to the bank to pay off your debt, with a credit-builder loan, you make all the payments first and then receive the funds after you have finished paying off the loan. Since these loans are much less risky for lenders, they can be offered to those struggling with bad credit or lack of credit history.

Generally, though, building credit by opening new accounts can take at least two years to see much of a positive effect. The best way we have seen to bypass this two-year waiting period is by piggybacking on the good credit of others.

Have you been affected by bad credit? What did you do about it? Tell us your story in the comments.

Many people are uncertain about what may happen to their credit when they get married and what can happen to their credit if they get divorced.

For example, it is commonly believed that your credit report merges with your spouse’s credit report when you get married.

Is that really true? And what happens to your credit when you get divorced?

Keep reading for an in-depth explanation of what happens to your credit score when you get married or divorced.

What Happens to Your Credit When You Get Engaged

Technically, nothing directly happens to your credit score as a result of getting engaged. However, becoming betrothed to your future spouse can come with pressure to go into debt, and can thereby indirectly affect your credit.

Financing the Engagement Ring

The first major purchase for a couple planning to marry is often the engagement ring or rings. Many people still hold onto “traditional” ideas about how much one “should” spend on an engagement ring and want to be able to purchase an expensive ring for their partner. The average cost of an engagement ring in 2019 is nearly $6,000!

Those who don’t have the cash on hand to pay for a lavish ring may feel that they need to finance one in order to please their partner or keep up with the Joneses, but be mindful of the impact this could have on your credit.

If you want to take advantage of an in-house financing plan at the store where you are purchasing the ring, you’ll likely have to open a retail credit card with the store. The inquiry on your credit report might ding your credit score by a few points, and the new retail card account will lower your average age of accounts, which is also likely to affect your score.

In addition, if the credit limit of the store card is close to or the same price as the ring, then your individual utilization ratio will be very high or maxed out on that account, and it will also contribute to an increase in your overall utilization ratio. This makes you look riskier to lenders and thus has a negative impact on your credit score.

Before financing an engagement ring, make sure you know how it could affect your credit.

Another way to finance an engagement ring is to take out a personal loan. Taking out an installment loan is generally less damaging to your credit score than opening a new revolving account such as a credit card and maxing it out immediately. However, the downside of taking out a loan to pay for the ring is that you will have to pay interest on top of the price of the ring, whereas with in-store financing you may be able to take advantage of an interest-free promotional offer.

Regardless of how you may choose to finance the jewelry, unfortunately, going thousands of dollars into debt for a ring can bring down your credit score, especially if you become overextended and can’t keep up with the payments.

Paying for the Wedding and Honeymoon

While the cost of an engagement ring can certainly get quite expensive, it typically pales in comparison to the cost of the wedding ceremony and reception.

Planning a wedding involves paying for a venue, catering, photography, flowers, invitations, and much more, and all those expenses can add up quickly. In 2018, the average amount spent on weddings in the United States, not including the cost of the honeymoon, was almost $34,000.

While it used to be commonly expected for parents to foot the bill for weddings, now, spouses-to-be are increasingly paying their own way, even if that means going into debt. Business Insider recently reported that 28% of American couples go into debt to pay for their weddings.

The expenses don’t stop there if you want a traditional honeymoon, which can add several thousand dollars to the total—over $5,000, on average.

The average cost of a wedding in the U.S. is over $30,000, and many couples resort to taking out loans to pay for their nuptials.

Needless to say, on top of the staggering amounts of student loan debt that many couples are already saddled with, spending money you don’t have to shoulder the astronomical cost of a wedding can lead to even more credit struggles.

How Does Marriage Affect Credit?

Although many people seem to believe that your credit report combines with your spouse’s credit report after you tie the knot, this is a misconception. After you get married, both parties still retain their individual credit histories and credit scores. Your partner’s accounts will not be added to your credit report and vice versa.

There is no such thing as a shared credit score for married couples. In fact, your credit report will not even indicate your marital status or your spouse’s name.

Does Marriage Affect Your Credit Score?

No, getting married does not directly affect your credit score. Since your credit report does not change when you get married, neither does your credit score.

However, just like when you get engaged and plan your wedding, your credit may be indirectly affected by your marriage due to financial actions that you may take as a married couple.

Applying for a Mortgage

One of the most important financial decisions a couple can make is whether to apply for a mortgage to buy a home and, if so, whether both parties will apply jointly or whether the spouse with the best credit score will apply individually.

If you get a joint mortgage with your spouse, make sure you are on the same page about who will be responsible for making payments.

If both you and your partner have already established a credit history before entering the marriage, then it is likely that you will have different credit scores. In some cases, your scores may be in the same credit score range, while in others, the gap may be substantial. Ideally, all couples would do well to discuss finances before committing to marriage so that no one is surprised by a bad credit score after you have already taken the plunge.

If one spouse has bad credit while the other does not, the lower credit score could damage your chances of getting approved for a mortgage or getting the best rate on your loan. In this case, it might be a better idea for the spouse with good credit to apply in their name only, or else you could end up owing tens of thousands of dollars more on your mortgage thanks to a higher interest rate.

On the other hand, if your credit scores are similar, then it would probably make sense to apply for the home loan jointly. Assuming both partners have decent credit, then applying for a joint mortgage may offer certain advantages. Namely, both your income and your partner’s income will be considered, which could allow you to apply for a larger loan than if you were just relying on one person’s income.

While getting a mortgage is certainly a huge milestone and financial commitment, since it is a type of installment loan, having a lot of mortgage debt won’t affect your credit as much as revolving accounts do.

However, it’s how you and your spouse manage the mortgage together that can have a significant impact on your credit. With a joint mortgage, both parties are responsible for paying the bill on time. If your partner is in charge of paying the mortgage bill and one month they miss the due date and get a 30-day late, since you are equally responsible for the joint account, that late payment will also show up on your credit report and can bring down your score.

Opening Joint Credit Accounts

Besides applying for a joint mortgage, there are other types of joint credit accounts that married couples may open together, such as joint credit cards or joint auto loans.

This can allow couples to more easily manage their shared finances together. As we discussed in “The Fastest Ways to Build Credit,” if one spouse doesn’t have the credit score to get approved for an account on their own, then applying for a joint credit account with their partner can be a good way to help them build credit.

As with a joint mortgage, opening any other type of joint credit account together means you can both be held fully responsible for the debt. That can be a risky move since it means you can be held accountable and your credit score will suffer the consequences if your partner shirks their financial responsibilities.

Credit piggybacking as an authorized user can help build credit if one spouse’s credit file is thin or less than perfect.

Becoming an Authorized User

When one spouse has better credit than the other, then the partner with good credit can add the other as an authorized user to one or more of their credit cards with positive payment history.

This practice, known as credit piggybacking, often results in the age and payment history of that positive account being added to the credit report of the authorized user. This can be a great way for a spouse to help their partner build credit.

In addition, unlike opening a joint account, it’s low-risk for the authorized user, who can remove themselves from the account at any time if the relationship goes south or the account becomes derogatory.

Does Divorce Hurt Your Credit Score?

Although no one goes into a marriage planning to get divorced later on, unfortunately, divorce is a reality for many couples. To protect your credit, it’s important to be realistic about the possibility of divorce and to keep it in mind when making financial decisions.

Now, let’s answer the question of whether getting divorced can hurt your credit.

If you have been operating under the belief that your credit report merges with your spouse’s when you get married, then you might have assumed that getting a divorce will hurt your credit. However, as we have seen, the act of getting married itself does not affect your credit. It’s how you manage your credit that determines how your credit score might change.

Getting a divorce can be very costly, but if you want to keep your credit in tact, don’t neglect your other bills.

The same idea applies when getting a divorce. Your change in marital status will not be shown on your credit report and will not have any bearing on your credit score. However, it is certainly possible that getting divorced from your spouse can affect your credit by other means.

The Cost of Getting a Divorce

Since you’ll most likely need to hire legal counsel, unfortunately, getting a divorce can often be quite costly. This can make it more difficult to keep up with the rest of your bills. Do whatever you can to pay all of your bills on time so that you don’t end up with any minor or major derogatory items on your credit report.

If you’re really struggling to stay afloat financially in the midst of a divorce, reach out to your creditors and ask if there are any ways in which they can accommodate your situation in this time of financial hardship. For example, some lenders may be willing to lower your payments temporarily or even let you postpone a few payments.

In addition, you could also consider getting a personal loan to help pay for your expenses until you can get back on your feet financially after your divorce.

Managing Your Joint Accounts While Going Through a Divorce

As we discussed previously, many married couples may end up with joint credit accounts, such as a mortgage, an auto loan, or joint credit cards. Getting a divorce doesn’t nullify the debt or release either party from financial responsibility. It’s a legal agreement between you and your ex-partner, not with your creditors. Your joint debts still need to be paid.

In a divorce, it can be hard to resolve who will be responsible for paying off the debt and canceling joint accounts, especially if there are strong emotions at play.

A divorce agreement may dictate who is responsible for paying joint bills, but your lenders can still hold both of you responsible for the debt.

Although a judge may assign certain debt repayment responsibilities to each party, again, this is not an agreement with the lenders, who care only about whether your bills get paid, not who pays them. Both of you can still be held liable for joint debts by the lenders.

If your ex agrees in court to pay off a joint account but doesn’t follow through, those missed payments can damage your credit score just as much as it hurts their own. If the account goes into collections, that could be disastrous for your credit.

Since you may not trust your ex to responsibly manage shared credit accounts, you’ll probably want to pay off and close any joint accounts as soon as possible.

Unfortunately, most lenders don’t allow one person to be removed from a joint account, so you can’t simply convert it to an individual account. Instead, you will most likely need to close the account altogether and then apply for a new account on your own.

As you may know from our article about closed accounts, closing an account hurts your credit utilization. If you have to close any joint credit cards that you had with your ex-spouse, for example, the credit limit of those cards will no longer be factored into your overall utilization ratio. As a result, your utilization is going to go up and your credit score likely could go down, since credit utilization is 30% of your FICO score and about 20% of your VantageScore.

Ideally, you and your ex could decide how to assign responsibility for your joint debts outside the courts. If all goes smoothly when divvying up and paying the debts during your divorce proceedings, then your credit could theoretically remain unscathed aside from the hit to your credit utilization.

However, things can get messy quickly if there is any conflict as to who should pay certain bills.

If your ex decides they don’t want to make payments on a debt that they were supposed to pay, or even if they simply make a mistake and forget to pay, then your credit will suffer from those missed payments unless you pick up the slack. Since payment history is the biggest factor in your credit score, this situation has the potential to destroy your credit.

If your ex-spouse misses a payment on a joint debt, that negative mark will also affect your credit.

Let’s say you didn’t know your ex was behind on payments and the account went to collections. Then you would have a major derogatory on your credit report, through no fault of your own!

What Happens to a Joint Mortgage When You Divorce?

Resolving the question of what happens to your joint mortgage after your divorce can also get tricky, but there are several options to consider. Each of these options will likely affect your credit but in different ways.

Option 1: Sell the House

If you and your ex-spouse agree to sell the home, you can use the proceeds from the sale to pay off the joint mortgage and then go your separate ways. In this situation, by paying off the mortgage early, you cut out the risk of either party missing mortgage payments down the road and damaging your credit.

Some states have community property laws that may necessitate selling the house in order to split up everything you and your spouse owned together unless both of you can reach an agreement on how to divvy things up.

The downside of selling the house is that now both of you will have to find somewhere else to live, and buying another house when you’re divorced can be a challenge, as we will elaborate on below.

Depending on how the housing market is doing when you get divorced, it’s possible that you could end up owing more on the mortgage than the house is currently worth. In this case, your bank might agree to a short sale, where you sell the house for an amount that is less than what you owe toward your mortgage.

Often, the simplest solution for dealing with a joint mortgage after a divorce is selling the house and using the proceeds to pay off the mortgage.

Unfortunately, a short sale is considered a settlement, which means it is a major derogatory item on your credit report, so a short sale should be your last resort if the goal is to preserve your credit.

Of course, selling the house is not always possible, as one spouse may want or need to stay in the home, which brings us to the next possibility for dealing with your joint mortgage.

Option 2: Refinance the Mortgage in One Spouse’s Name

If someone needs to remain in the home, then the joint mortgage will have to be refinanced in one person’s name. This requires that one party has enough income and an adequate credit score to qualify for a mortgage on their own.

If your credit is not quite where it needs to be to refinance the mortgage in your name alone, you could try to boost your credit score with some quick fixes such as decreasing your credit utilization or increasing your credit limit. Then you can request a rapid rescore from your mortgage lender to see an immediate increase in your score.

Ideally, the person who will continue to live in the home would be the one refinancing the mortgage in their name. This removes the liability from the spouse who is no longer living in the home, meaning that if the new sole mortgage owner fails to make on-time payments, the other person’s credit will not be punished for it.

However, this is not always the case. When the opposite is true, i.e. the spouse not living in the home becomes responsible for the mortgage, there can be problems. For example, if you are the one staying in your home and your spouse is supposed to pay the mortgage, but instead, they default on the loan, you could be at risk of your house being foreclosed by the bank, even though you weren’t at fault for the missed payments.

Option 3: Buy Out Your Spouse and Keep the Home

In some states, the equity of a shared home is split between the two parties in the event of a divorce.

If this is the case for you and you want to keep the house, you can try to raise enough cash to buy out your spouse’s portion of the equity in the home.

To raise funds, you could apply for a home equity loan, which is essentially a second mortgage. Alternatively, you could take out a personal loan. Of course, getting approved for a personal loan will be dependent on your credit and income, since it does not use your home as collateral.

Option 4: Keep the House and the Existing Mortgage

Keeping the joint mortgage and continuing to live in the home with your ex-spouse may not be ideal, but it could save you some money.

In some situations, it may be most practical or even necessary to continue cohabitating with your ex-spouse and keep the mortgage as-is. Although this arrangement is obviously not ideal, it could give both parties some extra time to get their credit in shape to either refinance the mortgage or sell the home and buy a new home.

Buying a New Home When You’re Divorced

In going through a divorce, there’s a good chance you’ll have to move out of your house and find a new home. Unfortunately, according to Forbes, if you have recently gotten divorced or are currently undergoing divorce proceedings, this can affect your chances of qualifying for a mortgage.

Since one of the important factors that mortgage underwriters look at is your debt-to-income ratio, it can be difficult to get approved for a mortgage on a second house when you’re still paying off another mortgage.

Therefore, if your ex-spouse cannot refinance the mortgage in their own name, then you may have to wait until you sell the home that you shared with your ex-spouse before trying to get a loan to buy a new place.

How to Rebuild Credit After Divorce

If your credit has taken a beating as a result of your divorce, the good news is that there are steps you can take to repair your bad credit.

Pay all of your bills on time to help rebuild a positive credit history, increase your credit age, and outweigh any derogatories that you may have gotten.

Consider getting a secured credit card or a credit-builder loan to establish primary accounts in your name.

Get added as an authorized user to a seasoned tradeline. This can add years of credit age and perfect payment history to your credit report.

Options for rebuilding credit include applying for a credit-builder loan, getting a secured credit card, and being added as an authorized user to a seasoned tradeline.

Conclusions on How Getting Married or Divorced Can Affect Your Credit

By now, you know that the myth that you and your spouse merge credit reports when you get married is not true and that neither getting married nor getting divorced have a direct impact on your credit. However, there are a multitude of ways in which your marital status can indirectly affect your credit.

Firstly, getting engaged and planning a wedding may often mean going into debt in order to pay for the rings, the wedding ceremony and reception, and the honeymoon. This can affect your credit utilization ratio, and if having all that debt leaves you overextended, then you could end up missing payments and getting some derogatory items on your credit report.

Once you are married, your credit will be affected by any joint accounts you and your spouse open together, such as a mortgage. It’s important to be on the same page as your spouse when it comes to managing joint accounts in order to reduce the risk of your credit being damaged by your spouse’s mistakes (and vice versa).

It is true that many people struggle with their credit after getting a divorce, not because of their divorced status per se, but because legally separating from your spouse is expensive, and it creates complications for your joint credit accounts that can be difficult to resolve.

However, you don’t have to let a divorce ruin your credit. Try to come to an agreement with your ex-spouse about how to split up financial responsibilities. If your credit does take a hit during your divorce proceedings, you can rebuild your credit by becoming an authorized user and opening up new primary accounts in your name.

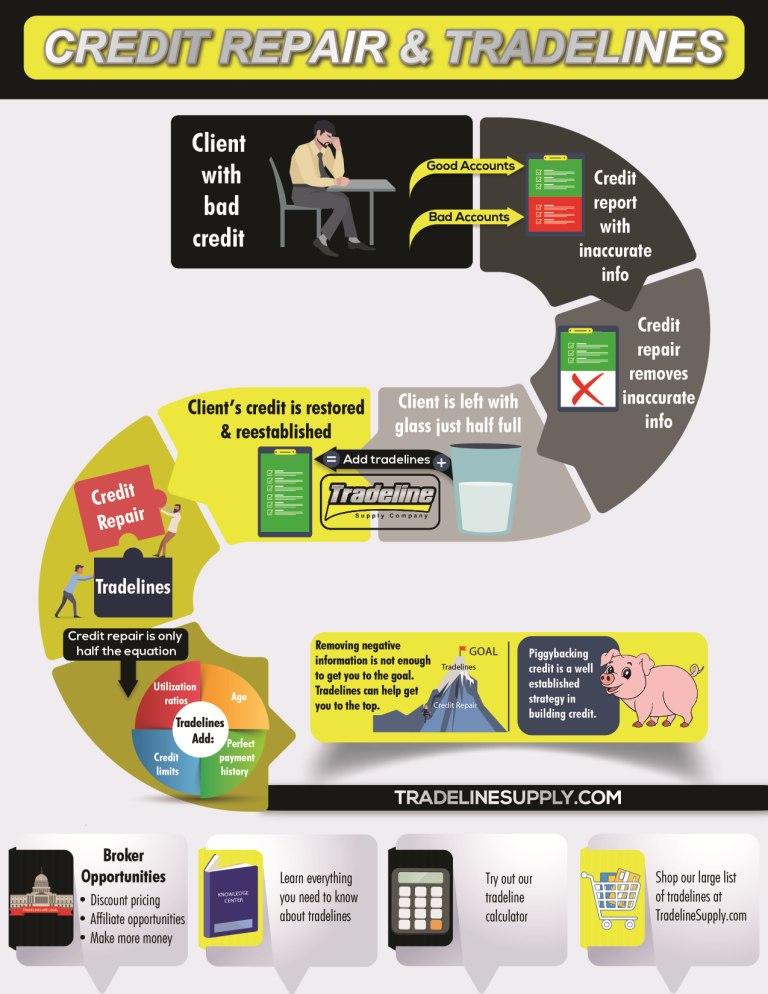

Perhaps the title “Credit Repair vs Tradelines” is not entirely accurate, but this is a common way that many consumers think of the two industries and even many credit repair companies as well. In truth, as our infographic illustrates, the two services really go hand-in-hand.

However, there are several differences that we will highlight in order to understand the full range of credit-related options. Be sure to check out our article below the infographic for all the details.

What Is Credit Repair?

The term “credit repair” can have different definitions depending on who you ask. Generally, however, credit repair is considered to be the process of mending poor credit that is a result of errors in your credit report or identity theft. This is accomplished by disputing inaccurate information in your credit file with the credit bureaus, who will investigate the claim and take appropriate action.

For example, if you have collections on your credit report that are being reported with inaccurate information, you can dispute the collection account and have it updated or removed from your credit report.

Sometimes people also use the term credit repair to mean fixing bad credit in general, using traditional methods such as bringing all accounts current and paying down debts.

For those who are seeking credit repair services through a company, you are probably interested in the process of repairing bad credit by disputing inaccurate negative information in your credit file. If your credit score is lower than the average range, going to a credit repair business may seem like an appealing option.

However, keep in mind that credit repair has its limitations. Since credit repair services focus on removing information from your credit file, once that is accomplished, there may not be much left in your file to show that you have a credit history at all. This is especially true of questionable credit repair companies who use dishonest methods to aggressively “sweep” your credit file of legitimate information.

In order to truly improve your credit score, it is important not only to remove inaccurate negative information but to also work on rebuilding your credit.

Credit repair focuses on removing inaccurate information from your credit report.

Tradelines vs. Credit Repair: What’s the Difference?

Addition and Subtraction

As we discussed above, credit repair can be thought of as the process of removing negative information from your credit report. In contrast, tradelines add information to your credit report.

A tradeline is simply any account in your credit file, so adding tradelines by definition bulks up your file. This can be helpful for people with short or thin credit histories, or those who are recovering from a period of bad credit and trying to rebuild their credit.

A short credit history means the age of your credit file is not very long, while a thin credit history means you have only a few accounts in your credit profile, if any. Credit scoring models factor in both the length of your credit history and your mix of credit, so having a thin or short credit file will likely result in a lower credit score rating.

Being added as an authorized user to tradelines that are in good standing and have a higher age (known as “seasoned” tradelines) could improve both of these factors by increasing your length of credit history and diversifying your mix of accounts.

In addition, seasoned tradelines for sale from a reputable company will have perfect payment histories and relatively low utilization ratios, which impact important components of your credit.

Tradelines can post to your report quickly, while the credit repair process may take longer.

How Long Does Credit Repair Take to See Results?

The credit repair process typically takes 1-6 months or longer, depending on how many disputes you need to make. Once you submit your disputes to the credit bureaus, they have 30 days to research the dispute and 5 more days to respond once they have completed the investigation. Sometimes, additional information may be needed, which can add more time to the process.

If you have a lot of errors to dispute, you may have to submit them a few at a time, which is why getting results can take several months.

Tradelines, however, can post to your credit report in as few as 11 days, and sometimes even faster. It just depends on the reporting period of the tradeline you are adding.

How Much Does Credit Repair Cost?

The cost of credit repair services can vary widely depending on the company, which services you need, and how long the process takes. Many credit repair organizations charge a monthly fee for their work in addition to an initial fee for pulling your credit reports. Typically, the monthly fees range between $60 to about $100 per month for basic credit repair services. [Disclosure: This article contains affiliate links.]

Purchasing tradelines, on the other hand, usually involves paying a one-time fee (unless you choose to extend the tradeline for additional time).

Is Credit Repair Worth It?

If you have bad credit, paying for a credit repair service is an option that you may want to consider, especially if you have a lot of errors on your credit report or if you have been the victim of identity theft and you need some help disputing fraudulent accounts.

If you do decide to hire a credit repair service to help you clean up your credit, make sure you research each company thoroughly and choose a legit credit repair company. Unfortunately, the industry has not earned the best reputation. Be sure to know your rights laid out by the Credit Repair Organizations Act (CROA) so you can protect yourself from being taken advantage of by shady credit repair companies.

Not everyone needs the help of a credit repair company to begin with. If you have one or two simple errors on your credit report, you may feel that you will be able to go through the credit repair process on your own and have those errors successfully removed or updated.

To answer the question of whether paying for credit repair is worth it, you’ll have to take a look at your credit report and decide whether the damage is extensive enough to warrant hiring a professional credit repair service or whether you want to try DIY credit repair.

How Credit Repair and Tradelines Work Together to Fix Your Credit

Credit repair and tradelines naturally go hand-in-hand. In one sense, tradelines pick up right where credit repair ends. Again, credit repair helps to “clean up” credit and tradelines help build or re-establish positive credit history.

One really should not exist without the other; the two techniques are most effective if done in tandem. Since credit repair removes information from your credit file, it may be necessary to add positive information to your file in the form of tradelines in order to truly rebuild your credit.

Tradelines can help to build or rebuild credit.

Buy Tradelines or Fix My Credit: Which Should I Do First?

It does not necessarily matter which one comes first. Both can exist at the same time.

However, if you have bad credit due to inaccurate derogatory information on your credit report, those variables will have an impact on your overall credit picture and could lead to tradelines having a diminished effect. In this case, the most effective course of action would be to repair your credit before adding tradelines.

On the other hand, it is never a bad time to have good things on your credit report. The timing of which strategy should come first ultimately depends on your individual situation and your own timeline.

For example, some credit repair programs take quite some time to accomplish. As we mentioned, is not uncommon for certain credit repair programs to take many months to complete. In these cases, tradelines may fit in at any given time during the credit repair process.

Credit repair and tradelines work best when used together as part of your overall credit strategy.

Why Don’t All Credit Repair Companies Offer Tradelines?

Surprisingly, not all credit repair companies sell tradelines or even know about tradelines. Sometimes tradeline companies are seen as competition to credit repair businesses because clients may end up spending money on tradelines as opposed to credit repair services.

However, as we have seen, credit repair works best when paired with tradelines. The best credit repair companies will provide you with all of the information and options that you need to make an informed decision about your financial future.

Conclusion

While tradelines and credit repair can both be effective in improving your credit, they are not the same thing. Rather, they are complementary strategies that work best when used together.

Don’t mistake tradelines for credit repair—think of tradelines as a way to build or re-establish credit. The best course of action for your credit is to evaluate your own unique situation and ask how tradelines can complement your credit repair strategy.

If you’ve been paying attention to the world of credit, you’ve probably heard a lot about credit freezes lately. A credit freeze can be a valuable tool for those who may be concerned about identity theft. However, many people are unaware of how credit freezes works and how to use them.

What is a credit freeze and how does it work? How do you place a freeze on your credit report? Is a credit freeze worth it? Keep reading for the answers to these questions and more.

What Does a Credit Freeze Do?

What a credit freeze does is it blocks lenders and business from accessing your credit file without your consent. This helps to prevent identity theft in the case of a criminal trying to open a fraudulent credit account in your name.

However, a credit freeze does not block access for all businesses; rather, it only pertains to companies with which you do not have an existing relationship. Lenders that you currently have a relationship with can still access your credit file, such as your credit card issuers, your auto lender, etc.

In addition, if you have an account in collections and your lender hires a collection agency, the collection agency can also view your credit report.

A credit freeze also does not prevent you from accessing your own credit report, including your free annual credit report from each credit reporting agency.

Who Should Do a Credit Freeze?

If you receive any bills that are in your name but do not belong to you, that is a sign of possible fraudulent activity.

You may want to consider freezing your credit if you have been a victim of identity theft or suspect you may be a victim of identity theft.

Here are some signs of potentially fraudulent activity in your name that Experian says to watch out for:

You have received bills in your name or letters from debt collectors for accounts that are not yours.

There are inquiries on your credit report from businesses to which you did not give your permission to pull your credit report.

You get a notice from a company that warning you that you have been affected by a data breach.

You get an alert from your bank about fraudulent activity on your account.

If any of these situations apply to you, you may have an elevated risk of becoming a victim of identity theft, which means it may be a good idea to freeze your credit.

How Does a Credit Freeze Work?

You will need to provide your PIN when you want to lift a credit freeze.

The way that credit freezes work is governed by federal law. Each of the major credit bureaus is required to provide credit freezes to consumers within a certain time frame.

If you request a security freeze online or over the phone, the law mandates that the freeze must be put in place by the next business day. When you want to lift the freeze to apply for credit, the credit bureaus must “thaw” your credit report within an hour of your request.

If you send your request to place or lift a freeze in the mail, the credit reporting agencies have up to three days after they receive your request to take the appropriate action.

When you place a credit freeze, the credit bureaus will provide you with a PIN or password. You will need this PIN or password to lift the freeze, so it’s important to store it securely. When you want to remove the freeze temporarily or permanently, you can contact the credit bureaus and provide your PIN or password and they will lift the freeze.

When it comes time to lift a freeze temporarily to apply for credit or employment, it’s worth asking which credit bureau the lender or employer is planning to pull your report from, so that you only have to lift the freeze with that specific bureau. If you are not sure which bureau they will use, you will need to contact each bureau to lift all of the freezes on your reports.

A security freeze on your credit will not prevent fraudulent activity on accounts that were compromised prior to the freeze.

Will a Credit Freeze Prevent Identity Theft?

A credit freeze can certainly help reduce the risk of identity theft by preventing scammers from opening new credit accounts in your name.

However, a credit freeze will not protect you against identity theft in cases where someone has already accessed your financial information, such as if your bank account password was stolen by a hacker or exposed in a data breach.

It’s always a good idea to check your credit reports regularly to watch out for fraudulent activity, whether you have a freeze on your credit file or not. If you are concerned about identity theft, placing a security freeze on your credit may give you some additional peace of mind.

Since credit freezes are guaranteed by federal law, if someone were to open a fraudulent account in your name while your credit is frozen, you would not be held liable for the financial losses incurred.

How Long Is a Credit Freeze in Effect?

The length of time that a credit freeze stays in effect varies depending on which state you live in.

In most states, credit freezes are in place permanently until the consumer decides to lift them, whether temporarily or permanently. However, some states set automatic expiration dates for security freezes a number of years after they were originally placed.

Is a Credit Freeze Permanent In Your State?

In Kentucky, Nebraska, and Pennsylvania, credit security freezes automatically expire 7 years from the date of placement. In all other states, they are permanent until removed by the consumer.

If you want to learn more about credit freeze regulations in your state, creditcards.com has a useful resource that summarizes the laws in all 50 states.

It is completely free to place a freeze on each of your credit reports. In addition, it is also free to temporarily lift the freeze and then reinstate it, which is important to do when applying for credit or buying tradelines, as we will discuss below.

How to Do a Credit Freeze

To place a security freeze on your credit file, you will need to contact each credit bureau (Equifax, Experian, TransUnion, and Innovis) and be ready to provide personal information such as your name, address, date of birth, and social security number.

Unfortunately, since the credit reporting agencies are all separate private companies, there is no integrated system in place where you can request a freeze once and have it apply to all of your credit reports. Instead, you have to work with each of the credit bureaus individually in order to place or lift a credit freeze.

Can I Place a Credit Freeze Online?

In many cases, it is possible to initiate a credit freeze online by visiting each credit bureau’s website and filling out a form. In some cases, they may ask you to send documentation verifying your identity via mail before issuing the freeze.

Some experts recommend freezing your child’s credit to prevent identity theft.

Freezing Your Child’s Credit

Given the proliferation of synthetic identity fraud using stolen SSNs, which we talked about in our article about CPNs, many credit experts recommend freezing your child’s credit to protect them from identity theft. You don’t want to wait until your child is an adult and ready to apply for credit to find out that their credit has been ruined by a criminal that stole their identity years ago.

If you have children under the age of 16, federal law allows you to freeze their credit. Although most children do not have credit files yet, when you request a credit freeze, the bureaus will create a credit file for your child and then freeze it.

When you freeze your child’s credit report, just like when you freeze your own credit file, remember that you will need to keep the PIN in a secure place and you should be prepared to “thaw” their file when the time comes for them to apply for credit.

What’s the Difference Between a Credit Freeze, a Credit Lock, and a Fraud Alert?

While they sound similar and are often confused, a credit freeze, a credit lock, and a fraud alert are all different things.

Fraud Alerts

A fraud alert is an alert placed on your credit report that lets potential lenders know that you may have been a victim of fraud.

It is similar to a credit freeze, but instead of simply preventing lenders from seeing your credit report, it allows them to obtain a copy if they take extra steps to verify your identity and that you are the person applying for credit, such as calling you on the phone.

Like a credit freeze, a fraud alert may help to prevent fraudulent accounts being opened in your name, but cannot stop someone who already has access to your accounts.

Unlike a credit freeze, fraud alerts are temporary. A normal fraud alert for someone who has not been the victim of identity theft lasts for one year. Victims of identity theft can get an extended fraud alert, which lasts for seven years. Those serving in the military can use an active duty military alert, which lasts one year and is renewable as long as you are deployed.

Credit locks are not governed by federal law and may come with monthly fees.

Fraud alerts are free. Conveniently, when you request a fraud alert, you only have to contact one credit bureau. That bureau must then contact the other two major bureaus and all three of them will implement a fraud alert on your respective credit reports.

Credit Locks

A credit lock is also similar to a credit freeze, but it does have some important distinctions. One of the main ways in which a credit lock differs from a credit freeze is that it is more convenient to unlock your credit than it is to lift a credit freeze.

While lifting a credit freeze requires you to provide the PIN that you were given when you placed the freeze, a credit lock can be undone in seconds and without a PIN online or using an app on your phone.

Credit locks are not covered by the federal law that regulates credit freezes and fraud alerts, so the credit bureaus are allowed to charge fees for providing credit locks. Consequently, placing a lock on your credit often comes with monthly fees.

In addition, a credit lock is simply a business arrangement between you and the credit bureaus and is not regulated by federal law. Therefore, the credit bureaus can’t necessarily be held responsible if someone does manage to fraudulently open an account in your name while you have a credit lock in place.

Some credit locks may come with forced arbitration agreements in the contract, meaning that if you have a dispute with the credit bureau, it must be resolved by arbitration instead of taking them to court.

Will a Credit Freeze Prevent My Tradelines from Posting?

In order for your tradelines to post correctly, all credit freezes, fraud alerts, and credit locks must be lifted.

The reason for this is simply that the purpose of a credit freeze is to block anyone from accessing your credit file. This, of course, includes the banks that you may buy tradelines from.

Therefore, if you have a credit freeze placed on your file, there is a good chance that it will prevent the tradelines from posting to your credit report.

The same goes for fraud alerts and credit blocks, which also restrict access to your credit file and thus prevent tradelines from posting.

For this reason, our non-posting guarantee requires that you lift all credit freezes, credit locks, and fraud alerts before placing a tradeline order with us.

A credit freeze is a tool that allows you to prevent others from accessing your credit report, which makes it harder for criminals to open fraudulent accounts in your name and thus helps to protect you from identity theft.

Placing a security freeze on your credit report is free and it does not affect your credit score, so it may be a good idea, particularly for consumers who are concerned about identity theft.

Unfortunately, the credit bureaus and banks have left themselves vulnerable to cyberattacks, and it has become commonplace for hackers to gain access to and expose the personal information of millions of consumers at a time. Therefore, virtually all savvy consumers are likely to be concerned about protecting their identity and sensitive financial information.

However, there are some things to keep in mind when considering placing a security freeze on your credit file.

Firstly, it is important to remember that you must lift a credit freeze before applying for credit. If you don’t, since the credit freeze will block the lender from accessing your file, your application could be delayed or denied altogether. You’ll need to carefully keep track of the information required to lift your credit freezes, such as a PIN or password.

Because of the hassle of unfreezing and refreezing your credit report, you might want to postpone placing a freeze on your credit if you are about to apply for a mortgage, an auto loan, or another type of new credit.

In addition, if you are planning to purchase authorized user tradelines, it is vital to remove all credit freezes, fraud alerts, and credit locks of any kind before buying tradelines, or else they will prevent your tradelines from being added to your credit report.

To summarize, a credit freeze can be a highly valuable tool in protecting your credit health—just be sure to remove any security freezes on your credit report before applying for credit or buying tradelines.

Now that you are familiar with the ins and outs of how credit freezes work, let us know what you think. Do you plan to get a credit freeze? Do you have a credit freeze in place already? Share your thoughts below!

When consumers ask me questions about their credit reports it’s normally about how to get an item removed or corrected. Sometimes, however, I do get questions about having information added to a credit report. This type of question brings up an interesting concept, which is whether or not consumers have the right to certain credit report information or even the right to a credit report at all.

The Fair Credit Reporting Act

The Federal statute that governs the credit reporting agency’s actions, the use of credit reports, and the furnishing of information to the credit reporting agencies is the Fair Credit Reporting Act or “FCRA.” The FCRA is a consumer protection statute that has been around since the early 1970s and confers rights to consumers as it pertains to their credit reports. The Act has been amended dozens of times.

There is no language in the FCRA that affirmatively gives consumers the right to have a credit report. And, there’s also no language in the FCRA that gives consumers the right to demand that they do not have a credit report. The act is silent on those two issues.

The Voluntary System

What this means is you cannot demand that a credit reporting agency push a button, delete your credit report information, and then never again collect information about your credit obligations. Conversely, you also cannot force a credit reporting agency to reach out to your bank or other service providers, get information about how you manage your accounts, and then add them to your credit reports.

Your credit scores might not be the same.

There are some very limited scenarios with federally guaranteed student loans and their servicers. The loan servicers may be required by the Department of Education to credit report debtor obligations, but that’s not the same as a lender choosing to report, or not to report. That’s entirely voluntary.

From a more granular perspective, you also don’t have the right to identical credit reports and certainly, you don’t have the right to identical credit scores across the credit reporting agencies and the various brands of credit scores. So, you cannot demand that your credit reports at Equifax, Experian, and TransUnion be the same and you cannot demand that your FICO and VantageScore credit scores are identical.

In fact, you don’t even have the right to a credit score, at all. There are certain minimum criteria that must be met before your credit report will even qualify for a credit score. When your credit report is created, a process that normally occurs the first time you apply for credit, it will not qualify for a credit score because there isn’t enough information to make it scorable.

Consistency, or Inconsistency

Another interesting aspect of credit reporting and our control (or lack of control) over what goes on and what does not go on our credit reports is the issue of consistency. For example, I can be added as an authorized user on Credit Card A and also added as an authorized user on Credit Card B, and there’s no guarantee that both card issuers will choose to report the account on my credit reports.

There’s also no guarantee that the issuer of Credit Card A will credit report all of their authorized users. They may choose to report some of them, and then choose to not report the rest. There’s nothing I can do about this. There’s nobody to complain to about the consistency issues and you can’t leverage your rights to consistency, because you don’t have any.

You also cannot control whether or not any of your lenders report to all three of the credit bureaus. For example, you may have a lender that reports to Equifax, but not to Experian and TransUnion. You can come up with any number of other combinations, and those would be true as well.

Not all credit card issuers report authorized user data to the credit bureaus.

This can be an issue with the use of secured credit cards, which are a common tool used by consumers to build or rebuild their credit. Notwithstanding the fact that becoming an authorized user on a loved one’s credit card is a much better alternative, there’s no guarantee that your secured card issuer will report to any of the credit bureaus.

Users of Credit Reports

There’s one final issue to cover on this topic of consistency. The users of credit reports, as in lenders and debt collectors, also don’t have the right to use credit reports or to furnish information to any of the credit bureaus. All users of credit reports had to apply for service with the credit bureaus and then go through a process of consideration and evaluation by the credit bureaus before their accounts were approved.

And even if a company has an account with the credit bureaus, buys credit reports, and furnishes information to the credit bureaus there’s no guarantee that they will always have that account. The credit bureaus can choose to stop doing business with a lender or a debt collector. They can also choose to purge data provided by a former client. And like consumers, there’s nothing they can do to force a credit bureau to change their mind.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company, LLC.

Q. I am planning to apply for a new apartment soon and my credit score is 678 from Equifax and 608 from Transunion. What do most rental companies require to get approved? This is a low-income property.

I also want to get a new credit card for someone with low income and no annual fee. Are there any credit cards that will give me a card with my current credit scores? Also, should I wait to get a credit card after the apartment complex does their credit check or should I get a credit card first?

Dear Reader,

Each rental company will look at your credit report differently. Ultimately, they want to know if they can trust you to pay them on time every month. Because your credit score is considered fair, you may end up needing to have a bigger deposit to secure an apartment.

Having only fair credit can make it difficult to get a credit card with a decent interest rate. However, you can look for a secure credit card. These cards work like regular cards, but they are secured by a deposit you make. Secured cards provide a great way for people with no credit or with a low score the opportunity to improve their scores and their credibility.

Be sure to do your homework and compare several secured credit cards. Look for one that meets your needs–in this case, one that does not have an annual fee. Another option for improving your credit would be to check out Experian Boost. It uses your phone and utility bill payments to “boost” your score if you have been paying those regularly and on-time.

Now, whether you should wait to get your card after the apartment company reviews your credit, I think you should. Whenever you ask for new credit, even for a secured credit card, a hard inquiry is generated on your report, and it lowers your credit score. So, it’s best to have the highest possible score to get your apartment.

After that, apply for the card and use it strategically, always paying on time and only using up to 30% of your available credit or less. If you need additional guidance, feel free to contact an NFCC-certified credit counselor from a local nonprofit near you. They are ready to help and can provide more personalized recommendations for improving your credit. Good luck!

Sincerely,

Bruce McClary, Vice President of Communications

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your credit report and damage your credit scores for several years. Fortunately, there are some things you can do to avoid getting derogatory marks as well as reduce the damage if you do end up with a negative item on your credit.

We’ll help you understand minor and major derogatories, how derogatory items affect your credit score, and what you can do about them.

What Is a Derogatory Credit Item?

The word derogatory simply means negative, so a derogatory credit item is a negative item on your credit report.

Derogatory items hurt your credit score and can impact your chances of getting approved for credit.

There are two types of derogatory items: minor derogatories and major derogatories.

Minor Derogatory Items

A minor derogatory is a payment that was past due, either 30 days late or 60 days late. If, after the 30- or 6-day late, you brought the account current again, then it is considered a minor derogatory mark. However, if you are currently 30 to 60 days late, it is considered a major derogatory, which we will discuss below.

30 Days Past Due

Lenders cannot report your account as late to the credit bureaus until 30 days have elapsed since the missed due date, so if you pay your bill anywhere between one to 29 days after the due date, you should not see a derogatory item reflected on your credit report.

However, your lender may charge a late fee, so it’s still best to pay all of your bills on time. If you’ve never been late on the account before, you can contact your lender and see if they can waive the late fee for the accidental late payment. Many lenders are willing to do this for account holders that otherwise have good records.

In addition, if you have a promotional interest rate, you will most likely forfeit the promotional rate if you miss a payment, even if you were only a few days late.

A 60-day late payment could result in an interest hike from your credit card issuer.

60 Days Past Due

If you miss your due date twice in a row and become 60 days late, the situation becomes more serious. At this point, the credit card issuer can hit you with a penalty APR of up to 29.99%.

Not only will this high interest rate apply to all your purchases for at least the next six billing cycles, but in this case, the bank is also allowed to apply the penalty rate to your existing balance as well. Not all credit cards have penalty APRs, however, so check the terms of your card to see if you could be subject to one.

Thankfully, “universal default” is a thing of the past—the practice of credit card companies raising consumer’s interest rates if they were late on any loan with any lender was banned by the Credit Card Act of 2009.

However, the exception is if you have multiple cards with the same bank. In this case, if you miss a payment on one of the cards, the bank is allowed to raise your rates on all of the cards you have with them.

Major Derogatory Items

A court judgment against you is a major derogatory.

A major derogatory credit item is typically defined as an account that is 90 days past due or more. If you have a major derogatory on your credit report, that is a huge red flag to lenders, and it may hinder you from being able to qualify for credit.

Examples of major derogatory credit items include:

Charge-offs – This is when a creditor writes off your account as a loss because you are so delinquent on the debt that they assume that the debt is unlikely to be paid. This typically happens after six months have passed without payment. Collections – After your account has been charged off by the lender, they may try to regain a portion of their losses by selling the account at a discount to a debt collector, who then becomes the owner of the debt and will try to collect the funds from you.

Court judgments – A judgment is when a lender or debt collector sues you over an unpaid debt and the court orders you to repay it. A court judgment gives the lender or debt collector more powerful options to collect the money you owe them, such as garnishing your wages or putting a lien on your home.

Foreclosures – This happens when you become so delinquent on your home loan that the bank takes possession of the home so that they can try to recover the balance of the loan by selling the property.

Settlements and short sales – A settlement is an agreement between you and your lender that you will pay back part of the debt you owe them. The lender will then stop trying to collect more money from you after you have paid the settlement amount, but since you did not pay the full amount you owed, it is a derogatory item. A short sale is considered to be a type of settlement since the lender is agreeing to sell the property for less than the mortgage balance you owe.

Bankruptcy is the most serious derogatory credit item.

Repossessions – This is when the lender takes back possession of something such as your car or your house because you defaulted on the payments.

Public records – Public records such as delinquent taxes, liens, unpaid alimony, and unpaid child support, are derogatory items that can be severely damaging to your credit, especially if there is still a balance owed.

Bankruptcy – Filing bankruptcy means you are asking to be legally released from paying back some or all of your debts. Because of this, and because it affects several credit accounts, not just one, it is the most damaging derogatory item. It will almost certainly devastate your credit score and reduce your chances of getting approved for credit for a significant amount of time, although it is possible to recover from bankruptcy eventually.

How Do Derogatories Affect Your Credit Score?

As you may have guessed, any derogatory mark on your credit report can seriously damage your credit score. However, they do not affect everyone equally. There is no predetermined amount of points that is associated with any given credit action.

“There is no fixed value to any derogatory entry. Their value is always relative to the presence or absence of other similar derogatory entries on a credit report. So, the answer to the question ‘how much?’ varies from ‘not at all’ to ‘a whole lot’ — and everything in between.”

In other words, the effect of a derogatory item could range from a significant drop in your credit score to potentially no difference in your credit score at all. It is going to depend on 1) what else is already in your credit file and 2) the severity of the derogatory information.

For those who have pristine credit records, even one 30-day late payment can do some serious damage to their credit scores. On the other hand, if you already have some delinquencies on your report, additional delinquencies won’t have as great of an impact.

Derogatory items will also have a larger impact on those with thin or short credit files, meaning they do not have very much positive credit history to help soften the blow of a negative mark. In contrast, those with a thicker file or longer credit history will have more positive history in their file to help balance out any negative events.

Credit scorecards, or “buckets,” can affect the impact of a derogatory item on your credit score.

Another complication is the concept of credit scoring scorecards or “buckets,” which score groups of consumers differently based on certain characteristics of their credit profile.

As a hypothetical example, there could be a scorecard for consumers with no major derogatories and a scorecard for consumers with one major derogatory. In this case, getting your first major derogatory mark could put you into a different scorecard, wherein your score would be calculated in an entirely different way than it was before.

While the impact of a derogatory item is going to vary from person to person depending on their unique individual credit history, one thing we do know for sure is that derogatory items become less impactful to your credit as time passes.

In fact, it is still possible to have good credit with a derogatory mark on your credit report if it is an old item and you have balanced it out with positive credit history since then.

How Late Payments Affect Your Credit Score

In terms of how bad late payments are for your credit, it’s not so bad to miss a payment on one account for one or two months, according to an article on The Balance. However, missing payments on several different accounts for one to two months will be worse for your credit. And finally, missing even one payment for three months in a row will be equally as harmful as a charge-off or collection since they are all major derogatory items.

The Impact of a Derogatory Item May Depend on the Credit Scoring Model

When it comes to collection accounts, for example, collections that have been paid off and small-balance collections have different impacts depending on which credit score is used.

FICO 8, the most widely used credit score, considers both paid and unpaid collections to be major derogatories. That’s one reason why paying off a collection account may not always increase your credit score.

FICO 9 and VantageScore 3.0 and 4.0 disregard collection accounts altogether once they have been paid. In addition, these three scoring models assign less weight to medical collections. FICO 8 and FICO 9 ignore collections that had an original balance of less than $100.

Paying the past-due balance does not make the derogatory mark disappear, but it is usually still a good idea.

Does Paying the Past-Due Balance Delete the Derogatory Mark?

Unfortunately, simply bringing the account current by paying the past-due balance does not make the derogatory mark disappear. It does not negate the fact that you were late paying your bill, which is important information that helps determine your credit score and helps lenders decide whether they want to do business with you.

Payment history is the most important part of both your FICO score and your VantageScore for a reason. It is highly predictive of how much of a credit risk you represent to lenders. For that reason, accurate derogatory information must stay on your credit report even after you have caught up on payments.

However, can still be beneficial to pay off the derogatory items on your credit report. Experian says, “While paying off a derogatory account won’t automatically remove it from your credit history, it will be updated to show it has been paid, and lenders may view a paid derogatory more favorably than an unpaid one.”

How to Minimize the Credit Score Impact of a Derogatory Item

Although bringing an account current will not remove the negative information from your credit report, it is still a good idea. Having made a late payment in the past and then catching up is better for your score than currently being late.

Moving forward, do your best to make sure you’re not late again.

Maintaining a positive credit history from now on is the most important thing you can do to minimize the effect of a derogatory item and restore your credit back to health.

Once you have done all you can to mitigate the damage of a derogatory item, then it simply becomes a matter of waiting until the negative mark ages off your credit report.

How Long Can Derogatory Credit Items Stay on Your Credit Report?

In general, derogatory marks can be reported for up to seven years after the account was first reported as late, which is referred to as the date of first delinquency (DOFD).

If you get a court judgment against you, however, that will remain on your credit report for seven years after the judgment was issued, not seven years from the date you were first late on the original debt.

Certain types of accounts can stay on your credit report even longer. Depending on the type of bankruptcy, for example, bankruptcy may stay on your credit report for up to 10 years.

According to Experian, since a Chapter 13 bankruptcy requires you to pay some of the debts you owe, this type of bankruptcy is removed from your credit report after seven years. With a Chapter 7 bankruptcy, you don’t pay back any of the debt, so it is removed 19 years after the date of filing instead of seven years. The individual accounts associated with the bankruptcy will still disappear seven years after the DOFD for each account; filing for bankruptcy does not affect the seven-year timeline.

Dispute derogatory items on your credit report that are inaccurate via mail.

Besides a Chapter 7 bankruptcy, all other delinquencies are required by law to be deleted from your credit report after seven years. However, the impact of a derogatory mark on your credit score will decrease over time, especially if you maintain a positive credit history going forward that can help outweigh the negative items.

Removing Derogatory Credit Items From Your Credit Report

If you have inaccurate negative items on your credit report, it’s in your best interest to dispute the derogatory items on your credit report as soon as possible.

Your credit reports should have instructions on how to dispute derogatory credit items that have been put on your credit report in error. The best way to dispute inaccurate negative information is to send a separate letter for each dispute via certified mail, along with any accompanying evidence that is needed to verify the validity of your claim.

Make sure to dispute the derogatory items on your credit report with the credit bureaus as well as with the creditor that is furnishing the data.

Should You Write a Letter Explaining Derogatory Items on Your Credit Report?

You may need to write a letter explaining derogatory items on your credit report when applying for a mortgage.

A letter of explanation is a letter that you write to a lender explaining the reason for negative marks on your credit report. This may be required by your lender when you apply for a mortgage, particularly when applying for a home loan that is subsidized by the government, such as an FHA loan or VA loan.

Your mortgage lender needs to be certain that you will be able to pay off your home loan. They will want to understand the circumstances of any derogatory items on your credit report in order to determine whether you have learned from your mistakes and taken steps to improve your situation or whether you may still be at risk of defaulting on a loan in the future.

A good letter of explanation should be truthful, clear, and detailed. If there were extenuating circumstances that led to you becoming behind on your bills, explain what happened and how you resolved the problem. As with a credit report dispute, be sure to include any documentation that supports your story along with your letter of explanation. Try looking up sample letters of explanation online if you need help.

How to Avoid Getting Derogatory Marks on Your Credit Report

Since accurate and timely derogatory information can’t legitimately be removed from your credit report, the best strategy is to prevent them from happening in the first place.

If you accidentally miss a payment, call your creditor right away to see if they can waive your late fee.

Here are some tips to help you keep your credit in the clear.

To ensure you never miss a payment, set up automatic payments for all your loans and credit cards.

As an additional precaution, also set up notifications that alert you when your statement is available and when your due date is coming up so that you can keep an eye on your accounts and make sure that the payments are going through. Knowing exactly when your bill is due and how much you need to pay will also allow you to make sure that you have sufficient funds in your bank account to make the required payments.

If you are in a period of financial hardship and can’t afford to make the minimum payment, contact your creditor and try to work out an arrangement with them to temporarily reduce or defer payments.