Myths about credit, unfortunately, are extremely common, even among people who purport to repair credit. We’ve previously compiled a list of common credit myths, which you can find in our Knowledge Center.

In this post, we’re going to focus on the top three credit myths that just won’t seem to go away, according to credit expert John Ulzheimer in a Credit Countdown video on the topic. Check out the video version at the end of this post.

Myth 1: Your revolving utilization ratio is worth 30% of your credit score.

While the general category of how much debt you owe does contribute 30% of your FICO score, the specific metrics regarding revolving utilization are just part of that category, not the whole thing. There are several other metrics included in this category, which FICO lists on their website. These include:

The total amount you owe on all of your credit accounts.

The amounts you owe on different types of accounts, such as installment loans and credit cards.

The number of your accounts that have balances on them.

The ratio of how much you still owe on your installment accounts, such as auto loans and student loans.

Therefore, your revolving utilization must necessarily be worth less than 30% of your credit score, although it is true that it is a highly valuable metric.

Myth 2: Closing an old credit card means the age of the card no longer counts toward your credit score.

Prominent sources in the credit arena often advise consumers not to close their oldest credit cards, claiming that this will cause consumers to lose the benefit of the card’s age. In theory, this idea makes sense because your credit age is worth 15% of your credit score and it is directly connected to your payment history, which is worth an additional 35% of your score.

However, the problem with this advice is that you actually do not lose the age of a credit card once you close the account. In fact, according to John, credit cards continue to increase in age and contribute to your average age of accounts even after they have been closed.

Still, it is important to remember that closing a credit card is not completely free of consequence. When you close a credit card account, you no longer get the benefit of the unused credit limit that was associated with the account, which was likely helping your credit score.

Myth 3: Employers can check your credit scores.

In truth, this myth likely exists because employers can check your credit reports, but credit reports and credit scores are not the same thing. Your credit report contains information about your credit accounts, while your credit score is a three-digit number that represents how creditworthy you are deemed to be by the credit scoring model.

Furthermore, the credit reports that employers receive are different from the versions that are provided to lenders, and these credit reports do not come with credit scores.

If there are other credit myths you think we should cover, leave a comment on this article or the accompanying video on our YouTube channel!

Some folks in the field of credit repair claim that hard inquiries can be “bumped” or “chopped” off of your credit report through the processes of inquiry “bumpage” and “choppage.”

What do these terms mean, and do they actually work?

Credit expert John Ulzheimer, who has worked in the credit industry for 30 years, gave us his take on this trend in a Credit Countdown video on our YouTube Channel. We’ve outlined the main points of the video for you in the article below.

How Much Do Inquiries Impact Your Credit Score in the First Place?

Credit scores factor in five categories of information when calculating your score, and they are not all given equal weight.

The most important piece of the credit score pie chart is your payment history, or in other words, your track record of making your payments on time. This factor accounts for 35% of your FICO credit score.

The next largest piece is how much debt you owe, which relies heavily on your revolving utilization metrics, among other factors. Your debt comprises 30% of your credit score.

Your length of credit history, AKA your credit age, represents 15% of your score, while credit mix, or your diversity of types of credit accounts, makes up 10%.

Finally, the last 10% of your credit score comes down to the new credit category, which includes hard inquiries.

For this reason, focusing on trying to remove inquiries from your credit report usually does not make sense as a credit improvement strategy. Even if you are 100% successful in removing all of the hard inquiries that may be bringing down your credit score, you will only move the needle a small amount relative to what you could accomplish by focusing on the more important credit score factors.

What Is Inquiry Bumpage?

The concept behind credit inquiry “bumpage” is the idea that the credit bureaus only have a certain amount of space allocated for each consumer’s credit report. Therefore, the theory goes, if you can fill that limited amount of space with new information, you can “bump” the oldest inquiries off of your credit report.

What Is Inquiry Choppage?

Inquiry “choppage” is theoretically what happens when the soft inquiries get “chopped” or removed from your credit report before the hard inquiries can be “bumped” off.

Do Inquiry Bumpage and Choppage Really Work?

According to John Ulzheimer, aside from the speculation and marketing tactics you may see in credit repair space online, there is no reason to believe that bumpage and choppage even happen in the first place, let alone that they are effective strategies to help get hard inquiries removed from your credit report.

Better Ways to Increase Your Credit Score

While the methods of bumpage and choppage are not recommended when trying to improve your credit, fortunately, there are more legitimate and effective things you can try.

Remove inaccurate derogatory information. If there is damaging information on your credit report that is not supposed to be there, filing a dispute to get it removed or corrected should be your top priority.

Pay your bills on time. Since your payment history has the greatest amount of influence on your credit score, getting more on-time payments onto your credit report will go a long way toward attaining a higher credit score.

Maintain low balances on your credit cards. Factors having to do with the amount of debt you owe also play a sizeable role in determining your credit score, and your credit card utilization ratios are the key metrics in this category. The lower your credit card balances are, the higher your credit score can climb.

Limit the number of accounts that have balances on your credit report. In addition to utilization ratios, credit scoring models also consider how many of your accounts have balances on them. Even if the balances are small, if you have too many accounts with balances, this can bring down your credit score.

Increase your credit age. All you have to do to increase your credit age is wait patiently for your accounts to get older!

Plus, try some of the other credit tips we’ve published in our Knowledge Center, such as our list of easy credit hacks that will actually get you results.

The NFCC often receives readers questions asking us what they should do in their money situation. We pick some to share that others could be asking themselves and hope to help many in sharing these answers. If you have a question, please submit it on our Ask an Expert page here.

This week’s question: I took on too much debt and went without a job for 23 months. I am now employed and currently paying off my last, charged-off credit card. Should I open a new line of credit or just continue to pay my debt to rebuild my credit?

Getting back on your feet after a period of unemployment and high debt is a huge accomplishment. Rebuilding your credit depends on multiple factors and on where you stand with your overall credit and finances. So, in your situation, I recommend doing it all: pay all your bills on time, continue to pay down your debt, and rebuild your credit health with positive account activity and a new line of credit.

As you work to improve your credit, you should know which factors influence your score and learn how to use them to benefit your score. These factors include paying your bills on time, keeping your utilization ratio low, how often you get new credit, the types of credit you have, and for how long you’ve had credit.

Ways to Improve Your Credit

Arguably, the most important thing you can do for your credit is always paying your bills on time. This should become second nature so that you build your credit now and maintain a good score in the future. Then, if you don’t have an active account on your credit files, you could apply for a new credit card in order to generate a positive credit history on your credit reports. One sure way to open a new account is to apply for a secured credit card. Secured credit cards are offered by many banks and have a variety of perks and fees. Apart from looking and acting like any other type of credit card account, the primary differences are that you are approved without a credit check and you need to send a security deposit when you open the account. This deposit typically becomes collateral that establishes your credit limit and it’s returned to you if you close the account or if your account is upgraded to an unsecured credit card.

Be Strategic

Once you have your credit card, use it strategically. This means paying on time and keeping your utilization ratio below 30%. Your utilization ratio is how much of your available credit you are using. So, when you have high credit card debt, you appear at risk of losing control of your financial stability, which brings your score down. That’s why you should continue to pay off your debt in order to reduce your utilization ratio.

The other factors—the age of your credit, the types of credit you have, and how often you use your credit—are also important to a lesser degree. How old your credit is only will improve with time, so be patient. The mix of credit looks at the type of credit you have—credit cards and loans. But, right now, let’s focus on the primary factors. And last but not least, that’s how often you apply for new credit. When you ask for a new credit line, a hard inquiry is generated, and it remains on your report for 24 months. Too many inquiries bring down your score. So, you must be selective and strategic about getting new credit lines.

As you can see, building your score comes down to being strategic about how you use your credit in every transaction. When you have the tools and the right plan to improve how you manage your credit, it becomes easier to make financial decisions that build a stronger credit rating. If you need help with more personalized strategies to work on your credit, you can reach out to an NFCC Certified Financial Counselor.

When purchasing tradelines, there are some cases where it is best to get a single tradeline and other cases when multiple tradelines might be more appropriate. To help you decide, we’ve provided some examples for each scenario below.

When to Buy Two or More Tradelines

Thin Credit File (Too Few Accounts)

Balance out derogatory accounts with positive tradelines.

Credit scoring models value a mix of several different types of credit accounts, so a thin file with only a few accounts might be limited in what it can achieve. In this case, adding a few tradelines would be ideal because it would help increase the number of accounts in the file.

On the other hand, someone with no credit at all or an extremely thin file can also experience significant benefits from adding one tradeline, since they didn’t have much there to begin with. Of course, more than one tradeline will help even more.

Balancing Out Derogatory Accounts

Accounts that have negative marks such as late payments and collections can really drag down credit. Derogatory accounts need to be outweighed by positive accounts, so one’s credit report should contain at least 2-3 positive tradelines for every negative account. Therefore, multiple tradelines may be necessary to balance out derogatory accounts damaging one’s credit.

Maximizing Results

For those looking to get maximum results, buying several of our best tradelines would be the ideal plan. This becomes increasingly important for people who already have good credit (680 FICO or higher) because it is much more difficult to significantly impact one’s credit report with a file that is already relatively strong.

There is also a point of diminishing returns on tradelines for those with already high credit scores, so situations like this require purchasing the absolute best quality tradelines in order to achieve positive results.

In other instances, the goal may be extremely important and the risks of failing to meet that goal may be significant. In situations where the outcome is very important, we recommend using the maximum strength possible.

Of course, the risk is that there are no guarantees on what the results will be, but at least you can be sure that you received the maximum benefit possible from tradelines. The rest is up to you.

Posting to a Specific Credit Bureau

In time-critical situations, purchasing additional tradelines will help protect against potential non-postings.

If it is important for a tradeline to post to a specific credit bureau, this is a good time to consider purchasing more than one tradeline.

Unfortunately, banks and credit card companies are not always 100% accurate in their reporting process, so while we guarantee that each tradeline will post to at least any two out of the three major credit bureaus, we do not have any control over which of the three bureaus the tradelines will post to.

Because there is always a degree of uncertainty with tradelines, if you are looking to get a tradeline to post to a specific bureau, purchasing extra tradelines will help provide the added security you need.

Important Time-Sensitive Events

Similarly, if something important and time-sensitive is going on that depends on the tradelines posting, the safest bet is to get more than one tradeline. Again, we do offer a money-back guarantee in the event that a non-posting occurs, but the fact is that non-postings do occasionally happen due to inconsistent reporting by the banks.

In time-critical situations, there may not be time to exchange a non-posting tradeline for a new one and wait for the new one to post. If you are counting on tradelines to post within a certain time frame, investing in additional tradelines will help hedge against potential non-postings.

When to Buy One High-Quality Tradeline

It’s usually best to purchase one high-quality tradeline if there are budget constraints.

Budget Constraints

If your budget is constrained to a certain dollar amount, it is usually better to purchase one high-quality tradeline rather than dividing that amount between two tradelines that are not as high in quality.

This is because credit scores consider both your average age of accounts and the age of your oldest account. A single account with lots of age has more potential to increase those numbers, while two accounts with less age may not offer as much improvement or might even dilute the credit file.

Here is a hypothetical example to consider. Let’s say your current average age of accounts is 2 years. If you were to spend the same amount of money in either case, would it be better to buy two tradelines that are both 4 years old, or one tradeline that is 8 years old?

If you decided to buy the two 4-year-old tradelines, this would increase your average age of accounts to about 3 years ([2 + 4 + 4] / 3 = 3.3) and your oldest account would be 4 years old.

On the other hand, if you were to buy one 8-year-old tradeline, this would bump up your average age of accounts to 5 years ([2 + 8] / 2 = 5) and your oldest account would be 8 years old.

In the second scenario, you end up with a higher age for both of these important credit history factors. Be sure to check out our tradeline buyer’s guide and tradeline calculator to help determine the best plan of action for your situation.

Current credit file

After adding 2 4-year-old tradelines

After adding 1 8-year-old tradeline

Average age of accounts

2 years

3 years

5 years

Age of oldest account

2 years

4 years

8 years

It is more difficult to affect the average age of accounts when there are many accounts, so one high-quality tradeline tends to be the best choice for very thick files.

Extending the Age of Your Oldest Tradeline

The age of the oldest account in your credit file is a very important data point. If the goal is simply to extend the age of the oldest tradeline in the credit report, then of course only one tradeline is needed. The tradeline just needs to be older than the oldest account that is currently on file, but obviously, the more age the better, so we recommend going significantly older.

Very Thick File (15 or More Accounts)

A very thick file with a large number of accounts will “dilute” the power of any tradelines that are added. Since there are so many tradelines already in the file, it will be more difficult to affect the average age of accounts. Therefore, one premium tradeline with a lot of age and a high credit limit will be a better fit for a very thick file, rather than multiple less potent tradelines.

Focusing on Credit Limit

Some consumers are less concerned with the age of the tradelines and more concerned with the credit limit for their specific circumstances. If a high credit limit is the main priority, it will usually make more sense to purchase one tradeline with a high credit limit rather than multiple tradelines that have lower credit limits.

If a high credit limit is the goal, usually one tradeline is enough.

The strategy on this topic may vary depending on what you are trying to accomplish and what your goals are, but in general, if you can accomplish the goal with one tradeline, that would probably be the better option.

Modest Goals

Depending on what a person’s goals are, they may not need to get the maximum results possible. For smaller goals, one tradeline may be all they need. However, it is always best to try to overshoot the goal in order to have some extra insurance in making sure the goal is truly achieved.

No Credit File or an Extremely Thin File

As we mentioned previously, adding a few tradelines to a thin credit file is ideal because it greatly increases the number of accounts in the file.

Adding just one tradeline to a very thin credit file can make a big difference.

However, it’s also important to keep in mind that someone with no prior credit history or an extremely thin file may still find value in buying just one tradeline, since adding one account to a baseline of zero or one existing accounts is still a significant change.

As an example, adding one tradeline to a credit report that previously only had one account in it represents a 100% increase in the number of accounts in the file! This not only adds valuable age and payment history but also impacts the “credit mix” factor in credit scoring.

Key Takeaways on How Many Tradelines to Buy

To summarize when you should consider purchasing a single tradeline versus when you should consider investing in more than one tradeline, we have included the main points of this article in the table below.

When to Buy Two or More Tradelines

When to Buy One High-Quality Tradeline

If you have a thin credit file (too few accounts)

If you have budget constraints

If you need to balance out derogatory accounts

When you want to increase the age of your oldest tradeline

When you want to maximize results

If you already have a very thick file (15 or more accounts)

When you need a tradeline to post to a specific credit bureau

If you want a high credit limit

If you need a tradeline for an important, time-sensitive event

If you have modest goals

If you have no credit file or an extremely thin credit file

If you are wondering how many tradelines you need, remember that the power of tradelines is always going to be relative to your current credit file and it is important to consider what will be the best fit for your specific situation.

In some situations, it may be important to maximize results using multiple powerful tradelines, such as when you are trying to accomplish a major goal or when there are serious hurdles to overcome. In other cases, one good tradeline might be all you need.

Whatever the case may be for you, it is always best to understand how tradelines work first and foremost and avoid making any common mistakes.

In simplest terms, the safest option is always to overshoot your goal and stick with the highest quality tradelines within your budget, and remember that in most cases, age is key. If budget is a big concern, then it’s usually best to just buy one of the highest quality tradelines your budget allows.

What are your thoughts on this article about how many tradelines to buy? We would love to hear your feedback, so leave a comment below!

Using a credit card is easy — you use the card to buy things and then pay the credit card bill.

A credit card can sometimes be difficult, however, when dealing with your credit file.

From a missed payment to a loan that isn’t yours that’s incorrectly listed on your credit report, there are all kinds of ways your credit score can drop.

And not all of them are from something you did wrong.

What Is the Fair Credit Reporting Act?

Consumers have protections under the law regarding their credit reports — which is where credit scores and credit problems are listed for lenders to check before offering you credit.

Errors on a credit report can drop your credit score, making it harder to get a loan, credit card, rent an apartment, or qualify for insurance coverage, among other things.

The main law that protects consumers from credit errors is the Fair Credit Reporting Act, or FCRA.

Your Rights Under The FCRA

Here are some of the rights you have under this law and how to use it to protect your credit:

View Credit Reports

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months.

You can do one check every four months from each of the three — Equifax, Experian, and TransUnion — if you really want to be on top of it.

Start by going to AnnualCreditReport.com to request your credit file online.

Only use that website and don’t use a copycat site that charges fees for what should be a free service.

You’ll need to verify your identity to get online access. You can also request your credit file through an automated phone system or the mail.

The FCRA applies to all consumer reporting agencies.

You can also look at reports from other consumer reporting agencies that collect noncredit information about you.

These include rent payments, insurance claims, employers, and utility companies.

The Consumer Financial Protection Bureau lists the reporting companies and how to request a free report from each.

DISPUTING ERRORS

Getting a credit report in your hands can lead to all sorts of eye-opening concerns. Anything that’s listed as negative should be checked for accuracy. Here are some things to look out for:

Eviction that wasn’t legal.

Creditor listed that you didn’t have an account with.

Loan default.

Wrong name.

Wrong address.

Wrong Social Security Number.

Incorrect loan balance.

Closed account reported as open.

A loan you didn’t initiate.

Some errors may be simple to resolve and others you may need to do more research on before disputing them to ensure they’re incorrect.

For example, you may not recognize the name of a creditor and assume you don’t have an account with them. But it may just be a store credit card you recently applied for that is listed by the issuing bank’s name. Or maybe a home or auto loan was sold to a new loan servicer.

Other errors could be reason to suspect identity theft, or there could just be wrong information that’s bringing down your credit score.

If you suspect identity theft, such as someone taking out a credit card in your name, then file a police report and report it to your credit card company and the credit reporting agencies.

To dispute erroneous information, use certified mail to send the credit bureau a letter and copies of documents explaining the error. If a loan still shows an outstanding balance and you have written proof that it was paid off, for example, send a copy to the credit agency.

Credit agencies have 30 days to investigate and respond to your dispute, unless they deem it frivolous.

If it corrects an error, it must send you a free copy of your credit report through AnnualCreditReport.com so you can see that the corrections have been made.

Check Your Credit Score

The law allows you to request a credit score, though it’s legal for credit agencies and other businesses to charge you a fee for this service.

Some credit cards provide scores for free, so check with your credit card issuer first.

A credit score isn’t the same as a credit report.

Information in a credit report determines a credit score, and each credit bureau can use a different scoring model that requires it to provide different information.

You have different credit scores, depending on which factors are weighed more heavily.

Monitoring your credit is vital. Make sure that you review your credit report for any inaccuracies.

Know Who Can View Your Credit Report

The FCRA doesn’t allow a credit reporting agency to share your credit file with someone who doesn’t have a valid need.

Some inquiries, such as from a potential employer or landlord, require your written consent.

And, they can only check your credit report, not your credit score.

The credit reporting agencies can share your credit report for legitimate reasons, such as when you’re applying for credit, insurance, housing, or with a current creditor.

A Time Limit To Negative Information

The FCRA doesn’t allow credit bureaus to report negative information that’s more than seven years old, though it allows some forms of bankruptcy to remain on a credit report for 10 years.

There’s also a time limit for positive credit information such as on-time payments and low balances — up to 10 years after the last date of activity on the account.

Rejections Based on Credit Report

If your application for credit, job, insurance, or housing has been denied because of information in your credit report, the law gives you the right to know this information.

The landlord, employer or other entity that denied your application must notify you and give you the name, address and phone number of the credit reporting agency that provided the information.

The FCRA allows you to get a free copy of your credit report from that reporting agency within 60 days of the action against you. That’s in addition to the three free credit reports allowed annually.

To best deal with a potential rejection ahead of time, it’s smart to check your credit report before applying for credit, rental unit or related use of your credit report and check it for errors. Give yourself enough time to fix them.

The NFCC often receives readers questions asking us what they should do in their money situation. We pick some to share that others could be asking themselves and hope to help many in sharing these answers. If you have a question, please submit it on our Ask an Expert page here.

This week’s question: I need some advice in regards to my credit report and good ways that I can begin to build up my credit. I have no credit at all. Eventually within five years once I’m out of school I want to buy a house.

Building credit from scratch will take some time and effort, just like getting a job after graduating from school. You can think about good credit as a means to an end: you need good credit to finance big purchases and get the best interest rates and repayment terms on loans and mortgages. So, getting your credit ready is an excellent start to buying a home in the near future.

What is on Your Credit Report?

Your credit is a record of your monthly financial credit transactions. Your creditors report your activity to the three credit bureaus, Equifax, Experian, and TransUnion, and they use that data to generate a credit score. Your credit report also includes your personally identifying information such as your name, addresses, social security, and some public records such as bankruptcies and judgments and tax liens, if you have any. To start generating data for your credit report, you need to get a credit line. The easiest way to do that is to get a secured credit card. Many banking institutions issue secured credit cards, and they work pretty much like a regular credit card. The main difference is that these cards are backed by a cash deposit, which usually corresponds to the card’s credit limit.

Be Strategic

Learning how to use your credit card strategically is equally as important as getting that credit line. Your credit score takes into consideration several factors. The factor that influences your score the most is whether you pay your accounts on time and as agreed. Late or insufficient payments are very detrimental to your credit history. So, you should plan to pay in full and before your due date. Another important factor is your utilization ratio, which is how much you owe compared to your available credit. To have a balanced ratio, experts recommend that you use only 30% or less of your available credit in every billing cycle. For instance, if you have a $500 credit limit, you should be using less than $150.

Yet another factor is the age of your credit history. The older your credit history, the more history and data you’ll have to establish a solid credit history. Achieving this will just require time and your continued effort. The other two factors to keep in mind are the mix of credit you have (credit cards and loans) and how often you ask for new credit. Too many new credit inquiries reflect negatively on your score, so it’s important that you only apply for new credit sporadically. In your case, you should keep your secured credit card for at least a year before applying for a regular credit card. In some cases, your creditor may even upgrade your secured credit card to a regular one and return your cash deposit.

It’s never too soon to start building your credit. And once you learn healthy credit management habits, it will be very easy for you to manage your credit and use your credit cards responsibly on a daily basis. If you feel you need additional guidance or personalized help to get you started, you can always reach out to an NFCC Certified Financial Counselor. They are ready to help over the phone, online, and in-person if it’s available in your state. Good luck!

The vast majority of lenders use your FICO credit score to evaluate your credit risk as a consumer when they are deciding whether or not to extend credit to you. And yet, historically, it has been costly for consumers to access their own FICO scores.

Popular websites such as Credit Karma and Credit Sesame offer free credit scores, but the scores provided are usually VantageScores, not FICO credit scores.

Knowing your VantageScore is still valuable information, but it is not directly tied to your FICO Score, so it is less useful when it comes to preparing to apply for credit. While it is often true that a consumer’s FICO score is similar to their VantageScore, in some cases, they may be vastly different, especially depending on which credit scoring models are used and which credit bureaus are providing the credit report information.

If you need to check your FICO score, where can you do so without paying a fee to access it?

Here are some of the best places to get your FICO score for free.

Your Credit Card Issuer

Several major credit card issuers now offer consumers the ability to check their FICO scores for free.

Discover Bank

Discover offers a free way to check your FICO score with their Credit Scorecard program. Even consumers who do not have a relationship with Discover Bank can freely use this feature.

Experian provides the credit report data that is used to calculate your FICO score. Your credit score updates once every 30 days and Discover notifies you when it is time to check your new FICO score.

In addition, Discover’s FICO Credit Scorecard keeps track of your credit score history so you can see how it changes from month to month.

The Credit Scorecard also provides a summary of what is going on with each of the five credit score factors that are influencing your FICO score: your payment history, credit utilization, length of credit history, mix of credit, and new credit (e.g. inquiries). You can find educational information about credit scores on the website as well.

To access your FICO score with Discover’s FICO Credit Scorecard, either visit their website or use the bank’s mobile app.

Bank of America

Bank of America is another widely used bank that offers free FICO scores to consumers. However, to enroll in this program, you must be a Bank of America credit card customer.

Much like Discover’s offering that we described above, Bank of America’s FICO Score Program provides customers not only with their FICO scores but also information on the major factors that influence your credit score, your month-to-month credit score history, and education about how to achieve and maintain good credit.

On top of this, Bank of America also compares your credit score to the national average.

Bank of America customers can view their FICO score for free on the company’s website or mobile app.

Citibank

Consumers who have Citibank branded credit cards can obtain their FICO score for free from Citi.

Citi states on their website, “We think it’s important to provide our cardmembers with free access to information that will help them understand and stay on top of their credit status. That’s why we’re providing you with your FICO® Score and information to help you understand it.”

Your FICO score from Citibank is determined using information from your Equifax credit report and the FICO Bankcard Score 8 credit scoring model. Unlike the standard version of FICO 8 that you may be used to seeing, which ranges from 300 to 850, the bank card model used by Citi ranges from 250 to 900. It is updated once a month.

You can find more information on Citi’s free FICO score program on their website.

American Express

Recently, American Express started providing access to free FICO scores to consumers who have American Express credit cards.

The bank uses the standard version of FICO 8, so the credit score range spans from 300 to 850. Experian provides the credit report data used to calculate your score.

As with the other free FICO score programs, you also get to see how your FICO score changes over time and you receive a summary of the factors affecting your credit score.

American Express credit cardholders can see their FICO scores in their online account or on their monthly statement.

Those who do not have credit cards with American Express can get their TransUnion VantageScore for free through the company’s MyCredit Guide program, but this does not include FICO scores.

Barclays

FICO scores from TransUnion are available to all Barclays credit card customers through the bank’s online banking system.

Once you have had your Barclays card for three months, you can see a chart of your FICO score history over the time you have had an account open with Barclays, according to SmartAsset.

Plus, Barclays will send you alerts via email if your credit score changes, including an explanation of why your score has changed.

Wells Fargo

Wells Fargo account holders who use their online banking platform can view their FICO credit score within their online account.

Additional features include your credit score history, information on your credit score factors, and personalized credit tips from Wells Fargo.

According to the bank, they offer your FICO score for free in order to “support your awareness and understanding of FICO® Credit Scores and how they may influence the credit that’s available to you.”

The FICO score you get through Wells Fargo is calculated using Experian credit report data and is updated once a month.

Experian

Experian is the only major credit bureau that offers consumers their FICO 8 scores for free along with their Experian credit reports.

In addition, Experian offers an alternative credit data program called Experian Boost, which can add positive payment history from certain bills to your credit report, such as utilities and Netflix.

Sign up on Experian’s website to start using these free services.

Your Local Bank or Credit Union

Not all banks and credit unions offer customers the ability to check their FICO scores for free, but it is worth asking if you do not have access to the previous options. If your local bank or credit union does not offer free FICO scores, they may be able to help direct you toward somewhere that does.

Will Checking Your FICO Score Hurt Your Credit Score?

Although this is a common concern, checking your own credit score should never hurt your credit.

This credit myth likely arises from the fact that hard inquiries on your credit report can have a small negative effect on your score.

However, hard credit inquiries only happen when you are actively seeking credit and a lender has to pull your credit report to decide whether or not to loan you money.

All other credit checks, including those you conduct yourself for educational purposes, are considered to be soft inquiries, which do not affect your score at all.

Final Thoughts on How to Get Your FICO Score for Free

If you want to be able to see your FICO score for free, there are many options available to you, especially if you have credit card accounts with major banks such as those listed above.

FICO also has a program called FICO Score Open Access that aims to enhance consumer access to FICO scores and educate consumers about the topic. FICO has a list of additional lenders and credit and financial counseling organizations that participate in this program, which you can browse in case you do not have any accounts with the banks mentioned here.

Keep in mind that lenders use many different versions of FICO scores, including older generations and versions that are specific to certain industries. That means that when you check your FICO score for free, it is not guaranteed to be the same exact FICO score that a lender will use when you apply for credit.

When you check your FICO score using one or more of the methods in this article, take note of which credit bureau is supplying the information as well as which FICO score version is being used to calculate the result so that there is no confusion if you see a different FICO score somewhere else.

Finally, remember that you can also get your VantageScore for free in many places as well. While it’s not the same as your FICO score, it can still provide educational value as it uses the same general principles to calculate your score.

Let us know if this article helped you find a way to get your FICO score for free by commenting below!

Credit cards are not only a useful payment method for making purchases but also an essential component of a solid credit-building strategy.

After all, credit cards are the most common form of revolving credit, which is given more importance than installment credit (e.g. auto loans, student loans, mortgages, etc.) when it comes to calculating your credit score.

Unfortunately, credit cards often get a bad rap because it’s easy to rack up excessive amounts of debt and destroy your credit score if you do not know how to use credit cards properly.

However, when you have the knowledge and ability to use credit cards to your advantage rather than to your detriment, they can be an extremely powerful financial tool to have in your arsenal.

If you’re unsure if using credit cards is the right choice for you or confused about how they work, then keep reading to learn the basics of credit cards that everyone should know.

What Is a Credit Card?

A credit card is a card issued by a lender that allows a consumer to borrow money from the lender in order to pay for purchases.

The consumer must later pay back the funds in addition to any applicable interest charges or other fees.

They can choose to either pay back the full amount borrowed by the due date, in which case no interest will be charged, or they can pay off the debt over a longer period of time, in which case interest will generally accrue on the unpaid balance.

Each credit card has an account number, a security code, and an expiration date, as well as a magnetic stripe, a signature panel, and a hologram. Most credit cards also now have a chip to be inserted into a chip reader rather than swiping the card at the point of sale. In addition, some credit cards offer contactless payment capability.

Credit cards allow consumers to pay for goods and services with funds borrowed from the credit card issuer.

How Do Credit Cards Work?

Although using credit cards may feel like using “fake money” or spending someone else’s money, it’s important to understand that the money you borrow when you pay with a credit card is very much real money that you now owe to the lender.

Credit Cards Are Unsecured Revolving Debt

With most credit cards, the funds you borrow are considered to be unsecured debt because you are borrowing the money without any collateral. That means the credit card issuer is taking on additional risk by giving you a credit card, since there is no collateral that they can take from you if you fail to pay back the debt, unlike with secured debt, such as a mortgage or a car loan.

Furthermore, the lender allows you to decide when and how much you want to pay back the funds instead of requiring you to pay the full balance on each due date. You can choose to only pay the minimum payment and “revolve” the remaining balance from month to month, which extends the amount of time during which you owe money to the credit card company.

Most credit cards now come with a chip in addition to a magnetic stripe.

For the above reasons, credit card interest rates are typically significantly higher than the interest rates for installment loans.

However, credit cards are also the only form of credit where paying interest is optional—there is a “grace period” of at least 21 days before the interest rate for new purchases takes effect, and you only get charged interest if you do not pay back your full statement balance by the due date.

(Keep in mind that the grace period usually only applies to new purchases, as stated by The Balance. This does not include balance transfers or cash advances, which typically begin accruing interest immediately.)

Understanding Credit Card Interest Rates

To reiterate, the interest rate of a credit card technically only applies when you carry a balance instead of paying off your full statement balance each month. However, most people will likely end up carrying a balance on one or more credit cards at some point, so it is still a good idea to be aware of what your interest rates are.

APR and ADPR

The interest rate of a credit card is usually expressed as an annual percentage rate (APR). This is the percentage that you would pay in interest over a year, which can be confusing because interest on credit card purchases is charged on a daily basis when you carry a balance from month to month.

You can find your average daily periodic rate (ADPR), which is the interest rate that you are being charged each day, by dividing the APR of your card by 365.

Average Credit Card Interest Rates

The interest rate of a credit card, expressed as the APR, is important to know if you ever carry a balance on the card.

As of October 2020, the average credit card interest rate as reported by The Balance is 20.23%. However, credit card issuers are allowed to set their APRs as high as 29.99%. It is not uncommon to see APRs upwards of 20%, even for consumers who have good credit.

The highest interest rates are generally seen on credit cards for bad credit or penalty rates that credit card issuers can implement when you are 30 or more days late to make a payment. You may also get penalized with a higher interest rate if you go over your credit limit or default on a different account with the same bank, according to ValuePenguin.

Ask for a Lower Interest Rate

In our article on easy credit hacks that actually work, we suggest trying the simple tactic of calling your credit card issuer’s customer service department and asking for a lower APR. Surveys have shown that a majority of consumers who do this are successful in obtaining a lower interest rate.

Important Dates to Know

Many consumers assume that the payment due date of your credit card is the only important date you need to worry about. While it’s true that the due date is the most important date to be aware of, there are several other dates that are useful to pay attention to as well.

Billing cycle

The billing cycle of a credit card is the length of time that passes between one billing statement and the next. All of the purchases you make within one billing cycle are grouped together in the following billing statement.

This cycle is typically around 30 days long, or approximately monthly, although credit card companies can choose to use a different billing cycle system.

Statement closing date

Your credit card’s statement closing date is not the same thing as your due date, so make sure you know both.

Sometimes referred to simply as the “closing date,” this is the final day of your billing cycle. Once a billing cycle closes and the statement for that cycle is generated, the balance of your account at that time is then reported to the credit bureaus.

You can look at your billing statement to find the closing date for your account. Because of the 21-day grace period, the statement closing date is usually around 21 days before your due date.

Due Date

This is the most important date to know in order to pay your bill on time every month, which is the most influential factor when it comes to building a good credit history. To make it easy for yourself to avoid accidental missed payments, you may want to set up automatic bill payments.

If your due date is inconvenient due to the timing of your income and other bills, you can try requesting a different due date with your credit card issuer.

Promotional offer dates

Many credit cards offer introductory promotions to attract new customers, such as 0% APR, bonus rewards, or no balance transfer fees. To use these offers strategically, you will need to know when the promotional period ends so you can plan accordingly.

Expiration date

All credit cards have an expiration date past which they cannot be used.

Every credit card has an expiration date printed on it, after which you will no longer be able to use that card, although your account will still be open. You just have to get a new credit card sent to you to replace the one that is expiring.

Usually, credit card companies will automatically send you a new card before the original card expires. If this does not happen, simply call the issuer to ask for a replacement credit card.

A Common Credit Card Mistake

Some consumers think that the closing date and the due date are the same thing and therefore believe that if they pay off the full statement balance by the due date, the credit card will report as having a 0% utilization ratio. They may then be confused to find out that their credit card is still reporting a balance to the credit bureaus every month.

However, the statement closing date is usually not the same date as your due date. This is why your credit cards may report a balance every month even if you always pay your bill in full—the account balance is being recorded on your statement date before you have paid off the card.

If you do not want your credit card to report a balance to the credit bureaus, you will need to either pay off the balance early, prior to the statement closing date, or pay your statement balance on the due date as usual and then not make any more purchases with your card until the next closing date.

Credit Card Payments

With credit cards, you have several different options for payment amounts.

Minimum payment

If you only pay the minimum payments on your credit cards, it will take longer to pay off your credit card debt and you will be charged interest.

This is the minimum amount that you are required to pay by your due date in order to be considered current on the account and avoid late fees. Although this may vary between different credit card issuers, typically the minimum payment is calculated as a percentage of your balance.

If you make only the minimum payment every month, it will take you a much longer time to pay off your balance and you will be paying a far greater amount in interest than if you were to pay off your statement balance in full. Check your billing statement to see how the math works out; the credit card company is required to disclose how long it will take to pay off the balance if you only make the minimum payments.

Statement balance

This is the sum of all of your charges from the preceding billing cycle in addition to whatever balance may have already been on the card before that cycle. This is the amount you need to pay if you do not want to pay interest for carrying a balance.

Current balance

This number is the total balance currently on your credit card, including charges made during the billing cycle that you are currently in, so it will be higher than your statement balance if you have made more purchases or transfers since your last closing date. You can pay this amount if you want to completely pay off your account so that it has no balance.

Other amount

You can also make a payment in the amount of your choosing, as long as it is greater than the minimum payment. This is a good option to use if you don’t have enough cash to pay the statement balance in full, but want to pay more than the minimum in order to mitigate the amount of interest you will be charged.

Credit Card Fees

Credit cards often charge various other fees in addition to interest. Here are some common fees to be aware of.

Although you may have access to a “cash advance” credit limit on your credit cards, it is generally not recommended to get a cash advance due to the high interest rates and fees you will have to pay.

Late payment fees

If you do not make the required minimum payment before the due date, the credit card company will likely charge you a late fee somewhere in the range of $25 – $40 (in addition to potentially raising your APR to a penalty rate). If you usually pay on time but accidentally miss a payment for whatever reason, try calling your credit card issuer and asking if they would be willing to reverse the fee since you have been an upstanding customer overall.

Annual fees

Some credit cards charge an annual fee for keeping your account open. Many times this charge may be waived for your first year as a promotional offer to attract new customers. Cards with higher annual fees will often have additional perks and rewards, but there are also plenty of great options for rewards cards that do not charge annual fees.

Cash advance fees

Your credit cards may give you the option to borrow cash in the form of a cash advance. However, this is usually not advised because cash advance interest rates are often significantly higher than your regular interest rate for purchases. In addition, you will most likely be charged a cash advance fee when you first withdraw the money, whether a flat dollar amount of around $10 or a percentage of the amount you take out, such as 5%.

Foreign transaction fees

Some cards charge a fee to use your card to pay for things in other countries. These fees are typically around 3% of the purchase amount. However, there are many credit cards on the market that do not charge foreign transaction fees.

Be sure to check the terms of service of your credit cards for fees such as these so that you can avoid any unexpected charges.

How Credit Cards Affect Your Credit

Credit cards are one of the most impactful influences on your overall credit standing, and they play a role in multiple credit scoring factors.

Building Credit With Credit Cards

One of the major advantages of credit cards is that it allows you to start building a history of on-time payments, which is extremely important given that payment history is the biggest component of your FICO score, making up 35% of it.

All you have to do to get this benefit is use your credit card every so often and pay your bill on time every month.

Click on the infographic to see the full-sized version!

Revolving accounts such as credit cards can have a much greater influence on your credit than auto loans, student loans, and even a mortgage—for better or for worse. They must be managed properly because negative credit card accounts will also have a very strong impact on your credit.

Mix of Credit

Although your mix of credit only makes up 10% of your FICO score, it is still worth considering, especially if you aim to achieve a high credit score or even a perfect 850 credit score.

A good credit mix generally includes various types of accounts, including both revolving and installment accounts. You can see the different types of accounts in our credit mix infographic.

Credit cards may help with your credit mix if you have a thin file or if you primarily have installment loans on your credit report.

They also add to the number of accounts you have, which is a good thing for the average consumer. In fact, as we talked about in How to Get an 850 Credit Score, FICO has stated that those who have high FICO scores have an average of seven credit card accounts in their credit files, whether open or closed.

The Importance of Credit Utilization Ratios

Your credit utilization is the second most important piece of your credit score, which is another reason why credit cards are such a strong influence on your credit.

The basic rule of thumb with credit utilization ratios is to try to keep them as low as possible (both overall and individual utilization ratios), meaning you only use a small portion of your available credit. Ideally, it’s best to aim to stay under 20% or even 10% utilization, because the higher your utilization rate is, the more it will hurt your credit instead of help.

Conclusions on Credit Card Basics

Credit cards can be intimidating, especially when you don’t know how to use them correctly.

It is also true that not everyone wants or needs to use credit cards.

It’s not impossible to build credit without a credit card, but it is more difficult since you would be limited to primarily installment loans, which are not weighed as heavily as revolving accounts, and possibly alternative credit data.

However, for those who are able to use credit cards responsibly and follow good credit practices, they can be an incredibly useful credit-building tool as well as a way to reap some benefits and perks that other payment methods do not provide.

We hope this introductory guide to credit cards provides the knowledge base you need in order to feel confident using credit cards and to take advantage of their benefits.

If you found this article useful, please comment to let us know or share it with others who want to learn more about credit cards!

It’s never a good feeling when you notice that your credit score has dropped. You might feel confused or concerned, and you would probably wonder why your credit score took a dip. Let’s explore some of the possible reasons that could cause your credit score to decline.

Your average of accounts decreased because of a new account.

As we’ve written about many times in the articles in our Knowledge Center, the age of a tradeline is extremely important, as is your overall credit age. This is because credit age is linked to payment history, which is vitally important to your credit health.

Payment history makes up 35% of your credit score and credit age contributes 15% to your score. When you add the two together, you get 50%, which means that half of your credit score is controlled by these two connected factors.

Within the credit age category, your average age of accounts is thought to be one of the most important variables. The more age your tradelines have, the more they can benefit your credit. Therefore, anytime you decrease your average age of accounts, you run the risk of your score decreasing as a result.

So if you recently opened a new primary tradeline or if you were added as an authorized user to an account that lacks age, the decrease in your average age of accounts might be what’s behind your credit score troubles.

Your account balances increased.

Did you use credit to make a large purchase recently? Have you been accumulating more debt by not paying the full balance you charged each month? If either of these scenarios is true for you, that could explain why your credit score took a dive.

As your account balances increase, so does your credit utilization rate. This is bad news for your credit score since credit utilization contributes about 30% of your score.

If you’ve been using your credit card more often without paying it off entirely each month, that could be the source of the change in your credit score.

Low utilization is favorable since it indicates that you are not overextending yourself financially. On the other hand, high utilization shows that you are using a lot of your available credit, which means you are statistically more likely to default on a debt in the future. For this reason, high credit utilization is penalized by credit scoring models.

Fortunately, there are many strategies you can use to overcome the problem of high revolving credit utilization, such as pre-paying your credit card bill before your statement closing date, making more frequent payments throughout the month, increasing your credit limit, or getting a balance transfer card.

When you open a new account, it can hurt your credit score for a few reasons. The first and most important reason is that the account has no age, which means it is going to negatively affect your average age of accounts.

In addition, there was likely a hard inquiry on your credit report as a result of applying for the new loan. In “Are Inquiries Really Killing Your Credit? What You Need to Know,” each recent hard inquiry on your report may affect your credit score by up to five points.

The new account may also have a negative impact on the “new credit” portion of your credit score. Having new credit makes you look like a riskier borrower, which means it could slightly reduce your score.

However, new credit only makes up about 10% of your credit score, so the impact of opening one new account would likely be relatively small and it would diminish over time.

You applied for credit but your application was denied.

Applying for a loan or credit card, whether your application is approved or denied, the resulting hard inquiry could damage your credit score slightly.

As we just mentioned, when you apply for credit, the lender usually has to do a hard pull (AKA a hard inquiry) on your credit report to see if you qualify.

This doesn’t always result in a new credit account being opened. Sometimes, for example, your credit application might get rejected by the lender, or perhaps you may choose to decline the terms you were offered and not proceed with opening the account. (Note, however, that when you apply for a credit card, typically the account is automatically opened when you get approved for the card.)

Unfortunately, even if you didn’t actually end up opening a new account, the fact that you applied for credit can still hurt your score. The hard inquiry still goes on your credit report whether you opened an account with that lender or not.

If you only applied for one account, then your credit score will likely only fall by a few points, if at all. If you applied for several accounts that you didn’t open within the past year, however, it’s possible that you could see a bigger dip in your score as a result of all of those inquiries on your report.

You missed a payment once or twice.

You might think that missing a payment here and there is not that big of a deal, but in reality, it can wreak havoc on your credit score. Recall that payment history is the most important factor contributing to your credit score, weighing in at 35% of your FICO score.

If you are 30 days late on making a payment even one time, this can have a significant detrimental effect on your credit, dropping your score by as much as 60 to 110 points.

If you still fail to make your payment by the following due date, then you get a 60-day late on your credit report, which hurts your credit even more.

30-day and 60-day lates are both considered minor derogatory items on your credit report, so they won’t mess up your credit as much as a major derogatory item.

However, if you get a 60-day late payment added to your credit report, do your best to catch up on payments before another 30 days pass, which is when things get even worse.

You missed a payment for three months in a row or more.

Missing a payment even once can seriously set back your credit score, but the damage will be even worse the longer you put off bringing the account current.

Once you reach 90 days past due on a credit account, that is now considered a major derogatory item, which is the worst possible type of item to have on your credit report. (Other major derogatory items include charge-offs, collections, foreclosures, settlements, judgments, repossessions, public records, and bankruptcies.)

Having a 90-day late on your credit report is certainly going to have a negative impact on your credit. A credit score drop from a major derogatory item will be even more severe and more difficult to recover from than that of a minor derogatory item. In addition, the major derogatory item could scare away potential lenders, making it harder to obtain credit in the future.

If you default on a debt, meaning you did not fulfill your obligations to repay that debt, your creditor can sell your account to a collection agency, who will then try to collect the debt from you. A collection account is also a major derogatory item on your credit report, which means it can seriously hurt your score if you have an account go into collections.

You applied for multiple credit cards in a short period of time.

Applying for multiple credit cards results in hard inquiries on your credit report, which can have a more significant impact on your score than just one inquiry.

Having too many hard inquiries on your credit report in a short period of time indicates that you are seeking a lot of new credit, which is a bad sign to lenders, and it will bring down your score.

With most credit scoring models, inquiries for credit cards are all counted separately, even if they were all around the same time. Since inquiries can each cost your credit score up to five points, that can add up quickly. (The exception to this is the VantageScore credit score, which counts all inquiries made within a 14-day window of each other as one inquiry, regardless of the type of account.)

Furthermore, if you got approved for and opened all of the accounts that you applied for, then you could also end up with too many new credit accounts on your credit report.

One of your credit cards was closed.

Many consumers mistakenly believe the credit myth that it will help their credit if they close some of their accounts. In a way, that makes sense, because it lowers the amount of available credit you have, which reduces the potential amount of debt you could get into if you were to use all of your available credit.

However, that is not how credit scores work, because unfortunately, credit scores don’t always make sense.

The truth is that closing an account almost always hurts your credit instead of helping it.

With revolving accounts, such as credit cards, closing an account reduces your total credit limit by removing the credit limit of that card. When you reduce your credit limit, that action increases your overall credit utilization ratio, meaning that you are now using a larger fraction of your available credit.

This hurts your credit score because having a high credit utilization ratio is penalized by the credit scoring algorithms, whereas maintaining a low utilization ratio is rewarded.

The worst-case scenario for your credit when closing an account is if the account is closed while it still has a balance on it. In this case, that individual account will look like it is maxed out or over the limit because it has a balance but no credit limit. That alone is enough to significantly harm your credit, and the increase to your overall utilization ratio only worsens the problem.

Depending on what else is in your credit file, closing a credit card could also negatively affect your credit mix, which could result in a small credit score drop.

On the plus side, the reason why an account was closed does not play a role in your score, so you won’t be affected more negatively if the card was closed by the issuer than if it was closed at your request.

Have you checked your credit card statements lately?

An unexpected decrease in your credit score could be the result of fraudulent activity on your accounts.

If you see any charges on your statement that you do not recognize, then it could be fraudulent activity that is bringing down your score. Perhaps someone was able to obtain your credit card information by phishing or through a data breach and used it to run up the balance on the card.

It’s important to monitor your credit accounts regularly so that you can catch any suspicious activity early on. Better yet, set up email or mobile notifications on your account that will alert you to fraudulent activity instantly.

If a criminal does manage to get access to your account, report the fraudulent charges to your credit card issuer immediately and ask to have the charges reversed. Most credit card companies have a zero liability policy, which means you won’t be held responsible for paying for any of the fraudulent charges.

You paid less than the minimum payment.

If your cash flow is tight, it can be tempting to send the bank or credit card company a partial payment instead of the full amount that is due that month. You may think that it’s not as big of a deal as not paying at all, because at least you are sending them some of the money.

Unfortunately, it doesn’t work that way. If you do not cover the full minimum payment by the due date, it will not be counted as an on-time payment.

If you can bring the account current before 30 days pass, you may still have to deal with a late fee from your credit card issuer (although it’s worth asking them to waive the fee), but at least the late payment will not show up on your credit report.

On the other hand, if you do not make a sufficient payment and 30 days go by, then you will have a late payment pop up on your credit report, which can definitely take a toll on your credit score.

To prevent this from happening, as soon as you know you will not be able to make the full payment, contact your credit card issuer and ask if they have a financial hardship program or try to negotiate an arrangement with them that allows you to pay what you can without damaging your credit.

You didn’t use your credit card for a long time.

Your credit card issuer might have closed your account if it had been inactive for a long time.

If you don’t use a credit card for a long period of time, it’s possible that your credit card issuer may decide to close your account due to the lack of activity.

As we discussed above, a closed credit card is bad news for your credit since the loss of available credit hurts your credit utilization and it may also damage your mix of credit.

According to The Balance, the credit card company is not required to give you advance notice if they plan to close your account, so it’s best to take proactive measures to prevent this from happening.

To avoid having your card closed due to inactivity, make sure you use it to make a purchase at least once every few months. An easy way to do this is to use the credit card to pay for a subscription service that renews each month. Then, set up automatic bill payments on your credit card and the whole process will be automated.

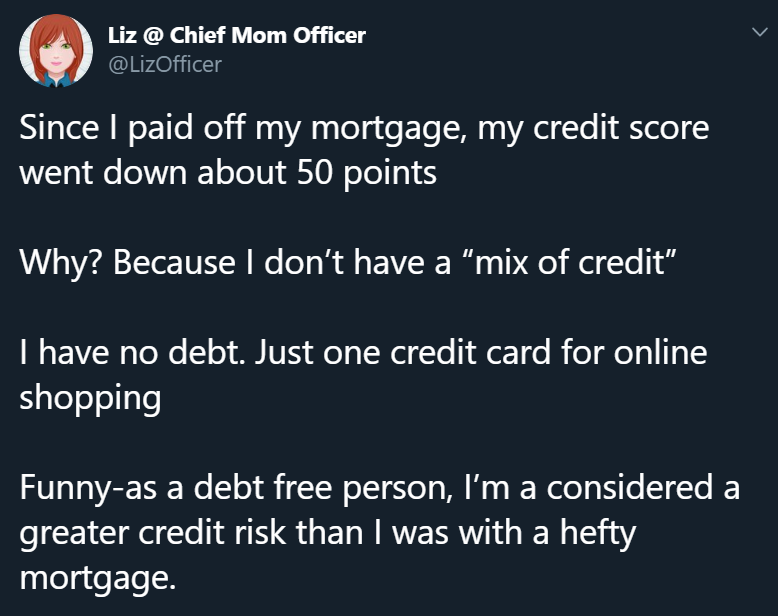

You finished paying off an installment loan.

Making the final payment on your auto loan, student loans, or mortgage is an exciting accomplishment. Yet, when you finish paying off an installment loan, your credit score may decrease instead of increase.

Even though you now have less debt, which sounds like it would help your credit score, this may not outweigh the negative impact to your mix of credit. The paid-off installment loan will now report as a closed account, which can be harmful to your credit if all you have left is a few revolving accounts.

@LizOfficer shared a real-life example of this on Twitter.

This Twitter user commented that paying off her loan made her credit score go down since it affected her mix of credit.

An account that you are piggybacking on became delinquent.

Sometimes being an authorized user on a credit card or having a joint account can be a risky thing. You are relying on the other person to pay their bills on time and to manage their balances well, otherwise their behavior can compromise your credit.

In other words, an ideal tradeline should have a low utilization ratio, it should have a higher age than your average age of accounts and your oldest account, and most importantly, it needs to have a perfect payment history.

Therefore, you want to avoid being added as an authorized user to a tradeline that has any derogatory marks on it so that those derogatory items don’t get added to your credit file and end up damaging your credit.

That’s the danger of piggybacking on a friend or family member’s credit card—even if the tradeline is perfect when you are first added to it, there’s no guarantee that it will stay that way.

If your authorized user tradeline does get any missed payments on its record, that could definitely hurt your credit, and it would be smart to remove yourself from it immediately. To do so, simply call the credit card issuer and request to be removed from the account, as most banks allow you to do this without needing to go through the primary account holder.

Delinquency on the part of the primary account holder can cause problems if you are piggybacking on someone else’s credit account.

You declared bankruptcy.

Bankruptcy is one of the worst things you can have on your credit report. Since declaring bankruptcy essentially means you are asking to be released from the legal obligation to repay your debts, it shows lenders that you have an extremely high risk of defaulting in the future, so it can have a severe negative impact on your credit score.

There are inquiries on your credit file that you did not authorize.

Unauthorized inquiries on your credit file can unfairly drag down your credit. In our article on credit inquiries, we reported that each hard inquiry on your credit report can potentially cost you up to five points each.

Fortunately, you have the right to dispute any hard inquiries on your credit report that you did not authorize. You can learn more about the credit dispute process in “How to Fix the Most Common Credit Report Errors.”

Your credit file got merged with someone else’s.

Sometimes inaccurate information can get on your credit report not as a result of fraud or because your lender reported it incorrectly, but because your credit file accidentally became mixed with the information of another person.

This is called a “mixed credit file” or “mixed credit report” and it usually occurs with two consumers who have similar names.

If the credit history of the other consumer with whom your file has been mixed contains negative information, that would obviously be detrimental to your score, and you would need to correct the situation by filing a dispute with the credit bureau.

This is an example of why it’s important to check your credit report regularly. If there is incorrect information on your credit report that should be removed, you don’t want to find out about it when you’re trying to apply for credit. You need to catch and correct credit report mistakes early so that they don’t stand in the way of you achieving your financial goals.

You maxed out one or more of your credit cards.

Credit utilization makes up nearly a third of your FICO score, which means it’s critically important to keep your utilization low if you want to maintain a high credit score. Maxing out even just one credit card can have a significant negative impact, and if you max out multiple cards, you’ll be even worse off.

An account on your credit report that you don’t recognize could be an account that someone else fraudulently opened in your name.

We already covered how opening a new account can negatively affect your credit initially, but don’t forget that the same thing can happen if someone else uses your name to sign up for a new account.

If you see that your credit score has decreased, take a look at the inquiries and accounts on your credit report to see if there are any items that should not be there.

You have “double jeopardy” with collection accounts on your credit report.

Debt collection agencies are not known to be the most trustworthy entities and often do not have the best practices when it comes to keeping track of debts and contacting consumers. Information often gets lost or misrecorded when it is transferred between creditors and sometimes numerous collection agencies.

Because of this, some consumers find themselves with more than one entry for the same open collection account on their credit report, which is known as “double jeopardy.”

While the same collection may be listed multiple times due to the account changing hands, only the entity who currently owns the debt should be reporting the account as open.

Fortunately, if a collection is being reported in error, you can dispute the inaccurate information and have the information be corrected or potentially removed altogether.

Your credit report says you missed a payment even though you paid on time.

Dispute any mistakenly reported late payments so that they don’t unfairly affect your credit score.

Since payment history is the most important factor in your credit score, an incorrectly reported missed payment could severely damage your credit, especially if you are starting with very good credit. The higher your score to begin with, the more you stand to lose from a credit mistake.

This type of situation is another example that demonstrates why it’s so crucial to regularly check your credit report. If you always made all of your payments on time, you might assume that you must have a spotless credit record, only to find out at an inconvenient time that a creditor has been incorrectly reporting that you missed a payment.

Keep an eye out for errors like this on your credit report so that you can dispute them right away.

Your credit card issuer reduced your credit limit.

Sometimes, credit card issuers lower the credit limits of their cardholders, even for those who have consistently managed their accounts responsibly.

Unfortunately, they are usually allowed to do this without asking for your permission or letting you know in advance, so it may come as a nasty surprise when you swipe your credit card and get declined, or when your credit score takes a dive because your credit utilization is suddenly much higher.

There are a few reasons why your bank may reduce your credit limit, such as the following:

Credit card issuers sometimes cut credit card limits, which hurts your credit utilization ratio.

Your balances have been increasing, which indicates that you are taking on more debt and might be at a greater risk of defaulting.

You missed a payment and your account becomes delinquent.

Your account was inactive because you did not use your credit card enough.

The economy is down and lenders want to minimize their risk exposure levels.

Regardless of why your credit limit took a hit, the result is the same: with less available credit, your credit utilization increases, which is bad for your score.

If your credit card issuer slashed your credit limit, check out “How to Increase Your Credit Limit” for some useful tips, and don’t be afraid to give your bank a call to ask them to reconsider.

A collection account was deleted from your credit report.

Surprisingly, it is actually possible that getting a collection account removed from your credit report could make your credit score go down instead of up.

By removing a collection account from your credit report, it is possible that you could move from one bucket into another bucket where your score will now be calculated differently. As a result of this new algorithm being applied to your credit report, your score could turn out to be lower than it was when you were in the first bucket.

You haven’t used any credit in a long time.