Soft Vs. Hard Inquiry – What’s the Difference?

Sometimes it’s the little things in life that can make all the difference.

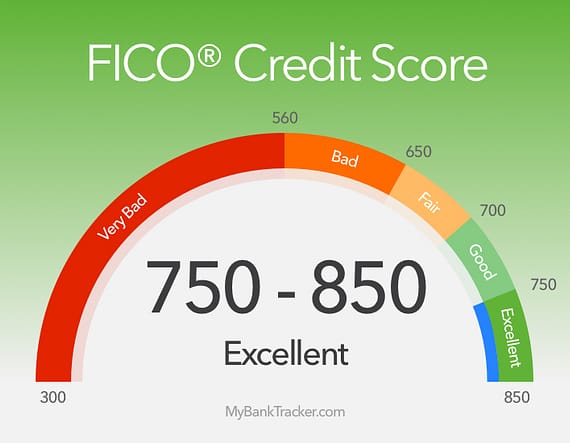

A small ding to your credit score can drop it just enough from being in the excellent credit score range to the good score range. That can be enough to cause lenders to charge you higher interest rates, costing you money that you might otherwise save without the small nick on your credit score.

Inquiries, or new credit, account for about 10 percent of a FICO credit score. While that isn’t much when compared to payment history accounting for 35 percent of a FICO score, a credit score drop of up to 10 percent for having too many lenders look at your credit score can be enough to cost you real money in the long run.

There are two types of inquiries — hard and soft — and the first will hurt a credit score and the latter won’t. Knowing the difference can help you know when to act so that an inquiry doesn’t hurt your score, or when you don’t have to worry about it.

Hard inquiry defined

An example of a hard hard inquiry is when you apply for a credit card and the issuer “pulls” your credit report from one of the three major credit bureaus.

The hard inquiry may lower your score up to five points, depending on the rest of your credit profile. Going months between credit inquiries can have less of an impact than having a bunch at the same time.

Applying for a mortgage is another hard inquiry. The FICO score allows mortgage rate shopping, so applying with four different mortgage lenders in 45 days is counted as only one hard inquiry.

Hard inquires stay on a credit report for two years, but the FICO score ignores them after 12 months. Whatever your credit score, potential lenders will look at you as risky if you have too many inquiries over a short period. For people with a short credit history, this can be especially troublesome.

What’s a soft inquiry?

Soft inquiries come in many forms, and none should hurt a credit score.

Checking your own credit report is a soft inquiry. It doesn’t lower your credit score, as some people think it does, and in fact is a good thing to do to make sure your score is good and the information on your credit report is accurate. Consumers can check their credit reports for free once a year from each of the three major credit bureaus.

Creditors you already work with may do soft inquiries by checking your credit report to see if you’re still creditworthy. Credit card companies do this monthly.

If you get preapproved credit card offers in the mail, those are soft inquiries that don’t affect your score.

If you’ve given a potential employer permission to view your credit report as part of a background check, it’s also a soft inquiry that doesn’t affect a credit score.

What you can do

If you want to avoid a hard credit inquiry that could cause your credit score to drop, the simple solution is to not apply for new credit. But that isn’t always practical, such as if you want to find a better credit card or want to buy a home or car.

There are some money management steps you can take, however.

Start by not applying for credit cards that you know you won’t qualify for. Knowing where your score is on the credit score range can help you decide if applying for a card with some of the best travel rewards, for example, is worthwhile since many such cards require having excellent credit. Applying for a credit card that you probably won’t be approved for results in a hard inquiry and a rejection, which can also hurt your score.

Some credit card issuers target people with bad credit. If that’s you, be sure to read the fine print and make sure it’s a card you can live with. It may not have all of the features you want, but over time and by paying the bill on time, you can improve your credit score and move up to a better credit card.

These issuers may advertise that they won’t run a hard credit check and will base their decision on other factors, such as your income and employment history.

If you have good or excellent credit, a hard inquiry shouldn’t have much of an impact, if any, on your credit score. Keep your score high by paying your bills on time, don’t use more than 30 percent of the credit available to you, and have a good mix of credit.

When checking your credit score, look for errors and dispute them with the credit bureaus. Your vigilance should pay off with a better credit score and eventually should get you better credit terms. With that, a hard credit inquiry won’t hurt so much, if at all.

The post Soft Vs. Hard Inquiry – What’s the Difference? appeared first on Better Credit Blog | Credit Help For Bad Credit.

Read more: bettercreditblog.org