The NFCC often receives readers questions asking us what they should do in their money situation. We pick some to share that others could be asking themselves and hope to help many in sharing these answers. If you have a question, please submit it on our Ask an Expert page here.

This week’s question: I took on too much debt and went without a job for 23 months. I am now employed and currently paying off my last, charged-off credit card. Should I open a new line of credit or just continue to pay my debt to rebuild my credit?

Getting back on your feet after a period of unemployment and high debt is a huge accomplishment. Rebuilding your credit depends on multiple factors and on where you stand with your overall credit and finances. So, in your situation, I recommend doing it all: pay all your bills on time, continue to pay down your debt, and rebuild your credit health with positive account activity and a new line of credit.

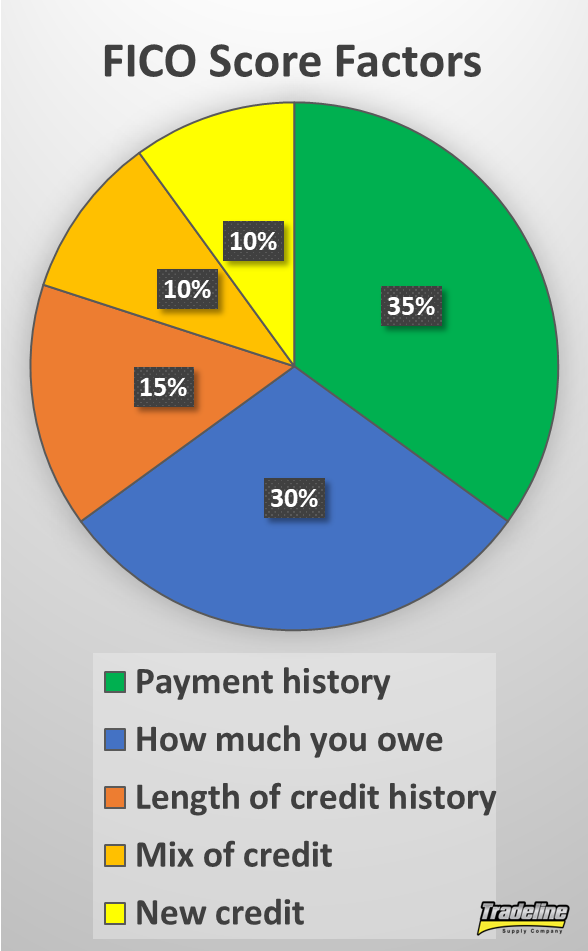

As you work to improve your credit, you should know which factors influence your score and learn how to use them to benefit your score. These factors include paying your bills on time, keeping your utilization ratio low, how often you get new credit, the types of credit you have, and for how long you’ve had credit.

Ways to Improve Your Credit

Arguably, the most important thing you can do for your credit is always paying your bills on time. This should become second nature so that you build your credit now and maintain a good score in the future. Then, if you don’t have an active account on your credit files, you could apply for a new credit card in order to generate a positive credit history on your credit reports. One sure way to open a new account is to apply for a secured credit card. Secured credit cards are offered by many banks and have a variety of perks and fees. Apart from looking and acting like any other type of credit card account, the primary differences are that you are approved without a credit check and you need to send a security deposit when you open the account. This deposit typically becomes collateral that establishes your credit limit and it’s returned to you if you close the account or if your account is upgraded to an unsecured credit card.

Be Strategic

Once you have your credit card, use it strategically. This means paying on time and keeping your utilization ratio below 30%. Your utilization ratio is how much of your available credit you are using. So, when you have high credit card debt, you appear at risk of losing control of your financial stability, which brings your score down. That’s why you should continue to pay off your debt in order to reduce your utilization ratio.

The other factors—the age of your credit, the types of credit you have, and how often you use your credit—are also important to a lesser degree. How old your credit is only will improve with time, so be patient. The mix of credit looks at the type of credit you have—credit cards and loans. But, right now, let’s focus on the primary factors. And last but not least, that’s how often you apply for new credit. When you ask for a new credit line, a hard inquiry is generated, and it remains on your report for 24 months. Too many inquiries bring down your score. So, you must be selective and strategic about getting new credit lines.

As you can see, building your score comes down to being strategic about how you use your credit in every transaction. When you have the tools and the right plan to improve how you manage your credit, it becomes easier to make financial decisions that build a stronger credit rating. If you need help with more personalized strategies to work on your credit, you can reach out to an NFCC Certified Financial Counselor.

The NFCC often receives readers questions asking us what they should do in their money situation. We pick some to share that others could be asking themselves and hope to help many in sharing these answers. If you have a question, please submit it on our Ask an Expert page here.

This week’s question: I need some advice in regards to my credit report and good ways that I can begin to build up my credit. I have no credit at all. Eventually within five years once I’m out of school I want to buy a house.

Building credit from scratch will take some time and effort, just like getting a job after graduating from school. You can think about good credit as a means to an end: you need good credit to finance big purchases and get the best interest rates and repayment terms on loans and mortgages. So, getting your credit ready is an excellent start to buying a home in the near future.

What is on Your Credit Report?

Your credit is a record of your monthly financial credit transactions. Your creditors report your activity to the three credit bureaus, Equifax, Experian, and TransUnion, and they use that data to generate a credit score. Your credit report also includes your personally identifying information such as your name, addresses, social security, and some public records such as bankruptcies and judgments and tax liens, if you have any. To start generating data for your credit report, you need to get a credit line. The easiest way to do that is to get a secured credit card. Many banking institutions issue secured credit cards, and they work pretty much like a regular credit card. The main difference is that these cards are backed by a cash deposit, which usually corresponds to the card’s credit limit.

Be Strategic

Learning how to use your credit card strategically is equally as important as getting that credit line. Your credit score takes into consideration several factors. The factor that influences your score the most is whether you pay your accounts on time and as agreed. Late or insufficient payments are very detrimental to your credit history. So, you should plan to pay in full and before your due date. Another important factor is your utilization ratio, which is how much you owe compared to your available credit. To have a balanced ratio, experts recommend that you use only 30% or less of your available credit in every billing cycle. For instance, if you have a $500 credit limit, you should be using less than $150.

Yet another factor is the age of your credit history. The older your credit history, the more history and data you’ll have to establish a solid credit history. Achieving this will just require time and your continued effort. The other two factors to keep in mind are the mix of credit you have (credit cards and loans) and how often you ask for new credit. Too many new credit inquiries reflect negatively on your score, so it’s important that you only apply for new credit sporadically. In your case, you should keep your secured credit card for at least a year before applying for a regular credit card. In some cases, your creditor may even upgrade your secured credit card to a regular one and return your cash deposit.

It’s never too soon to start building your credit. And once you learn healthy credit management habits, it will be very easy for you to manage your credit and use your credit cards responsibly on a daily basis. If you feel you need additional guidance or personalized help to get you started, you can always reach out to an NFCC Certified Financial Counselor. They are ready to help over the phone, online, and in-person if it’s available in your state. Good luck!

The vast majority of lenders use your FICO credit score to evaluate your credit risk as a consumer when they are deciding whether or not to extend credit to you. And yet, historically, it has been costly for consumers to access their own FICO scores.

Popular websites such as Credit Karma and Credit Sesame offer free credit scores, but the scores provided are usually VantageScores, not FICO credit scores.

Knowing your VantageScore is still valuable information, but it is not directly tied to your FICO Score, so it is less useful when it comes to preparing to apply for credit. While it is often true that a consumer’s FICO score is similar to their VantageScore, in some cases, they may be vastly different, especially depending on which credit scoring models are used and which credit bureaus are providing the credit report information.

If you need to check your FICO score, where can you do so without paying a fee to access it?

Here are some of the best places to get your FICO score for free.

Your Credit Card Issuer

Several major credit card issuers now offer consumers the ability to check their FICO scores for free.

Discover Bank

Discover offers a free way to check your FICO score with their Credit Scorecard program. Even consumers who do not have a relationship with Discover Bank can freely use this feature.

Experian provides the credit report data that is used to calculate your FICO score. Your credit score updates once every 30 days and Discover notifies you when it is time to check your new FICO score.

In addition, Discover’s FICO Credit Scorecard keeps track of your credit score history so you can see how it changes from month to month.

The Credit Scorecard also provides a summary of what is going on with each of the five credit score factors that are influencing your FICO score: your payment history, credit utilization, length of credit history, mix of credit, and new credit (e.g. inquiries). You can find educational information about credit scores on the website as well.

To access your FICO score with Discover’s FICO Credit Scorecard, either visit their website or use the bank’s mobile app.

Bank of America

Bank of America is another widely used bank that offers free FICO scores to consumers. However, to enroll in this program, you must be a Bank of America credit card customer.

Much like Discover’s offering that we described above, Bank of America’s FICO Score Program provides customers not only with their FICO scores but also information on the major factors that influence your credit score, your month-to-month credit score history, and education about how to achieve and maintain good credit.

On top of this, Bank of America also compares your credit score to the national average.

Bank of America customers can view their FICO score for free on the company’s website or mobile app.

Citibank

Consumers who have Citibank branded credit cards can obtain their FICO score for free from Citi.

Citi states on their website, “We think it’s important to provide our cardmembers with free access to information that will help them understand and stay on top of their credit status. That’s why we’re providing you with your FICO® Score and information to help you understand it.”

Your FICO score from Citibank is determined using information from your Equifax credit report and the FICO Bankcard Score 8 credit scoring model. Unlike the standard version of FICO 8 that you may be used to seeing, which ranges from 300 to 850, the bank card model used by Citi ranges from 250 to 900. It is updated once a month.

You can find more information on Citi’s free FICO score program on their website.

American Express

Recently, American Express started providing access to free FICO scores to consumers who have American Express credit cards.

The bank uses the standard version of FICO 8, so the credit score range spans from 300 to 850. Experian provides the credit report data used to calculate your score.

As with the other free FICO score programs, you also get to see how your FICO score changes over time and you receive a summary of the factors affecting your credit score.

American Express credit cardholders can see their FICO scores in their online account or on their monthly statement.

Those who do not have credit cards with American Express can get their TransUnion VantageScore for free through the company’s MyCredit Guide program, but this does not include FICO scores.

Barclays

FICO scores from TransUnion are available to all Barclays credit card customers through the bank’s online banking system.

Once you have had your Barclays card for three months, you can see a chart of your FICO score history over the time you have had an account open with Barclays, according to SmartAsset.

Plus, Barclays will send you alerts via email if your credit score changes, including an explanation of why your score has changed.

Wells Fargo

Wells Fargo account holders who use their online banking platform can view their FICO credit score within their online account.

Additional features include your credit score history, information on your credit score factors, and personalized credit tips from Wells Fargo.

According to the bank, they offer your FICO score for free in order to “support your awareness and understanding of FICO® Credit Scores and how they may influence the credit that’s available to you.”

The FICO score you get through Wells Fargo is calculated using Experian credit report data and is updated once a month.

Experian

Experian is the only major credit bureau that offers consumers their FICO 8 scores for free along with their Experian credit reports.

In addition, Experian offers an alternative credit data program called Experian Boost, which can add positive payment history from certain bills to your credit report, such as utilities and Netflix.

Sign up on Experian’s website to start using these free services.

Your Local Bank or Credit Union

Not all banks and credit unions offer customers the ability to check their FICO scores for free, but it is worth asking if you do not have access to the previous options. If your local bank or credit union does not offer free FICO scores, they may be able to help direct you toward somewhere that does.

Will Checking Your FICO Score Hurt Your Credit Score?

Although this is a common concern, checking your own credit score should never hurt your credit.

This credit myth likely arises from the fact that hard inquiries on your credit report can have a small negative effect on your score.

However, hard credit inquiries only happen when you are actively seeking credit and a lender has to pull your credit report to decide whether or not to loan you money.

All other credit checks, including those you conduct yourself for educational purposes, are considered to be soft inquiries, which do not affect your score at all.

Final Thoughts on How to Get Your FICO Score for Free

If you want to be able to see your FICO score for free, there are many options available to you, especially if you have credit card accounts with major banks such as those listed above.

FICO also has a program called FICO Score Open Access that aims to enhance consumer access to FICO scores and educate consumers about the topic. FICO has a list of additional lenders and credit and financial counseling organizations that participate in this program, which you can browse in case you do not have any accounts with the banks mentioned here.

Keep in mind that lenders use many different versions of FICO scores, including older generations and versions that are specific to certain industries. That means that when you check your FICO score for free, it is not guaranteed to be the same exact FICO score that a lender will use when you apply for credit.

When you check your FICO score using one or more of the methods in this article, take note of which credit bureau is supplying the information as well as which FICO score version is being used to calculate the result so that there is no confusion if you see a different FICO score somewhere else.

Finally, remember that you can also get your VantageScore for free in many places as well. While it’s not the same as your FICO score, it can still provide educational value as it uses the same general principles to calculate your score.

Let us know if this article helped you find a way to get your FICO score for free by commenting below!

It’s never a good feeling when you notice that your credit score has dropped. You might feel confused or concerned, and you would probably wonder why your credit score took a dip. Let’s explore some of the possible reasons that could cause your credit score to decline.

Your average of accounts decreased because of a new account.

As we’ve written about many times in the articles in our Knowledge Center, the age of a tradeline is extremely important, as is your overall credit age. This is because credit age is linked to payment history, which is vitally important to your credit health.

Payment history makes up 35% of your credit score and credit age contributes 15% to your score. When you add the two together, you get 50%, which means that half of your credit score is controlled by these two connected factors.

Within the credit age category, your average age of accounts is thought to be one of the most important variables. The more age your tradelines have, the more they can benefit your credit. Therefore, anytime you decrease your average age of accounts, you run the risk of your score decreasing as a result.

So if you recently opened a new primary tradeline or if you were added as an authorized user to an account that lacks age, the decrease in your average age of accounts might be what’s behind your credit score troubles.

Your account balances increased.

Did you use credit to make a large purchase recently? Have you been accumulating more debt by not paying the full balance you charged each month? If either of these scenarios is true for you, that could explain why your credit score took a dive.

As your account balances increase, so does your credit utilization rate. This is bad news for your credit score since credit utilization contributes about 30% of your score.

If you’ve been using your credit card more often without paying it off entirely each month, that could be the source of the change in your credit score.

Low utilization is favorable since it indicates that you are not overextending yourself financially. On the other hand, high utilization shows that you are using a lot of your available credit, which means you are statistically more likely to default on a debt in the future. For this reason, high credit utilization is penalized by credit scoring models.

Fortunately, there are many strategies you can use to overcome the problem of high revolving credit utilization, such as pre-paying your credit card bill before your statement closing date, making more frequent payments throughout the month, increasing your credit limit, or getting a balance transfer card.

When you open a new account, it can hurt your credit score for a few reasons. The first and most important reason is that the account has no age, which means it is going to negatively affect your average age of accounts.

In addition, there was likely a hard inquiry on your credit report as a result of applying for the new loan. In “Are Inquiries Really Killing Your Credit? What You Need to Know,” each recent hard inquiry on your report may affect your credit score by up to five points.

The new account may also have a negative impact on the “new credit” portion of your credit score. Having new credit makes you look like a riskier borrower, which means it could slightly reduce your score.

However, new credit only makes up about 10% of your credit score, so the impact of opening one new account would likely be relatively small and it would diminish over time.

You applied for credit but your application was denied.

Applying for a loan or credit card, whether your application is approved or denied, the resulting hard inquiry could damage your credit score slightly.

As we just mentioned, when you apply for credit, the lender usually has to do a hard pull (AKA a hard inquiry) on your credit report to see if you qualify.

This doesn’t always result in a new credit account being opened. Sometimes, for example, your credit application might get rejected by the lender, or perhaps you may choose to decline the terms you were offered and not proceed with opening the account. (Note, however, that when you apply for a credit card, typically the account is automatically opened when you get approved for the card.)

Unfortunately, even if you didn’t actually end up opening a new account, the fact that you applied for credit can still hurt your score. The hard inquiry still goes on your credit report whether you opened an account with that lender or not.

If you only applied for one account, then your credit score will likely only fall by a few points, if at all. If you applied for several accounts that you didn’t open within the past year, however, it’s possible that you could see a bigger dip in your score as a result of all of those inquiries on your report.

You missed a payment once or twice.

You might think that missing a payment here and there is not that big of a deal, but in reality, it can wreak havoc on your credit score. Recall that payment history is the most important factor contributing to your credit score, weighing in at 35% of your FICO score.

If you are 30 days late on making a payment even one time, this can have a significant detrimental effect on your credit, dropping your score by as much as 60 to 110 points.

If you still fail to make your payment by the following due date, then you get a 60-day late on your credit report, which hurts your credit even more.

30-day and 60-day lates are both considered minor derogatory items on your credit report, so they won’t mess up your credit as much as a major derogatory item.

However, if you get a 60-day late payment added to your credit report, do your best to catch up on payments before another 30 days pass, which is when things get even worse.

You missed a payment for three months in a row or more.

Missing a payment even once can seriously set back your credit score, but the damage will be even worse the longer you put off bringing the account current.

Once you reach 90 days past due on a credit account, that is now considered a major derogatory item, which is the worst possible type of item to have on your credit report. (Other major derogatory items include charge-offs, collections, foreclosures, settlements, judgments, repossessions, public records, and bankruptcies.)

Having a 90-day late on your credit report is certainly going to have a negative impact on your credit. A credit score drop from a major derogatory item will be even more severe and more difficult to recover from than that of a minor derogatory item. In addition, the major derogatory item could scare away potential lenders, making it harder to obtain credit in the future.

If you default on a debt, meaning you did not fulfill your obligations to repay that debt, your creditor can sell your account to a collection agency, who will then try to collect the debt from you. A collection account is also a major derogatory item on your credit report, which means it can seriously hurt your score if you have an account go into collections.

You applied for multiple credit cards in a short period of time.

Applying for multiple credit cards results in hard inquiries on your credit report, which can have a more significant impact on your score than just one inquiry.

Having too many hard inquiries on your credit report in a short period of time indicates that you are seeking a lot of new credit, which is a bad sign to lenders, and it will bring down your score.

With most credit scoring models, inquiries for credit cards are all counted separately, even if they were all around the same time. Since inquiries can each cost your credit score up to five points, that can add up quickly. (The exception to this is the VantageScore credit score, which counts all inquiries made within a 14-day window of each other as one inquiry, regardless of the type of account.)

Furthermore, if you got approved for and opened all of the accounts that you applied for, then you could also end up with too many new credit accounts on your credit report.

One of your credit cards was closed.

Many consumers mistakenly believe the credit myth that it will help their credit if they close some of their accounts. In a way, that makes sense, because it lowers the amount of available credit you have, which reduces the potential amount of debt you could get into if you were to use all of your available credit.

However, that is not how credit scores work, because unfortunately, credit scores don’t always make sense.

The truth is that closing an account almost always hurts your credit instead of helping it.

With revolving accounts, such as credit cards, closing an account reduces your total credit limit by removing the credit limit of that card. When you reduce your credit limit, that action increases your overall credit utilization ratio, meaning that you are now using a larger fraction of your available credit.

This hurts your credit score because having a high credit utilization ratio is penalized by the credit scoring algorithms, whereas maintaining a low utilization ratio is rewarded.

The worst-case scenario for your credit when closing an account is if the account is closed while it still has a balance on it. In this case, that individual account will look like it is maxed out or over the limit because it has a balance but no credit limit. That alone is enough to significantly harm your credit, and the increase to your overall utilization ratio only worsens the problem.

Depending on what else is in your credit file, closing a credit card could also negatively affect your credit mix, which could result in a small credit score drop.

On the plus side, the reason why an account was closed does not play a role in your score, so you won’t be affected more negatively if the card was closed by the issuer than if it was closed at your request.

Have you checked your credit card statements lately?

An unexpected decrease in your credit score could be the result of fraudulent activity on your accounts.

If you see any charges on your statement that you do not recognize, then it could be fraudulent activity that is bringing down your score. Perhaps someone was able to obtain your credit card information by phishing or through a data breach and used it to run up the balance on the card.

It’s important to monitor your credit accounts regularly so that you can catch any suspicious activity early on. Better yet, set up email or mobile notifications on your account that will alert you to fraudulent activity instantly.

If a criminal does manage to get access to your account, report the fraudulent charges to your credit card issuer immediately and ask to have the charges reversed. Most credit card companies have a zero liability policy, which means you won’t be held responsible for paying for any of the fraudulent charges.

You paid less than the minimum payment.

If your cash flow is tight, it can be tempting to send the bank or credit card company a partial payment instead of the full amount that is due that month. You may think that it’s not as big of a deal as not paying at all, because at least you are sending them some of the money.

Unfortunately, it doesn’t work that way. If you do not cover the full minimum payment by the due date, it will not be counted as an on-time payment.

If you can bring the account current before 30 days pass, you may still have to deal with a late fee from your credit card issuer (although it’s worth asking them to waive the fee), but at least the late payment will not show up on your credit report.

On the other hand, if you do not make a sufficient payment and 30 days go by, then you will have a late payment pop up on your credit report, which can definitely take a toll on your credit score.

To prevent this from happening, as soon as you know you will not be able to make the full payment, contact your credit card issuer and ask if they have a financial hardship program or try to negotiate an arrangement with them that allows you to pay what you can without damaging your credit.

You didn’t use your credit card for a long time.

Your credit card issuer might have closed your account if it had been inactive for a long time.

If you don’t use a credit card for a long period of time, it’s possible that your credit card issuer may decide to close your account due to the lack of activity.

As we discussed above, a closed credit card is bad news for your credit since the loss of available credit hurts your credit utilization and it may also damage your mix of credit.

According to The Balance, the credit card company is not required to give you advance notice if they plan to close your account, so it’s best to take proactive measures to prevent this from happening.

To avoid having your card closed due to inactivity, make sure you use it to make a purchase at least once every few months. An easy way to do this is to use the credit card to pay for a subscription service that renews each month. Then, set up automatic bill payments on your credit card and the whole process will be automated.

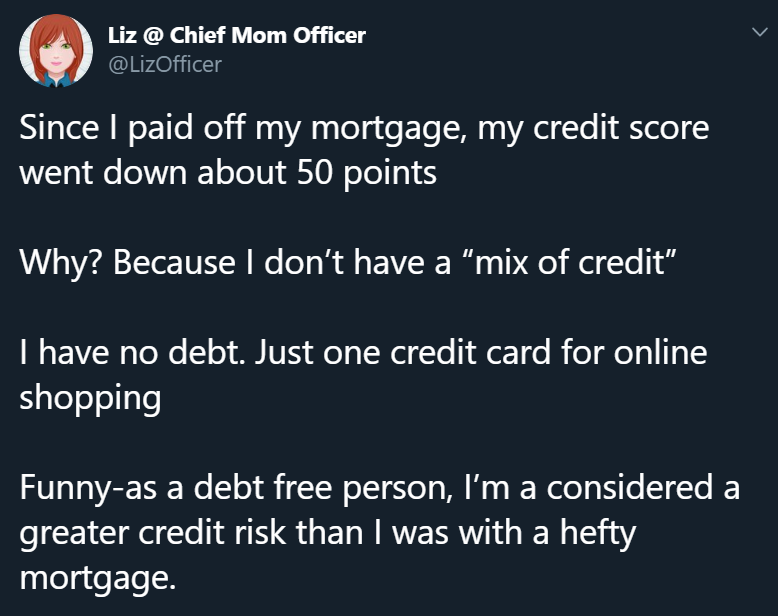

You finished paying off an installment loan.

Making the final payment on your auto loan, student loans, or mortgage is an exciting accomplishment. Yet, when you finish paying off an installment loan, your credit score may decrease instead of increase.

Even though you now have less debt, which sounds like it would help your credit score, this may not outweigh the negative impact to your mix of credit. The paid-off installment loan will now report as a closed account, which can be harmful to your credit if all you have left is a few revolving accounts.

@LizOfficer shared a real-life example of this on Twitter.

This Twitter user commented that paying off her loan made her credit score go down since it affected her mix of credit.

An account that you are piggybacking on became delinquent.

Sometimes being an authorized user on a credit card or having a joint account can be a risky thing. You are relying on the other person to pay their bills on time and to manage their balances well, otherwise their behavior can compromise your credit.

In other words, an ideal tradeline should have a low utilization ratio, it should have a higher age than your average age of accounts and your oldest account, and most importantly, it needs to have a perfect payment history.

Therefore, you want to avoid being added as an authorized user to a tradeline that has any derogatory marks on it so that those derogatory items don’t get added to your credit file and end up damaging your credit.

That’s the danger of piggybacking on a friend or family member’s credit card—even if the tradeline is perfect when you are first added to it, there’s no guarantee that it will stay that way.

If your authorized user tradeline does get any missed payments on its record, that could definitely hurt your credit, and it would be smart to remove yourself from it immediately. To do so, simply call the credit card issuer and request to be removed from the account, as most banks allow you to do this without needing to go through the primary account holder.

Delinquency on the part of the primary account holder can cause problems if you are piggybacking on someone else’s credit account.

You declared bankruptcy.

Bankruptcy is one of the worst things you can have on your credit report. Since declaring bankruptcy essentially means you are asking to be released from the legal obligation to repay your debts, it shows lenders that you have an extremely high risk of defaulting in the future, so it can have a severe negative impact on your credit score.

There are inquiries on your credit file that you did not authorize.

Unauthorized inquiries on your credit file can unfairly drag down your credit. In our article on credit inquiries, we reported that each hard inquiry on your credit report can potentially cost you up to five points each.

Fortunately, you have the right to dispute any hard inquiries on your credit report that you did not authorize. You can learn more about the credit dispute process in “How to Fix the Most Common Credit Report Errors.”

Your credit file got merged with someone else’s.

Sometimes inaccurate information can get on your credit report not as a result of fraud or because your lender reported it incorrectly, but because your credit file accidentally became mixed with the information of another person.

This is called a “mixed credit file” or “mixed credit report” and it usually occurs with two consumers who have similar names.

If the credit history of the other consumer with whom your file has been mixed contains negative information, that would obviously be detrimental to your score, and you would need to correct the situation by filing a dispute with the credit bureau.

This is an example of why it’s important to check your credit report regularly. If there is incorrect information on your credit report that should be removed, you don’t want to find out about it when you’re trying to apply for credit. You need to catch and correct credit report mistakes early so that they don’t stand in the way of you achieving your financial goals.

You maxed out one or more of your credit cards.

Credit utilization makes up nearly a third of your FICO score, which means it’s critically important to keep your utilization low if you want to maintain a high credit score. Maxing out even just one credit card can have a significant negative impact, and if you max out multiple cards, you’ll be even worse off.

An account on your credit report that you don’t recognize could be an account that someone else fraudulently opened in your name.

We already covered how opening a new account can negatively affect your credit initially, but don’t forget that the same thing can happen if someone else uses your name to sign up for a new account.

If you see that your credit score has decreased, take a look at the inquiries and accounts on your credit report to see if there are any items that should not be there.

You have “double jeopardy” with collection accounts on your credit report.

Debt collection agencies are not known to be the most trustworthy entities and often do not have the best practices when it comes to keeping track of debts and contacting consumers. Information often gets lost or misrecorded when it is transferred between creditors and sometimes numerous collection agencies.

Because of this, some consumers find themselves with more than one entry for the same open collection account on their credit report, which is known as “double jeopardy.”

While the same collection may be listed multiple times due to the account changing hands, only the entity who currently owns the debt should be reporting the account as open.

Fortunately, if a collection is being reported in error, you can dispute the inaccurate information and have the information be corrected or potentially removed altogether.

Your credit report says you missed a payment even though you paid on time.

Dispute any mistakenly reported late payments so that they don’t unfairly affect your credit score.

Since payment history is the most important factor in your credit score, an incorrectly reported missed payment could severely damage your credit, especially if you are starting with very good credit. The higher your score to begin with, the more you stand to lose from a credit mistake.

This type of situation is another example that demonstrates why it’s so crucial to regularly check your credit report. If you always made all of your payments on time, you might assume that you must have a spotless credit record, only to find out at an inconvenient time that a creditor has been incorrectly reporting that you missed a payment.

Keep an eye out for errors like this on your credit report so that you can dispute them right away.

Your credit card issuer reduced your credit limit.

Sometimes, credit card issuers lower the credit limits of their cardholders, even for those who have consistently managed their accounts responsibly.

Unfortunately, they are usually allowed to do this without asking for your permission or letting you know in advance, so it may come as a nasty surprise when you swipe your credit card and get declined, or when your credit score takes a dive because your credit utilization is suddenly much higher.

There are a few reasons why your bank may reduce your credit limit, such as the following:

Credit card issuers sometimes cut credit card limits, which hurts your credit utilization ratio.

Your balances have been increasing, which indicates that you are taking on more debt and might be at a greater risk of defaulting. You missed a payment and your account becomes delinquent. Your account was inactive because you did not use your credit card enough. The economy is down and lenders want to minimize their risk exposure levels.

Regardless of why your credit limit took a hit, the result is the same: with less available credit, your credit utilization increases, which is bad for your score.

If your credit card issuer slashed your credit limit, check out “How to Increase Your Credit Limit” for some useful tips, and don’t be afraid to give your bank a call to ask them to reconsider.

A collection account was deleted from your credit report.

Surprisingly, it is actually possible that getting a collection account removed from your credit report could make your credit score go down instead of up.

By removing a collection account from your credit report, it is possible that you could move from one bucket into another bucket where your score will now be calculated differently. As a result of this new algorithm being applied to your credit report, your score could turn out to be lower than it was when you were in the first bucket.

You haven’t used any credit in a long time.

If you have used credit in the past but not recently, some of your old accounts may have fallen off of your credit report altogether. Accounts that are closed or inactive do not stay on your credit report forever. Positive accounts will generally stay on your credit report for 10 years, whereas negative accounts may stay on your credit report for up to 7 years.

When these old accounts age off of your credit report, you lose all of the credit history associated with them, the most important of which is the payment history. Because you are losing valuable credit history, your score could take a hit.

Those with thin credit files or those who have not used credit in several years will need to focus on building credit in order for their credit score to recover.

Conclusions

When it comes to your credit score, minor fluctuations are normal, so there’s generally no need to fret about losing a few points here and there.

If you are practicing good credit habits and paying all of your bills on time, it’s probably not necessary to watch your credit like a hawk and check your score every single week, and a change of a few points in either direction should not cause you to panic.

However, as we have seen, you don’t want to neglect your credit entirely, since mistakes can and do happen.

In addition, keep in mind that credit moves can sometimes have unexpected results, particularly in cases where you may be migrating from one credit scoring “bucket” to another.

If you see a significant drop in your credit score, that is definitely worth investigating further so that you can understand why it happened, address the issue, and hopefully get some of those credit score points back.

26 million consumers in America have no credit record whatsoever. On top of that, there are an additional 19 million consumers who do have credit files, but they do not contain sufficient credit information to be scored by a widely available credit scoring model. These consumers—in total making up nearly one in five American adults—are the “credit invisibles” and “credit unscorables.”

Due to a lack of credit history, these consumers are virtually invisible to the credit system. That means credit can be very hard or even impossible to obtain when it is needed. After all, we all know that “it takes credit to get credit,” since lenders often don’t want to take the chance of lending to someone with no prior credit record.

“Alternative data,” which involves using data sources other than traditional credit reporting information to make lending decisions, is a concept that is becoming increasingly popular as one possible solution to the problem of credit invisibility.

Let’s shed some light on the emerging topic of alternative credit data and how it could help or hurt consumers.

What Is Alternative Credit Data and How Does It Differ From Traditional Credit Data?

Traditional credit data refers to your credit report, credit scores, and the information they contain. In other words, traditional credit data primarily consists of information about how you manage your tradelines, which are the credit accounts you own.

When we are talking about credit, we are almost always discussing traditional credit data since that is what is used to make most lending decisions.

In contrast, alternative credit data is financial information about consumers that is not typically included in traditional credit reports. Examples of alternative credit data sources include rent payments, utility payments, full-file public records, and data from alternative financial service providers (ASFPs), such as payday lenders.

Traditional Credit Data Alternative Credit Data

Contains information about the tradelines in your credit report Information comes from other sources since there is insufficient credit data

Payment history for loans and credit cards Data from alternative financial service providers (e.g. payday lenders)

Credit utilization ratio Utility payment history

Delinquencies Rent payment history

Credit mix Consumer-permissioned data

Credit inquiries Full-file public records information

What Is the Purpose of Alternative Credit Data?

Alternative data includes data that consumers may choose to allow credit reporting companies to access, such as bank account balances.

For the millions of consumers who lack credit reports based on traditional credit data, building credit and obtaining credit is a challenge. Without a verified credit history, lenders cannot make an informed decision about whether to extend credit to a consumer.

One way the credit scoring industry is trying to address this problem is by creating new types of credit scoring algorithms that utilize different sources of data that are not contained within a consumer’s traditional credit report but still have predictive power with regard to a consumer’s credit risk.

These alternative data sources, such as rent and utility bill payments, are more accessible and more commonly used among those who are credit invisible.

The idea behind alternative credit data is that a consumer’s non-credit financial information can still be used to predict whether the consumer is financially responsible and creditworthy. This information can help lenders provide credit to consumers who may have a thin credit file or no credit file at all but who may still be creditworthy.

Therefore, using alternative data to make lending decisions could theoretically allow lenders to expand their customer base and earn more revenue while providing more credit to consumers who lack a traditional credit history.

How Do Consumers Benefit From Alternative Data?

The benefit to consumers, of course, is that many consumers who may be creditworthy but are invisible to the traditional credit system could potentially use alternative data as a path to building credit where they lacked one before.

For example, a consumer who gets a good credit score using an alternative data scoring method might now be able to get approved for an unsecured credit card, whereas they might have had to put down a deposit to get a secured credit card if the lender had only been able to use traditional credit data. This would allow the consumer to hold onto the cash they would have had to put down as collateral and instead save it for emergencies or some other use.

Applications of Alternative Credit Data

Consumers who are “credit invisible” but have a history of being financially responsible in other areas may benefit from the use of alternative credit data.

Although alternative credit data is still a relatively new field, major players in the credit industry are already working on developing new credit scoring tools that make use of alternative data.

FICO XD and FICO XD 2

FICO is working on developing new credit scoring models that can reliably assess the credit risk of consumers who are unscorable using traditional credit scoring methods.

The FICO Score XD “leverages alternative data sources to give [bankcard] issuers a second opportunity to assess otherwise unscorable consumers.”

Nerdwallet reports that the FICO XD model uses phone, utility, and cable payment data as well as things like information about your home if you are a homeowner, occupational licenses you may have, and your bank records.

Compared to traditional FICO scores, this model has the same credit score range of 300 to 850 and the same expected credit risk for each score group within that scale.

According to FICO, the XD scoring model can provide a score for more than half of all credit applicants that had previously been unscoreable, which adds millions of consumers to the scorable population.

Although only about a third of applicants that can be scored with FICO XD receive scores higher than 620, which is considered to be fair credit, the company claims that almost half of borrowers with higher FICO XD scores later go on to obtain credit and achieve traditional FICO scores of 700 or greater.

FICO XD’s newer version, FICO Score XD 2, works similarly but has been further refined to provide more accurate results.

Similarly, the FICO Score X incorporates alternative data sources for credit scoring, such as telecom payments, mobile payments, “digital footprint” data, and even data from psychological surveys to provide a way for international lenders to score previously unscorable consumers.

UltraFICO

The UltraFICO score, currently being pilot tested by Experian, will use “consumer-permissioned” banking data to enhance its scoring capabilities. In this case, what that means is that consumers can choose to contribute data about their checking, savings, and money market accounts in order to allow lenders to assess their creditworthiness by looking at their overall financial profile.

Some of the specific financial factors considered by the UltraFICO score include:

A history of positive bank account balances is a beneficial factor with the UltraFICO credit score.

How long you have had your bank accounts open How often you make banking transactions When your most recent bank account transactions occurred Verification that you often have money saved in your bank accounts A history of having positive bank account balances

FICO says this credit scoring model can help increase access to credit for “nontraditional borrowers” who have limited credit histories, particularly young consumers, immigrants, and those who are rebuilding their credit after experiencing financial distress.

The company also states that UltraFICO could potentially improve credit access for most Americans and could be especially helpful for those whose credit scores are in the “grey area” of the upper 500s and lower 600s or those whose scores just barely miss a lender’s credit score cutoff.

Seven out of 10 consumers who have had consistently positive banking habits in the past three months could get a higher UltraFICO score than their traditional FICO score, according to the company’s website.

Experian Boost Credit Score

Experian has also come up with their own alternative data solution called Experian Boost, which is a free service that allows users to provide access to their bank accounts in order to get credit for their on-time payments of bills such as electricity, water, gas, phone plans, cable, and even Netflix.

One major advantage with Experian Boost is that it only counts positive payment history, so missed payments will not hurt your score. If the program detects that you have missed a payment, it will remove that account from your credit file so that the late payment will not hurt your score.

Experian Boost lets you add positive payment history from your utility bills and some streaming services.

The New York Times has reported that the reason why Experian Boost does not consider negative information about your bills is that anything negative on your record will most likely end up on your credit report anyway, either because your utility provider may start reporting it to the credit bureaus or the account may get sold to a collection agency which then reports the collection account.

In addition, Experian says that you can disconnect your bank accounts if your FICO score decreases because of Experian Boost and that you can always reconnect your account later once your finances have improved.

According to Experian, consumers who sign up for Experian Boost receive an average boost to their FICO score of 13 points. Those who do not see a boost initially may see a larger effect over time if they keep their account connected as the program continues to check your account for payments you made on time and adding those to your credit profile.

If Experian Boost helps your credit but you later decide for whatever reason that you no longer want to use it, be aware that the positive payment history that was helping you will be removed from your credit profile, so it’s likely that your credit score will fall.

TransUnion FactorTrust

In 2017, TransUnion acquired FactorTrust, a company that provides lending data on short-term and small-dollar loans (e.g. payday loans), which are not reported in traditional credit reports and are often utilized by underbanked and credit invisible consumers.

This information will allow TransUnion to assess credit risk for a larger group of consumers.

In addition, TransUnion says that their small-dollar loan data will help lenders comply with the Consumer Financial Protection Bureau’s recent changes to payday lending rules meant to protect consumers.

Equifax DataX

In 2018, Equifax acquired a specialty credit reporting agency and provider of alternative credit data called DataX. Equifax stated that they plan to use DataX to help lenders improve financial inclusion and access to credit, especially for consumers who are underbanked.

DataX claims that they can help lenders better evaluate the credit risk levels of prospective customers by utilizing a “massive, proprietary consumer database that provides valuable insights on consumers not covered by traditional credit information sources.” This database contains demographic, financial, and credit data on millions of consumers.

The Downsides of Alternative Credit Data

In theory, alternative data sounds like a promising solution to the credit catch-22 and the problem of credit invisibility. According to FICO’s white paper on the subject, the use of alternative data allows millions of previously unscorable consumers to achieve credit scores that are high enough to get access to credit.

However, while the credit scoring and credit reporting companies only talk up the positives of their alternative data products, there are some drawbacks to this approach that also need to be considered.

Alternative Data May Perpetuate Credit Inequality

Although alternative data is marketed as a solution to credit invisibility, it’s possible that it could actually worsen credit inequality.

Despite FICO’s impressive claims, in the company’s white paper, we can clearly see how alternative data in credit scoring might not be so helpful to many consumers.

According to their research, about a third of the “newly scorable” consumers scored 620 or above using the alternative data score. These are the millions of consumers they refer to that may now be able to access credit.

But if only a third of consumers scored 620 or above, that means two-thirds of consumers now fall below 620 with the alternative data score, which is considered bad credit. That means there are twice as many of the newly scored consumers who end up with bad credit than those who end up with good credit after the alternative data model has been applied.

In many cases, having bad credit is even worse than having no credit, because instead of starting from scratch, you have derogatory information on your credit report that is going to weigh down your credit score. This can make it even more difficult to get your credit to a good place than if you had started with no credit history at all.

The results of FICO’s alternative data research bear out the concerns presented by the National Consumer Law Center (NCLC). According to the NCLC, if utility payments become part of the credit reporting system, this could result in millions of consumers getting negative marks and would disproportionately impact low-income consumers and people of color.

Although alternative credit data is pitched as a way to lift millions of consumers out of credit invisibility, in reality, it is another profit-generating tool created by the credit scoring and reporting companies to sell to financial institutions. Any benefit or harm to consumers is incidental to the primary goal of the banks making more money by lending to more consumers.

As you know from our article, “What Happened to Equal Credit Opportunity for All?” the credit scoring system was built upon and continues to perpetuate a history of financial inequality in our country.

Unfortunately, although it has the potential to help millions of consumers if implemented in the right way, it seems likely that alternative credit data may just end up being used to continue the legacy of inequality and discrimination that is still firmly entrenched in the credit industry and in our society in general.

Data Privacy Concerns

Another major concern with alternative data is privacy. In recent years, major data breaches have been happening left and right, including the 2017 Equifax breach that compromised the information of around 148 million consumers. The credit bureaus have shown with multiple egregious security breaches that consumers cannot trust them to safeguard their personal information.

Experian Boost, as well as other similar “consumer-permissioned” data reporting systems, require users to allow access to their bank account in order to report bill payments. For many, it may be hard to stomach the idea of giving FICO or the credit bureaus access to their personal information when they have repeatedly mishandled sensitive consumer data. Those who do choose to use such services do so at the risk of their information potentially being compromised.

Some Lenders May Not Use Alternative Data Credit Scores

Since alternative credit data is still a relatively new development, one downside is that many lenders may not be using alternative data or credit scores based on it in order to make their lending decisions.

The credit industry is slow to change, as we talked about in “Do Tradelines Still Work in 2020?”, so it may take several years for alternative credit data to be widely adopted.

Therefore, at this time, there is no guarantee that your lender of choice will have the ability to access and use your alternative credit data.

Conclusion: Is Alternative Data Helpful or Harmful?

Alternative data has the potential to lift millions of consumers out of credit invisibility, which is a step toward providing equal credit opportunity to these consumers.

However, it has just as much potential to harm consumers and perpetuate credit inequality due to the issues we discussed above.

As with any credit reporting or credit scoring tool, we have to remember who these tools are designed for and who they are intended to serve: the banks.

Ultimately, the purpose of alternative credit data is to help lenders make more money by lending to a greater number of consumers. For consumers, the benefits and risks are not so clear cut.

If you have no credit record or a thin credit file, alternative credit data scoring systems may be worth considering and trying out. As with any major credit moves, be sure to do your due diligence as a consumer by researching how these programs work and how you can protect yourself and your credit if you do not get the results you are looking for.

What is your take on the issue of alternative credit data? Have you tried any of these alternative data services yourself? Drop a comment below to let us know your thoughts!

Your credit score is a seemingly simple three-digit number, but it can have a major impact on your finances. Without a high score, you may not be able to pursue some of your major financial goals. Or even if you can, those goals can actually turn into major challenges if you’re stuck with high interest rates because you had a low score. If you are preparing to improve your credit, you need to know the general ranges for scores so that you can set a specific goal for yourself. There are various tiers of credit scores, and being in a higher tier will generally bring the reward of better terms.

First, What’s the Average?

We’re going to talk about credit score categories in a moment, such as “poor,” “fair,” and “good.” But first let’s take a look at the average credit score. One initial point of clarification—while there are two major credit scoring models—FICO and VantageScore—we will focus primarily on the FICO score in this article, though we will make brief mention of the VantageScore as well. There are actually multiple FICO scoring models, and lenders use a variety of them, but the information here specifically relates to FICO® Score 8.

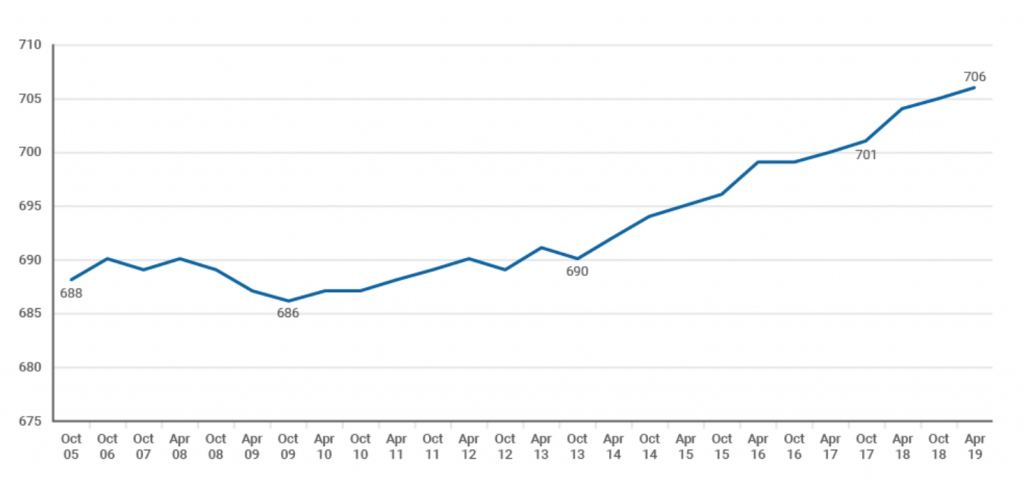

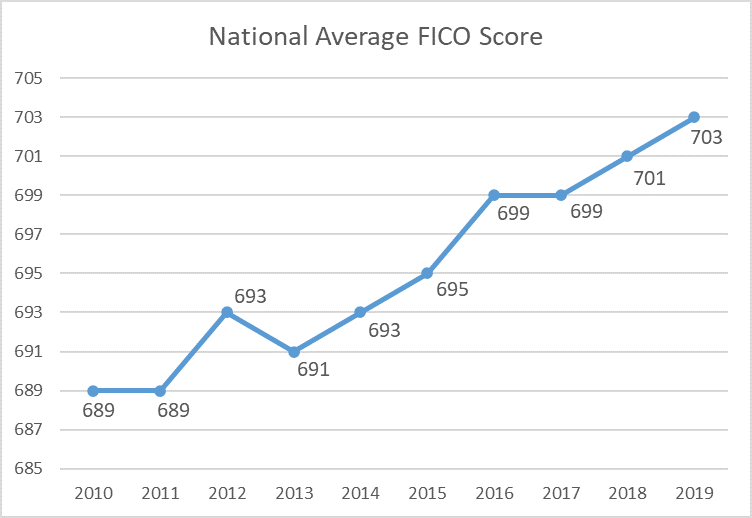

FICO most recently reported that the average credit score is 706. Credit scores nationwide can fluctuate significantly depending on the state of the economy. Back in 2009, the average was 686. COVID-19 and other economic factors may have a negative impact on the national average, but only time will tell. The average can be a useful baseline for comparing your own score. But, don’t let the average discourage you if your score is lower, because there are many ways to increase your score.

Source: FICO.com

The Breakdown

Using the FICO 8 scoring model, the credit bureaus agree (see Experian’s post here and Equifax’s here) to the following breakdown for score ranges. Again, remember that your lender may use a different model which could result in a slightly different breakdown. But, this should give you a good general idea of what to aim for.

Poor

A poor credit score is a score between 300 and 579.

Fair

A fair credit score is a score between 580 and 669.

Good

A good credit score is a score between 670 and 739.

Very Good

A very good credit score is a score between 740 and 799.

Excellent

An excellent credit score is a score between 800 and 850.

If you are curious about the breakdown for VantageScore 3.0, it looks like this:

Interestingly, the VantageScore ranges are narrower on the low end of the spectrum (including both a “very poor” and “poor” range, and broader on the high end (including only a “good” and “excellent,” without a “very good” range).

Why the Ranges Matter

Now that you know the ranges, here are three important reasons that they matter.

Access to Credit and Other Services

If your score is too low you may not have access to credit or, at the very least, you will likely have obstacles to credit. A score in the “very poor” range may mean that any applications for credit are denied. Your best bet may be a secured credit card, which requires you to make a deposit. While this is not ideal, a secured card can be an important tool in rebuilding your credit.

Also, remember that getting credit is not the only concern. Access to other products and services often depends, in part, on your credit history. Being in the “very poor” range can limit your ability to rent an apartment, enter certain contracts, or even get a job.

Favorable Credit Terms

Even if you can get credit, you will want the credit terms to be as favorable as possible. Bad credit terms, like high interest rates, will make your debt more expensive. They will also limit your purchasing power, which can prevent you from buying the home or car you want. Every time your score improves from one category to the next (say from “fair” to “good”), that should be paired with lenders offering you more favorable terms.

Here is a look at estimated mortgage rates by credit score and a look at auto loan rates by credit score. Note: these tools use different ranges and terminology for scores (for instance, the auto loan chart has ranges from “deep subprime” to “super prime”), but the general point still applies.

Goal Setting

Knowing the general credit score ranges can help you plan your goals for the future. Make a plan to check your credit score frequently, but especially as you make major changes (paying off a debt, opening a new card or loan, or changing your credit limit). You will also need to check your credit report often, as that report is the basis for your score. Keeping a close eye on these will help ensure that you move your credit in the right direction.

Want a free credit report review? An NFCC-certified counselor can review your credit report with you, and help you make a game plan for improving your financial standing. Learn more about the free credit report review, or get started here.

FICO, the company behind the creation of the original FICO credit score and its many subsequent iterations, has announced the latest model in their line of credit scoring algorithms: the FICO Score 10 and the FICO Score 10 T. The “T” in the latter scoring model stands for “trended,” which reflects the incorporation of trended data over time into the algorithm.

Thanks to not only the trended data but also a few other major changes, the new scoring models are claimed to be superior to all previous FICO scores.

Although the majority of consumers are not likely to see a dramatic change in their credit scores, some groups of consumers may experience more extreme shifts. Ultimately, the new FICO scores are predicted to widen the gap between consumers with good credit versus those with bad credit.

However, none of that matters until FICO 10 and 10 T actually start being used, which could still be a few years away.

Keep reading to get all the facts on FICO 10, including what makes it different from previous FICO score versions, the impact it will have on credit scores, and when we will start to see lenders adopting it. Most importantly, we’ll tell you how to get a good credit score with FICO 10.

Why Did FICO Come Out With a New Credit Scoring Model?

The whole point of a credit score is to communicate a consumer’s level of credit risk to lenders so that lenders can make less risky decisions when granting credit. Lenders want to avoid extending credit to borrowers who are likely to default on a loan because defaults represent losses for the company.

So, the more accurate a credit scoring model is at predicting consumer credit risk, the more useful it is to lenders. With a predictive credit scoring model, lenders can make more informed lending decisions, which helps their bottom line.

For this reason, the goal of each new credit score is to make it better than the last version at predicting credit risk, and that is exactly what FICO 10 is designed to do.

Consumer Debt Is on the Rise—But So Are Credit Scores

According to The Balance, consumer debt has increased to record levels, and yet the average credit score in the United States has also increased to 706 as of September 2019. This can be attributed partly to economic conditions over time, but there is another major factor that has the banks worried.

The national average FICO score has been on the rise for the past decade and it surpassed the 700 mark in 2018.

It has now been 12 years since the Great Recession of 2008, which means almost all of the delinquencies and derogatory marks on consumers’ credit reports from that period of financial hardship have been removed from their records. Therefore, creditors can no longer see how consumers handled the recession and whether they were able to pay all of their bills when the economy went south.

Couple this with the fear of another possible economic recession on the horizon, and you can understand why lenders have started to feel concerned that delinquencies and defaults may soon begin to rise to a level that is not reflected in consumers’ high credit scores.

Because of these economic factors, the credit scoring system needed an overhaul that would take into account the changing economic climate as well as changing consumer behavior and allow for better predictions of credit risk and default rates.

FICO 10: More Accurate Predictions of Credit Risk

FICO predicts that FICO 10 will lower defaults on auto loans by 9% and defaults on mortgages by 17%.

Due to the changes made to the scoring model that we discussed above, especially the inclusion of trended data for the FICO score 10 T, FICO claims that the new scores perform better than all previous FICO scores by substantially lowering consumer default rates.

Here’s what else FICO has to say about their new products:

“By adopting the FICO® Score 10 Suite, a lender could reduce the number of defaults in their portfolio by as much as ten percent among newly originated bankcards and nine percent among newly originated auto loans, compared to using FICO® Score 9. The reduction in defaults is even higher for newly originated mortgage loans, at 17 percent compared to the version of the FICO Score used in that industry. These improvements in predictive power can help lenders safely avoid unexpected credit risk and better control default rates, while making more competitive credit offers to more consumers.”

How Is FICO 10 Different Than Previous FICO Scores?

Although FICO routinely updates their credit scoring algorithms every five years or so, this will be the first time that they are releasing two different versions of the same general scoring model: FICO 10 T, which uses trended data; and FICO 10, which does not use trended data.

Both FICO 10 and FICO 10 T will be drastically different than the previous FICO score, FICO 9. FICO 9 was designed to be very forgiving to consumers, which led many to believe that it produced credit scores that were higher than they should have been.

With FICO 9, for example, medical collections were given less weight than other types of collections, which was a benefit to consumers struggling with medical debt.

Furthermore, FICO 9 completely ignored paid collection accounts, meaning that if you had a collection on your credit report but then paid the balance, it would no longer affect your credit score. Many felt that this change contributed to FICO 9 overestimating the creditworthiness of consumers, which in turn led to the scoring model not being accepted by many industries.

In contrast, the FICO 10 scores represent a swing back in the opposite direction. It is designed to be less lenient toward consumers with risky credit behaviors in order to avoid understating consumers’ credit risk. In that sense, it is probably more similar to FICO 8 than to FICO 9. However, FICO 10 also rewards consumers who have successfully managed their credit.

To accomplish this, FICO made some significant changes in creating their latest set of credit scoring algorithms.

Trended Data

The new FICO 10 T score is the first FICO score to look at trended credit data.

The FICO 10 T score will incorporate trended data, which means that it will not just consider your credit profile as a “snapshot” in time, but rather, it will take into account your credit behavior over the previous 24 to 30 months and how your credit profile has changed in that time.

VantageScore 4.0, a competing credit scoring model, has been using trended data since it debuted in 2017. Now, FICO is following suit with their 10 T score.

Because of the more extensive temporal data set FICO 10 T has to draw from, it is even more predictive of a borrower’s credit risk than the basic FICO 10 score, which can only see a “snapshot” of your credit report at a given point in time.

For consumers, the trended data factor is especially significant for the credit utilization portion of your credit score. Of course, credit scores already looked at your payment history from the past seven to 10 years, but until now, they only looked at your credit utilization ratios at a given point in time.

This means that with most credit scoring models, even if you max out your credit cards one month and your credit score suffers as a result, as long as you pay down your cards again by the next month, your score can still bounce right back to where it was before you maxed out the card.

With FICO score 10 T, however, it won’t be so easy to recover from high balances, because a record of being maxed out could stick around for the next 24 to 30 months.

In addition, if your balances have been climbing higher over the last two years or if you have been seeking credit more aggressively, you could be penalized by FICO 10 T, because this kind of behavior indicates a higher risk of you defaulting in the future.

On the other hand, if you have been managing your credit well and your debt levels have been decreasing over the past two years, you will be rewarded for that behavior.

Personal loans from online lenders have exploded in popularity, but it’s best to avoid them if you want to get a high FICO 10 credit score.

Personal Loans Will Be Penalized

The vice president of scores and analytics at FICO, Joanne Gaskin, has said that the most significant change to the scoring algorithm is the way it treats personal loans.

Personal loans are growing faster than any other type of consumer debt, even credit cards. Consumers are turning to personal loans to consolidate credit card debt more frequently than in the past, and the proliferation of financial technology companies has made personal loans easier to qualify for and more accessible.

With older FICO models, personal loans are treated the same as any other installment loan. Since the balances of installment accounts don’t affect credit scores as much as the utilization ratios of your revolving accounts, with most scoring models, taking out a personal loan to consolidate credit card debt (essentially converting revolving debt into installment debt) would benefit a consumer’s credit score.

However, many consumers who take out personal loans to pay off revolving debt don’t change the spending habits that got them into debt in the first place. Consequently, after getting a personal loan and paying down their credit cards, they may run up their cards again and find themselves even deeper in debt.

According to FICO, the credit risk of such consumers is higher than you would think based on their credit scores using previous FICO models. To account for this, FICO 10 is treating personal loans as their own category of credit accounts and is potentially penalizing consumers for taking out personal loans.

With FICO 10 T, recent missed payments will matter even more than they already do with other FICO score versions.

Therefore, with FICO 10, the strategy of consolidating credit card debt with a personal loan might not help your credit score as much as you hope and might even hurt it. However, the negative impact of taking out a personal loan can be mitigated by steadily working to reduce your overall debt level.

On the other hand, if your overall debt load stays the same or continues to increase after you take out a personal loan, that could hurt your credit score because it shows lenders that you are getting deeper into debt and not managing your credit well.

Recent Missed Payments Will Be Penalized More Heavily

Payment history has always been the most important part of a FICO credit score, but it is even more important with FICO 10 T, the trended data score.

Using historical data, it can assign late and missed payments even more weight based on your behavior in the past 24 months. For example, if you’ve been getting progressively farther behind on payments over time, the negative impact on your credit score could be even greater than it would with a previous FICO score.

If you have delinquencies that are at least a year old, though, then those older negative marks on your credit report won’t hurt your score as much, according to MSN.

How Will the FICO 10 Scoring Model Affect Credit Scores?

Overall, it is predicted that the new FICO 10 scoring models will have a polarizing effect on consumers’ credit scores, which means that some consumers who have bad credit scores may see them drop even further, while those who have good credit scores because they are on the right track may be rewarded with even higher scores.

40 million consumers are likely to experience a credit score drop of 20 or more points with FICO 10 compared to previous models. This could push some consumers over the edge into a lower credit rating category.

FICO has estimated that approximately 100 million consumers will probably experience minor changes of less than 20 points to their scores. The company also estimates that about 40 million consumers will see their credit scores drop by 20 or more points, while another 40 million could see their scores increase by the same amount.

You are likely to see a credit score drop if you took out a personal loan to consolidate debt but then kept accruing more debt instead of paying it off, or if you have credit card debt that you are not paying down.

You are most likely to see a credit score increase if you have been penalized for having high balances from time to time, since the temporal data from FICO 10 T will help to average out the peaks in your utilization rate.

While a decrease of 20 points in your credit score isn’t catastrophic, it could be enough to make a difference in your chances of being approved for credit or the interest rates you could qualify for. This is especially true for those whose credit scores sit near the lower border of a credit score category.

For example, if someone with a credit score of 595 with FICO 8 is considered to have fair credit. If FICO 10 gave them a credit score that is 20 points lower, their credit score would be 575, which is considered bad credit. That could very well make or break your chances of getting approved for a loan or a credit card.

On the other hand, the inverse is true for those who stand to gain 20 points. If a 20 point increase pushes a consumer over the edge from fair credit to good credit, for example, this could certainly be beneficial when applying for credit.

It’s estimated that 80 million consumers will see a significant change in their credit scores with FICO 10, which may move them into different credit score ranges.

Less Severe Score Fluctuations

As you may recall from How to Choose a Tradeline, the more data there is contributing to an average, the more difficult it is to affect that average.

Since FICO 10 T looks at your credit utilization for an extended period of time instead of just the current month, it is likely that your credit score will not change as drastically from month to month based on your utilization ratios at the time.

In other words, your utilization data from the past 24 to 30 months will have a stabilizing effect on your score that will protect it from being heavily penalized if you occasionally have high balances. For example, if you spend extra on your credit cards in December to prepare for the holidays, your score that month won’t be hurt as much as it would without the trended data (as long as you pay it off quickly).

Greater Emphasis on Trends and Recent Data

FICO 10 T will especially reward consumers who have a trend of improving their credit over time.

The inclusion of trended data with FICO Score 10 T and extra emphasis on recent data means that your credit score is not based solely on what your accounts look like today, but instead, it will give more importance to whether your credit is getting better or getting worse.

Hypothetically, it’s possible that two consumers with the same amount of debt and derogatory items could have different credit scores based on the trend in their debt levels.

If one consumer has $10,000 of credit card debt, but they have been making progress on paying that down from a starting point of $20,000 of debt, then their credit score would be helped by FICO 10 T because their debt level is demonstrating a trend of improvement over time.

If the other consumer also has $10,000 of credit card debt, but they used to only have $1,000 of revolving debt, that trend shows that they are getting deeper into debt, and their FICO 10 score would be hurt by that pattern of increasing debt.

A Polarizing Effect on Credit Scores

One of the major effects of FICO 10 is that it is likely going to polarize the pool of consumers’ credit scores. In other words, those near the top of the credit score range will get even higher, while those with low credit scores will sink even lower along the scale.

According to CNBC, consumers with scores of lower than 600 will experience the largest reductions in their credit scores with FICO 10. Those with scores of 670 and above could possibly gain up to 20 points.

This creates a distribution of credit scores that is more concentrated at the two extremes, as opposed to most consumers’ credit scores being concentrated around the average.

Unfortunately, that means the negative effects of the new FICO scores will disproportionately impact consumers who are already struggling with debt. This will make it even harder for consumers to get out of debt and may force them to seek out costly, predatory loans, which only accelerates the downward spiral of debt.